Gold, Oil & Global Currencies Entering a Watershed Moment

Below we look at the math, history and current oil environment in the backdrop of a global debt crisis to better predict currency and gold market direction without the need of tarot cards.

Seeing the Future: Math vs. Crystal Balls

Those looking forward only need to look at current and backward math to make relatively clear forecasts without risking the mug’s game of deriving crystal ball predictions.

Not surprisingly, the theme and math of simple (as well as appalling) US debt levels makes such forward-thinking almost too simple.

The Oil Issue: Is Anti-Shale Anti-American?

Although not as fluent as others in the oil trade or the green politics of the extreme US left, I’ve argued in prior reports that the current administration’s anti-shale policies make for some good (debatable?) environmental chest-puffing while ignoring the math, history and science of sound national as well as well as global thinking.

(But then again, the entire woke fiasco of current US policy seems to be on a crusade to cancel such things as math, history and science; so, thinking contextually or globally is beyond their sound-bite-driven stump-speeches.)

Oil, however, still matters.

And when understood in the broader context of the macro-economic themes we’ve tracked for years–namely debt, currencies, inflation, gold, a cornered Fed and a weaponized USD–the current and future trends are already in motion.

And as for the endless debate as to global warming, butterfly-friendly energy policies and the simple reality of fossil fuels as a part of, rather than threat to, our planet, I’m certainly not here to answer or solve the same.

Certainly the Germans (and their solar powered ideas in a part of Europe with very little sun) are not getting it… In fact, they are getting much of their (nuclear) energy from France and are now forced to burn coal to get through the winter.

I am here, however, to lay down some objective facts and ask some blunt questions.

Oil Politics

Biden, it seems fairly clear to all, is not in charge of US policy.

That’s a scary fact. Even more scary, however, is determining who is in charge?

Again, not something I can answer.

But if he were in charge, we’d all be amused to ask how he expected Saudi Arabia to welcome him and his embarrassing pleas for Saudi production increases (to ostensibly ease inflated US fuel costs) after previously telling the world he considered Saudi Arabia a pariah state…

We all remember that embarrassing fist-pump with the Crown Prince.

Meanwhile, Saudi is now spending far more time with the Chinese and Iran…

We’d also love to hear the White House explain how it expects increased US shale production to reduce energy inflation when it has been simultaneously seeking to legislate oil off the American page.

Furthermore, it would be worth reminding Americans and politicians tired of inflated fuel prices that the vast majority of those inflated pump costs are due to US taxes per gallon, not Saudi production cuts.

But I digress.

Oil Math

At the current levels of US oil production and exploration, the US (according to its own Dallas Fed) will have to engage in annual energy price inflation levels of 8-10% just to keep the oil industry’s lights on at a breakeven price level.

Such conservative inflation figures for oil/fuel pricing, when seen in the context of over $31T in US Federal debt, basically means that Uncle Sam’s ability to cover his ever-increasing public debt burden will weaken by at least 8-10% per year at a moment in US history where Uncle Sam needs all the help, rather than weakness, he can get.

Fighting Inflation with Inflation, and Debt with Debt?

Needless to say, the only “solution” to these inflated debt burdens will be the monetary mouse-clicker at the Eccles Building, whose doom-loop (yet now ossified) “solution” to addressing inflated oil prices is the even more inflationary policy of printing more fake money to “fakely” cure an inflation crisis.

You really can’t make this stuff up.

Fed monetary policy, ever since patient-zero Greenspan sold his soul (and sound-money, gold-backed academic thesis) to Wall Street and Washington, boils down to this: We can solve a debt crisis with more debt, and an inflation crisis with more, well…inflation.

Does this seem like “sound monetary policy” to you?

Or, Just Export Your Inflation to the Rest of the World?

But as I’ve warned for years, Uncle Sam’s first instinct (as holder of the world reserve currency) whenever handed a hot-potato of self-inflicted inflation, is to hand it off to the rest of the world—i.e., to export his inflation to friends and foes alike.

Global energy importers in Europe, emerging markets, India, China, and Japan, for example, are facing what accountants call a balance of payments crisis, but what I’ll bluntly call by its real name: A currency crisis.

That is, under the current, but potentially dying petrodollar system, these countries will need more USDs to buy oil.

But that’s where the problem lies.

Why?

Simple: Those USDs are drying up (unless more are printed).

How Long Will Global Currencies (& Leaders) Remain Prisoner to the USD?

Regardless of whether you believe in the perpetual hegemony of the USD as a payment system or not, we can all agree that USD liquidity is drying up (whether it be from the milk-shake theory absorption in euro-dollar and derivative markets or from post-sanction de-dollarization).

Nations facing the double whammy of needing more USDs to pay for inflated oil prices and inflated USD-denominated debts around the globe are going to being crying “uncle!” rather than just “Uncle Sam.”

What can these nations do in the face of that bullying hot potato known as the USD? How can they service these increased USD payment (oil and debt) burdens?

How the US Creates a Global Currency Crisis

Well, short of turning their backs on the USD (not yet), the only current option other nations have is to devalue (i.e., inflate and debase) their own currencies at home, which is how Uncle Sam makes his problem just about everybody else’s problem…

As I often say, with friends like the US, who needs enemies?

Something, however, has to give.

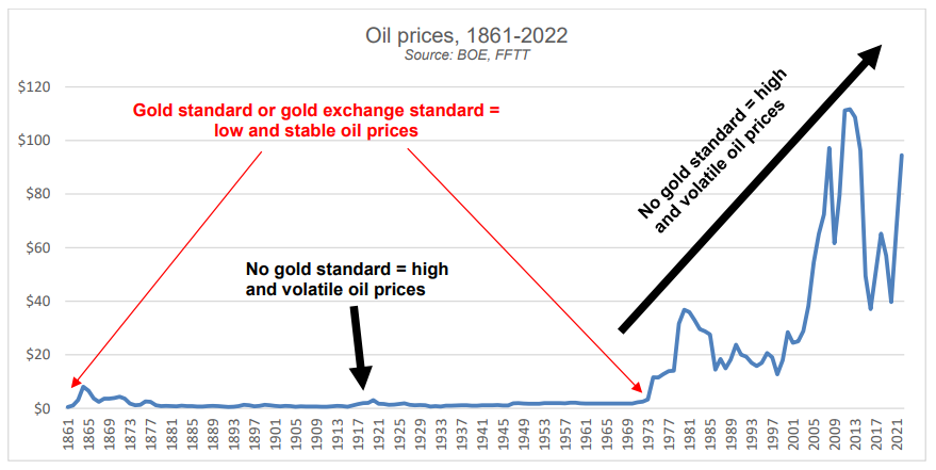

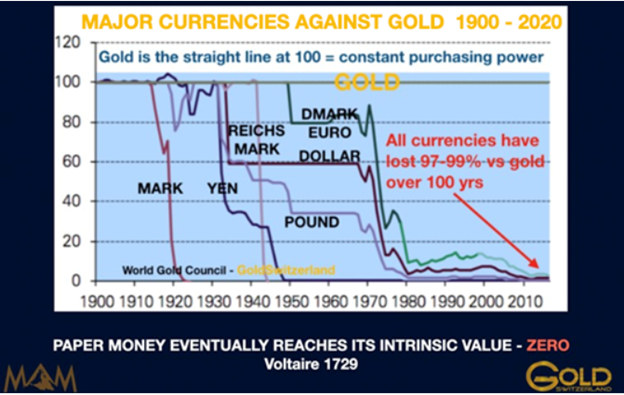

How Physical Gold Offers Better Pricing than Fiat Dollars

This clearly broken system of the US exporting its inflation upon a world forced since the 1970’s to import oil under a broken and inflationary Greenback has a genuine potential to implode.

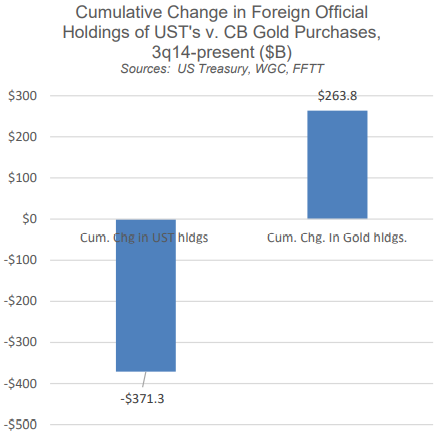

Already, countries like Ghana have realized that it’s better to trade oil in real gold rather than fake fiat dollars.

Long before the petrodollar became the mad king, for example, history recognized that physical gold was a far better instrument of payment to settle stable oil pricing.

See for yourself.

As more and more of the world recognizes the currency crisis slowly in play now, and then steadily in greater pain tomorrow, this “Balance of Payments” (i.e., currency) crisis can easily evolve into a “change of payments” reality in which gold re-emerges as a superior payment system for oil.

Think about that.

More Tailwinds for Gold

As of this writing, the physical oil markets are greater than 15X the size of the physical gold markets on an annualized (USD) production basis.

If the world turns slowly (then all at once?) toward settling oil in gold (partially or fully) to avoid a global currency crisis, gold will have to be repriced at levels significantly higher than current pricing.

Hmmm.

Something worth tracking, no?

Well, the Zeitgeist suggests that we are not the only ones tracking these trends…

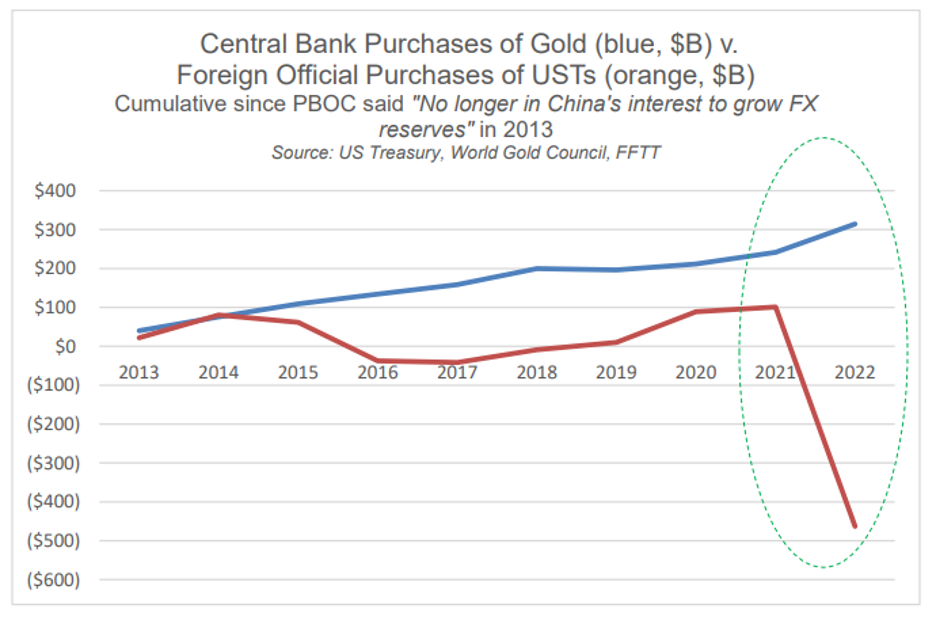

The Central Banks Are Catching On to (and Stacking) Gold

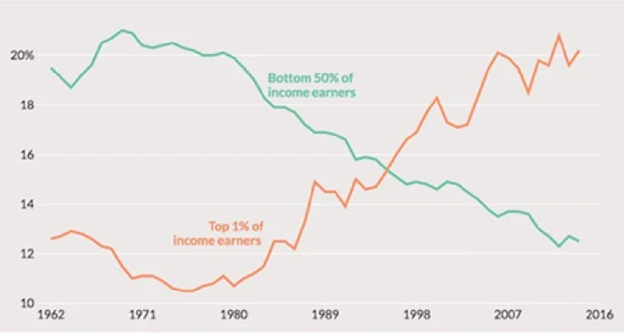

A recent pole of over 80 central banks holding greater than $7T in FX reserves indicated that 2 out of 3 polled strongly believe that central banks will be making more, not less, purchases of physical gold in 2023.

Again: Are you seeing a trend? Are you seeing the context? Are you seeing why?

As I’ve said countless times and will say countless times more: Debt matters.

Debt matters because debt, once it crosses the Rubicon of insanity and unsustainability, impacts everything we market jocks were supposed to have been taught in school and in the office—namely bonds, currencies, inflation and recessionary cycles follow debt cycles.

In short: It’s all tied together.

Once you understand debt, the policies, reactions, weaknesses, truths, lies, and cycles are far easier to see rather than just “predict.”

The increasing loss of faith in the world reserve currency and its embarrassing IOUs (i.e., USTs) is not merely the domain of “gold bugs” but the simple and historical consequence of the blunt math which always follows broken regimes, of which the US is and will be no exception.

The graph below, is thus worth repeating, as the world is clearly turning away from Uncle Sam’s drunken bar tabof debased dollars and IOUs toward something more finite in supply yet more infinite in duration.

Again: See the trend?

Gold, Oil & Global Currencies Entering a Watershed Moment

From oil markets to treasury stacking, backdoor QE, investor fantasy and hedge fund prepping, it’s becoming more and more clear that the big boys are bracing for disaster as gold stretches its legs for a rapid run north.

Recently, I dove into the cracks in the petrodollar as yet another symptom of a world turning its back on USTs and USDs.

Gold, of course, has a role in these headlines if one looks deep enough.

So, let’s look deeper.

Diving Deeper into the Oil Story

The headlines of late, for example, are all about “surprise” OPEC production cuts.

Why is this happening and what does it say about gold down the road?

First, let’s face the politics.

As noted many times, it seems US policy, on everything from short-sighted (suicidal?) sanctions to the “green initiative” makes just about zero sense in the real world, which is miles apart from the “keep-me-elected” fantasy-world of DC.

After all, energy, matters, which means oil matters.

But the current regime in DC has been losing friends in Saudi Arabia and cutting its prior and once admirable shale production outputs (think 2016-2020) in the US despite a world that still runs on black gold fighting against green politics.

The DC attack on shale may make the Greta Thunbergs happy, but let’s be blunt: It defies economic common sense.

Saudi, by cutting production, is now showing a still very much oil-dependent world it is not afraid of losing market share to the USA in the face of rising oil for the simple reason that the USA just aint got enough oil to fill the gap or flex its energy muscles.

In the meantime, Chinese demand for crude is peaking while Russian oil flows to the east (including to Japan) are hitting new highs at prices above the US-led price cap of $60/barrel.

If DC has any blunt realists (wrongly castigated as tree-killers) left, it will have to re-think its anti-oil policies and get back toward that recent era when US shale was responsible for 90% of total global oil supply growth.

If not, oil prices can and will spike, making Powell’s war on inflation even more of an open charade.

Speaking of inflation…

Ghana Oil-for-Gold Beats Inflation

When it comes to oil and the decades-long bully-effect of a usurious USD (See: Confessions of an Economic Hitman), we have argued countless times that a strong USD and an imposed petrodollar was gutting developing economies around the world.

We also warned that developing economies (spurned by global distrust of the Greenback in a post-Putin-sanction era of a weaponized reserve currency) would respond by turning their backs on US policies and its dollar.

In the old days, the US could export its inflation abroad. But those days, as we warned as early as March 2022, would be slowly but steadily coming to a hegemonic end.

Again, this does not mean (nod to the Brent Johnson) the end of the USD as a reserve currency, just the slow end of the USD as a trusted, used or effective currency.

Toward that slow but steady end, it’s perhaps worth noting that Ghana’s inflation rate has fallen from 156% to just over 60% since it began trading oil for gold rather than weaponized USDs.

Hmmm.

Gold Works Better than Inflated Greenbacks

The most obvious conclusion we can draw from such a predictable correlation is that gold seems to be working better than fiat dollars to fight/manage inflation, a fact we’ve been arguing for well…decades.

From India to China, Ghana, Malaysia, China and 37 other countries engaged in non-USD bilateral trade agreements, the inflation-infected USD is losing its place in more than just the critical oil trade.

Nations trapped in USD-denominated debt-traps (thanks to a rate-hiked and hence stronger and more expensive USD) are now finding ways to tie their exports (i.e., oil) to a more stable monetary asset (i.e., GOLD).

This, of course, makes me that much more confident that as the world moves closer to its global (and USD-driven) “Uh-Oh” moment, that the already-telegraphed Bretton Woods 2.0 will have to involve a new global order tied to something golden rather than just something fiat.

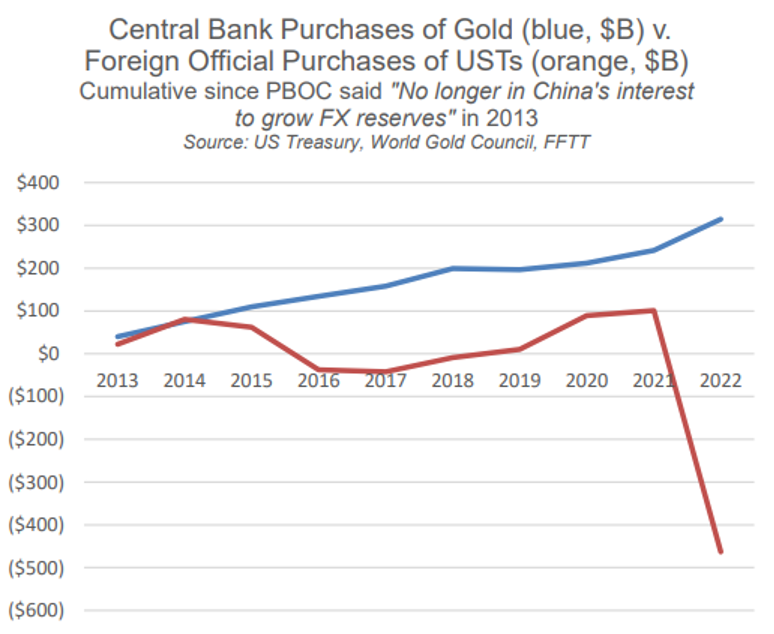

This, again, explains why so many of the world’s central banks are loading up on gold rather than Uncle Sam’s IOUs.

Gosh. Just see for yourself:

Ouch.

Uh-oh?

US Investors: Still High on Past Fantasy Rather than Current Reality

Sadly, however, the US in general, and US investors in particular, remain trapped in a spiral of cognitive dissonance and still believe today and tomorrow’s America is the America of magical leaders, deficits without tears and the balanced-budget honesty of the Eisenhower era.

That’s why the vast majority (and their consensus-think, safety-in-numbers advisors) are still huddling in correlated 60/40 stock bond allocations rather than physical gold according to a recent BofA survey of wealth “advisors.”

This always reminds me of a phrase circling around Tokyo just before the grotesquely inflated Nikkei bubble lost greater than 80% of its hot air in the crash of 1989, namely: “How can we get hurt if we’re all crossing the road at the same time?”

Well, a large swath of US investors (and their “advisors”) is about to find out how.

Doubling Down on Return Free Risk

This may explain why US households (a statistical term of art which includes hedge funds) have upped their allocations to USTs by 165% ($1.6T) since Q4 of 2022 at the same time that the rest of the world (see above) has been dumping them.

But in all fairness, this does make some sense, as higher rates in the US give investors in USTs (especially in short-duration/money market securities) a greater return than their checking or savings accounts.

Unfortunately, where the masses go is also where bubbles go; but as I like to remind: All bubbles pop.

Of course, when adjusted for inflation, these poor US investors are still getting a negative return on USTs.

Foreigners, of course, have stopped falling for this, but when Americans themselves get suckered en masse into this same bond-trap, they’re basically just paying an invisible tax while chipping away at GDP growth and unknowingly helping Uncle Sam finance his debt for free (namely: at a loss to themselves).

Crazy?

Yep.

Negative Returning IOUs—The Lesser of Evils

But why are hedge funds (i.e., the “smart money”) falling for this? Why are they loading up on USTs?

Because they see trouble ahead, and even a negative returning UST is safer (less evil) than a tanking S&P–and that’s exactly what the pros are bracing for/anticipating.

Waiting for a Market Bottom

In short: The big-boys are safe-havening today in negative-USTs so that they’ll have dry powder at hand to buy a pending and massive market bottom tomorrow.

Once they can buy a bottom, they too will dump Uncle Sam’s IOUs as the QE (along with inflation) kicks back to new highs thereafter.

And speaking of QE…

Backdoor QE: Coordinated and Synthetic Liquidity by Another Name

I have always endeavored to simplify the complex with big-picture common sense.

Toward this end, let’s keep it simple.

And the simple truth is this: With US debt at unprecedented and unsustainable levels, it is a matter of national survival to prevent bond yields—and hence bond-driven rather than Fed- “set” interest rates–from spiking.

Such a natural, and bond-driven spike, after all, would make Uncle Sam’s embarrassing debt too expensive to function.

Survival vs. Debate

Thus, and to repeat: Keeping bond yields controlled is not a matter of pundit debate but national survival.

Since bond yields spike when bond prices fall, it is thus a matter of sovereign survival to keep national bond prices at reasonably high levels.

This, however, is naturally impossible when bond demand (and hence price) is naturally sinking.

This natural reality opens the door to the un-natural “solution” wherein central banks un-naturally print trillions (“synthetic demand”) to buy their own bonds/debt.

Of course, this game is otherwise known as QE, or “Quantitative Easing”–that ironic euphemism for un-natural, anti-capitalist, anti-free market and anti-free-price-discovery Wall Street socialism whose inflationary consequences cause Main Street feudalism.

In short: QE has backstopped a modern system of central-bank-created lords and serfs.

Which one are you?

See why Thomas Jefferson and Andrew Jackson feared a Federal Reserve, which is neither “federal,” nor a solvent “reserve.”

The ironies, they do abound…

How Can there be QE if the Headlines Say QT?

But the official narrative and headlines are still telling us only stories of QT (Quantitative Tightening) rather than QE, so what’s the problem?

Well, as with just about everything from CPI data and transitory inflation memes to recession re-defining, the official narrative is not always the truthful narrative…

In fact, back-door or “hidden QE” is all around us, from the Fed bailing out/funding repo markets and dead regional banks to central banks making secret deals behind the scenes.

Although it’s not officially QE when the central bank of one country is buying the IOUs (bonds) of another country, it is more than likely that leading central banks are acting in a coordinated way to “QE each other’s debt,” a system which former Fed official, Kathleen Tyson, describes as a “Daisy Chain.”

And if we look at the IMF’s own data, we can connect the dots of this Daisy Chain with relative (rather than tin-foil-hatted) clarity.

Since Q4 of 2022, for example, overall FX reserves are now up by over $340B, the equivalent of over $100B per month of central bank QE by another name.

Toward that end, the math is simple, with: 1) GBP reserves up 10% (no surprise given the gilt implosion of Oct. 2022), JPY reserves up nearly 8%, EUR reserves up 7% and USD reserves only up only 0.5%.

Not only does this look like backdoor QE masquerading as “building excess reserves,” it looks to me, at least, like a coordinated attempt by DXY central banks to collectively weaken the 2022 USD which Powell’s rate hikes had made painfully too high for the rest of the world, a fact/pivot of which we warned throughout 2022.

Since the above G7 policies kicked in, the USD has fallen 11% into 2023 as the other DXY currencies (JPY, EUR and GBP) gave themselves a little backdoor/QE boost.

It seems, in short, that the need for artificial liquidity in a world thirsty for USDs found a clever way to weaken the relative strength (and cost) of that USD (and confront/tame skyrocketing volatility in USTs) without overtly requiring Powell to mouse-click dollars from his own laptop.

Why Markets Rise into a Recession

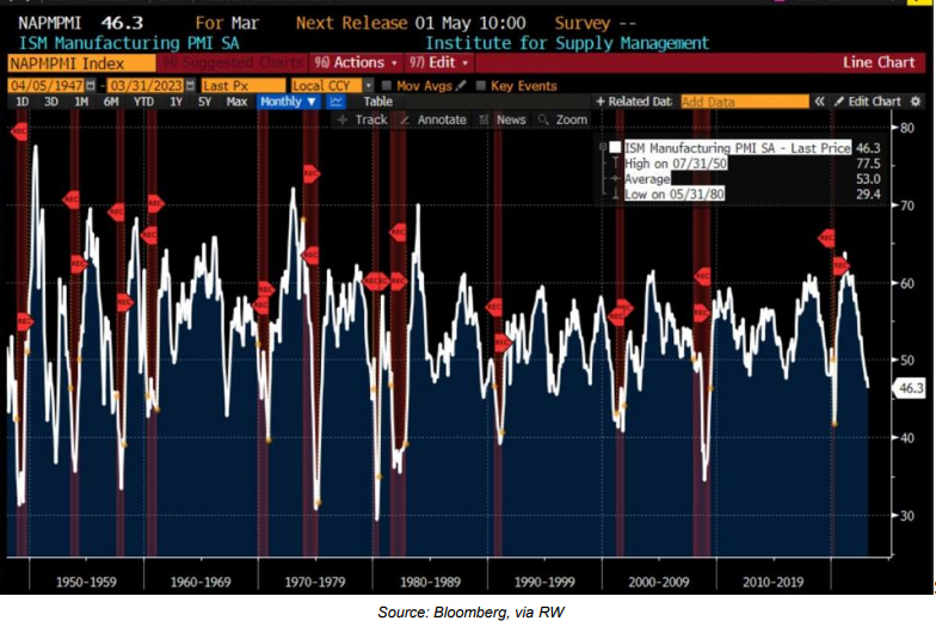

This unofficial but likely coordinated play to constructively weaken the USD among the big boys helps explain why the S&P has been rising into 2023 despite open indicators that the country is itself marching toward a recession.

US Manufacturing data (ISM) is now at levels consistent with a recession…

Again: The ironies (and un-natural manipulations) abound.

Meanwhile, the Atlanta Fed’s GDPNow is down 1.5% from March’s 3.2% figure.

But hey, who needs growth, productivity, tax receipts or even a modicum of national economic health to keep a liquidity-supported stock market from defying reality—at least for now…

Waiting to Pay the Debt Piper…

Ultimately, of course, debt will get the last, cruel laugh, and with the US heading toward a deficit that is greater than 50% of GLOBAL GDP (!), I personally believe the Fed will need to return to its own money printer in a big way once this market charade ends in an historical “uh-oh” moment.

This seemingly inevitable return to mouse-click trillions (inflationary) will likely come after a deflationary implosion in equity assets currently supported by the foregoing tricks and fantasy rather than earnings and growth.

In the interim, and like those hedge fund jocks discussed above, we can only wait for things to get S&P ugly as gold, often sympathetic in the first hours of a market crash, rips toward all-time highs thereafter.

Gold, Oil & Global Currencies Entering a Watershed Moment

The latest headlines, of course, are all pointing toward the ripple effect of Silicon Valley Bank (SVB), and they should be.

This banking metaphor for the tech sector in particular and the previously described disaster in California as a whole or the matter of banking risk as a theme, require understanding and attention, provided below.

Once we get past a forensic look at the data and forces which explain SVB’s demise, we quickly discover that SVB is itself just a symbol of a much larger financial (and banking) crisis which ties together nearly all of the major macro forces we’ve been tracking since Powell began his QE to QT quest to be Volcker-reborn.

That is, we confirm that everything comes back to the Fed and bond market in general and the UST market in particular. But as I’ve argued for years, and will say again now: The bond market is the thing.

By the end of this brief report, we also discover that SVB is just the beginning; contagion inside and outside of the banking sector is about to get worse. Or stated more bluntly: “We aint seen nothing yet.”

But first, let’s look at the banks in Silicon Valley…

Two Failed Banks

The tech-friendly SVB story (i.e. FDIC shutdown) is actually preceded by another failed bank, namely the crypto-friendly Silvergate Capital. Corp, now heading into voluntary liquidation.

Because SVB was a much larger bank (>$170B in deposits) than Silvergate (>$6B in deposits), it got and deserved more headlines as the largest bank failure since well, the 2008 bank failures…

Unlike Lehman or Bear Stearns, the recent disasters at SVB and Silvergate were not the result of concentrated and levered bets/loans negligently packaged as investment-grade credits, but rather the result of a good ol’ fashioned bank run. Bank runs happen when depositors all want to get their money out of the banks at the same time—a scenario of which I’ve warned for years and compared to a burning theater with an exit door the size of a mouse-hole.

Banks, of course, use and lever depositor funds to lend and invest at risk (which is why Henry Ford warned of revolution if folks actually understood what banks actually do). Thus, if a mass of depositors suddenly wants their money at the same time, it’s just not gonna be there.

So, why were depositors in a panic to exit?

It boils down to crypto fears, tech stress and bad banking practices.

No Silver Lining at Silvergate

At Silvergate, they provided loans to crypto enterprises, which were the belle of the speculation ball until Sam Bankman-Fried’s FTX implosion made investors weary of crypto exchanges. Nervous depositors withdrew billions of their crypto-linked deposits at the same time.

Silvergate, of course, didn’t have the billions needed to meet depositor requests, because, well… banks by their operational (fractional reserve) nature never have the money when needed at the same time.

Thus, the bank had to quickly and desperately sell assets, which meant selling billions worth of non-mature Treasuries whose prices had tanked in the interim thanks to the Powell rate hikes.

(See how the Fed lurks, head down and silent, as the source behind nearly every crisis?)

This was selling bank assets at the worst time imaginable and immediately sent Silvergate into the red and toward the cold dark ocean floor.

Once DOJ investigations end and the FDIC insurance runs out, we’ll discover just how “whole” the bigger depositors at Silvergate will be—but this will take time and end in some degree of pain for many of them.

Death Valley for Silicon Valley Bank

As for the bigger disaster at SVB, they mostly serviced start-ups and technology firms with a major focus on life sciences start-ups—i.e., yesterday’s unicorns and tomorrow’s donkeys.

These unicorns, of course, were not only under the cloud of the FTX fears in particular and falling faith in tech miracles in general, but equally under the pressure of Powell’s rate hikes, which made funding (or debt-rollovers) harder and more expensive to obtain for tech names.

In short, the keg party of easy money for questionable tech enterprises was beginning to unwind.

SVB’s slow and then rapid demise came as depositors (at the advice of their VC advisors) withdrew billions at the same time, which SVB (like Silvergate) could not match after selling UST assets at a massive loss to save the first withdrawals while burning the later movers.

In short, and like all Ponzi schemes, banks suffering a bank run can’t and won’t make everyone whole—just the first money out—i.e., the fastest runners in the burning theater.

Burn Victims, Recovery?

Banks, ironically, can’t technically go bank-rupt. Silvergate plans to eventually make all depositors whole as they sift through their assets in liquidation. Hmmm. Good luck with that.

SVB, however, waited too long for voluntary liquidation procedures and was instead taken over by the FDIC as a receiver to manage the sale of assets to return investor deposits as a dividend over time.

Furthermore, the FDIC “insures” investor deposits up to $250K, but that won’t help the vast majority of SVB deposits (95.5%) not covered by this so-called insurance.

The Contagion Effect?

Notwithstanding the pain felt by depositors at Silvergate and SVB, the fear there has spread to the broader banking sector (big bank to regional), which saw expected sell-offs at the end of last week and has prompted the inevitable question, namely: Is this another Lehman moment?

For now, we are talking about bank runs rather than banks failing ala 2008 due to massive derivative exposures and bad loans. In short, this is not (yet at least) a 2008-like banking crisis.

That said, and as we’ve reported countless times, post-2008 banks are still massively over-levered and over-exposed to that toxic waste dump otherwise known as the COMEX and derivatives market.

Each day, the headlines change.

Signature Bank, this time in New York, was just shuttered by New York regulators.

The Fed then announced over the weekend that they will make depositors whole, which is tantamount to confessing yet another Fed bailout of bad banks under the new name of the $25B “Bank Term Funding Program”—or BTFP, an acronym which spurs reminders of the 2009 TARP days…

Such a bailout policy makes the odds of further Fed rate hikes in 2023 a bit less likely, and already the traders on Wall Street are renaming BTFP as “Buy The F***ing Pivot.”

As I’ve written for months (and show below), Powell’s QT plan would last until something inevitably broke, and it would seem that day has come, as expected.

Many are suggesting that the BTFB will need to be funded to at least $2T, not $25B, to backstop further banking risk.

Easy Prognosis

Based on context and current data, however, we can begin to make certain objective and early conclusions.

- Cash flow from VC into tech is about to get a lot tighter, as we’ve been warning for the last 2 years.

- SVB depositors may eventually get some or much of their money back over time once the bank’s assets (Treasuries, loans etc.) are sold off by the FDIC. Despite my very, very low opinion of bank regulators, at least SVB, unlike FTX, was regulated.

- As to a full-on crisis across all banks, it’s a bit early to say that the foregoing regional cancers will spread across all banks of all flavors, though our blunt reports on banking risk in the past suggest that banks as a whole are anything but safe.

- Cryptos, already under the cloud of FTX and now SVB, saw more pain, as the sell-offs in this space last week confirm. However, as banking fears prompt a more dovish Fed in Q2, many cryptos could rise.

The Bigger, Scarry Picture

In the still evolving nature of the current banking crisis, we see reasons to be concerned, very concerned, about systemic risk in the banking sector.

Banks, and banking practices, are complex little beasts. Just across town at that gasping entity known as Credit Suisse, for example, they have been too afraid to publicly report their cash-flow statements as the bank’s stock fell yet another 60%. So, yeah, things are complex…

But returning to the US in particular and banks in general, one can still derive the simple from the complex, which is simply scarry.

Keep It Simple

At the most basic level, banks fail when the cost of funding their operations rises dramatically above the returns or yields on their performing/earning assets.

It is our view that such a set-up for further pain across the banking sector is real, a set-up made all the worse by—you guessed it—that entirely un-natural destroyer of natural markets forces, free price-discovery and honest capitalism otherwise known as the U.S. Federal Reserve.

Central Bankers and Broken Bonds

As I’ve written and spoken, everything is connected, and everything eventually takes it signals from the bond market, which was long ago hijacked by the Fed.

Powell’s rate hikes, for example, don’t just occur in a vacuum to fight his bogus war on an inflation nightmare which he once promised was only “transitory.”

Fed QT and QE, for example, are more than just words, experiments or theories, they are un-natural, artificial and powerful toxins which can’t be contained to just making central bank balance sheets thinner or fatter and bogus CPI data higher or lower.

Instead, the Fed’s little tweaks, tricks and madness impact just about everything, and always end up screwing everything up.

Why? Because markets were designed to be managed by natural forces of supply and demand not artificial forces of fake money from central bankers.

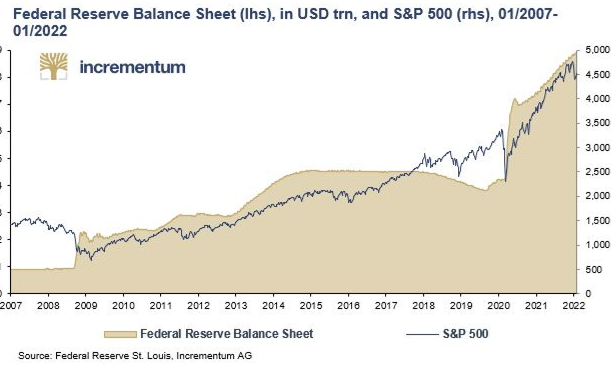

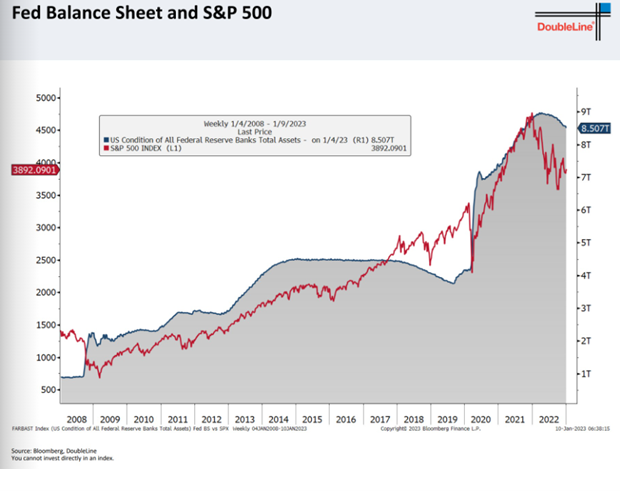

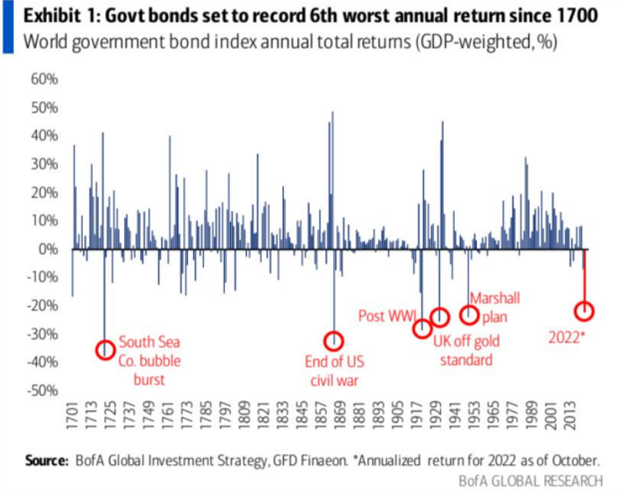

By raising the Fed Funds Rates toward 5% and above at rapid pace, for example, Powell has done more than just make a tiny $300B dent in the Fed’s nearly $9T balance sheet. He has engineered a dis-inflationary recession and sent combined nominal returns in stocks AND bonds to levels not seen since 1871.

But when it comes to banking risk, Powell has also gut-punched that sector with criminal negligence.

How so?

Even the Banks Can’t Fight the Fed?

When the Fed began raising rates, it sent bonds to the floor and hence yields to the moon (yields and bond price are inversely related).

This impacts bank balance sheets because banks make a living by paying depositors at rate X while earning X+; but now those banks are in a deadly corner of the Fed’s own mis-design.

That is, the Fed has sent bond yields higher than the rates/yields which commercial banks offer depositors, which is why many depositors are questioning the advantage of being, well…depositors.

This mis-match, of course, will likely require banks to raise depositor rates to compete with rising UST yields, a costly tactic which cuts their profits and reddens their balance sheets.

Alternatively, banks could offer/issue more bank shares to increase their capital, but this dilutes existing share counts and value, which is how bankers are paid.

To add insult to injury, banks (and bankers) are also facing the real risk of rising or at least persistent inflation, which means that the real return on even “enhanced” depositor rates is ultimately a negative return when adjusted for the invisible tax of inflation.

All Conversations Return to Gold

So, no, we hardly think the commercial banking system, the massive and compounding risks of which we have reported for years, is anything remotely healthy, safe or credible.

All frowns and inevitable (yet increasingly empty) gold-bug critiques notwithstanding, we think holding a physical bar of segregated, allocated and non-levered gold in one’s own name in the world’s safest private vaults and jurisdictions makes a lot more sense than trusting your increasingly worthless paper or digital money to the world’s increasingly fractured banks, be they SVB, Credit Suisse or JP Morgan.

Just saying…

Gold, Oil & Global Currencies Entering a Watershed Moment

Below we consider the State of California as the metaphor of a failed state as well as the failing state of the American Union, which is anything but a dream.

Metaphors

For those already familiar with my articles, interviews or even daily banter, I have an admitted affinity for metaphors and analogies, as they help draw the simple from the complex.

Toward that end, I’ve 1) compared policy makers to failed generals, 2) debt and currency bubbles to Titanics, 3) macro investing to polo matches, 4) monetary policy to drug addiction and 5) the love of bloated bond markets to toxic romances.

As for politicians and political issues, there is always the risk of partisan bias and offending those who cling to only one perspective.

Fortunately, my take on the left or the right of current politics is fairly agnostic, as I view nearly all politicos as crooked as a dog’s hind leg.

Thus, as I turn my lens toward the state of California and its failed governor, I hope readers of the left or right can dispense with politics and just stick to math so that we can all get past the swamp of red vs. blue opinions and respect the objective facts of red vs. black balance sheets.

And when it comes to the State of California, she’s deeply in the red, and serves, ironically, as yet another broader yet applicable metaphor of the world economy in general and the United States in particular.

So, let’s dig in.

California Dreaming?

Oh, how I have loved California. It is home to some wonderful personal memories as well as personal wipeouts—and not just the surfing kind.

Its sunny appeal, however, is universally seductive, and like that famous Eagles song, one indeed feels like you can check in any time you’d like, but you can never really leave California’s tempting horizons and mythical spell where dreams come true.

Nevertheless, folks are leaving California, and have been doing so to the tune of over 500,000 exits in the last 2 years alone.

Why?

For those on the political right, California’s big-headed Gavin Newsom is an easy target.

His over-the-top COVID hysteria (similar to other failed experiments in Seattle, Chicago or Portland…) and unsustainable tax policies coupled with San Francisco’s soft-on-crime nightmare (car-jacking capital) and L.A.’s recent fall from City of Dreams to Tent City are all classic symbols of a failed state.

I once lived on this beach…

But let’s leave that issue, debate and fall to the woke, the left, the right, the angry and the smug.

For me, the math of California (whose nominal GDP ranked as the 5th largest in the world) makes the discussion far easier to sift through.

The Hard Reality of Simple Math

Like nearly all cornered politicians, Newsom is driven by obfuscating the obvious and trivializing the momentous (Chicago’s recently failed mayor of the nation’s “murder capital” comes to mind…).

For example, his January projected budget deficit of $22.5B (an already embarrassing figure which he nevertheless tried to downplay) was in fact off.

Way off.

It turns out that even Newsom’s “sunny” forecast and optimistic math had overlooked a few pesky facts.

First, the state’s monthly tax revenue for January was almost $14B less than the revenue for the month prior.

Secondly, California’s fiscal year, which started last July, is moving at a pace of $23B in less income than the previous year.

In short: California’s income stream is running toward an emptiness equivalent to Newsom’s IQ, despite sunsets as consistent as his immaculate wardrobe and “Hollywood” smile (smear?).

But as many Californian’s know—it’s not how things feel, but how they look which counts.

For the top income bracket, however, California’s tax bills (and revenues) aren’t looking good.

Even those wealthy and beautiful (from Topanga to Belvedere Island) are starting to squirm under a state tax structure that feels and looks anything but “dreamy.”

State tax for Californians earning over $1M is 13.3%, and the top 0.5% of California’s tax payers are responsible for over 40% of the state’s total tax income.

Many, of course, are getting sick of paying taxes for increasingly expensive sunsets, even from Orange County’s row of waterfront mic-mansions.

Furthermore, for those wealthy left-coasters who’ve lost their jobs or capital gains at Google, Amazon, Facebook and countless other Silicon Valley enterprises of late, that tax income is openly drying up, which means so are the state’s revenues.

Fantasy Land

California, of course, is home to Hollywood and fantasy-like conversations of making dreams come true over cocktails at Shutters on the Beach or an overpriced vegetarian meal at The Ivy.

Fantasy, of course, is fun, and even necessary at times. (I always loved Shutters…)

It was fantasy, for example, that made an Austrian body-builder into a former Governor of California. How’s that for the American/Californian dream?

Unfortunately, that same Austrian never studied Austrian economics in between barbell sessions, and the last time I heard him speak, he was saying “screw your freedom,” suggesting that the unvaccinated were all anti-science “schmuks… “

What a guy. What a dream.

But had some of Cali’s former leaders indeed studied any form of economics, they’d likely understand that rising deficits and falling revenues is the opposite of a dream—it’s the historically-confirmed prelude to a nightmare.

Even the once-reliable WSJ has confessed that California’s budget has imploded and that January revenues are poised to be down by 40% y/y.

Uh-oh?

One wonders how long the top 0.5% of California will want (or be able) to pay that ever-increasing bill as profits in their tech-heavy portfolios creep ever closer toward a cliff steeper than Malibu’s Point Dume.

Fantasy Politics—Lipstick on a Pig

In the interim, Californian leadership sure knows how to put lipstick on a pig.

They’d tell us, for example, that despite revenues falling from prior peaks, that the state expects revenues for 2023-24 to “remain about 20% higher than before the pandemic.”

In other words, nothing to worry about.

Really?

First, those “projections” already have a ring of good ol’ Californian fantasy to them.

But even if we assume they are accurate and that California’s “revenue problems” are solved, those same budget wizards are ignoring the spending (i.e., the aforementioned budget deficit) problem which is mounting.

California as Metaphor

Unfortunately, California’s embarrassing combination of tanking revenues, increased spending and expanding deficits is not happening in a vacuum.

In fact, California serves as a mirror to a broader problem within the United States as whole (or debt hole) …

Like the failed state of California, the equally failed state of the US government has a problem with incoming tax revenues, an issue I’ve been tracing throughout 2022.

Like the Californian wealthy 0.5%, the wealthy 1% of the United States taken collectively are the ones paying 40% of the national taxes.

And like California’s wealthy in general, the nation’s wealthy in particular get a lot of that wealth from a bubbling risk asset market whose best days are largely behind us and whose worst days (and hence weaker capital gain receipts) are still ahead.

In short, and like California, the United States is facing less tax revenues combined with greater deficits and increased spending, making the Cali crisis a leading indicator of a national crisis.

The Math of Recessions

Recessions, even the kind the DC crowd seeks to redefine, deny, postpone or ignore, have patterns and facts which we can use to foresee coming trends, weaknesses and even opportunities.

For example, recessions mean less tax receipts and higher deficits.

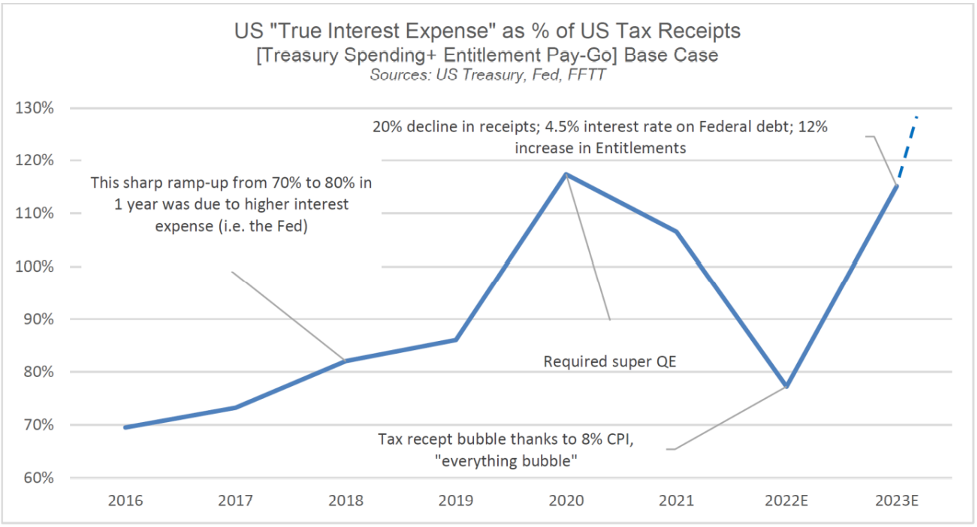

If we assume even a 20% decline in tax receipts (conservative), tagged on to rising deficits estimated at a 12% increase in Entitlement Pay-Go’s (also conservative) in the backdrop Powell’s current rate hike policy, Uncle Sam’s bar tab (i.e., True Interest Expense) returns to Covid crisis/pain levels reminiscent of a seemingly forgotten yesterday:

In other words, the United States (along with California…) are mathematically heading toward a bar-tab (i.e., interest expense bill) as painful as the one we saw in March of 2020, when markets tanked and the Fed was required to print trillions in less than 8 months just to keep Uncle Sam’s nose (and Treasury market) above water.

For now, however, the Fed is not printing trillions via QE, but tightening ala QT.

Or stated more simply, US debt obligations are sailing toward yet another debt iceberg, only now the issue is not about too few lifeboats, but no life boats at all.

As I see it, and have said many times prior, the US is trapped with no easy solutions as debt levels are rising and revenues falling.

The end result is obvious, even if the precise timing of the iceberg is not.

Whether Powell’s Fed continues to tighten into a debt iceberg, or eventually seeks to temporary melt (monetize) that iceberg with more QE, the nation is doomed either way in a Hobbesian choice between tanking markets (QT-driven) or skyrocketing inflation (QE-driven).

No One Likes Bears, and Even Fewer Understand Gold

Unless you are a talented short-trader or volatility option jock, no one likes bears or bear markets, and hence very few like to hear data-driven bears (mathematical realists) like myself constantly reminding us of the debt elephant in the room–and all that this toxic debt inevitably implies.

Once debt levels become fatal, the direction of credit, stock, property and finally currency markets are easy to diagnosis, though the time of death is not.

Gold, of course, loves dying currencies.

The price of gold today, or the strength or weakness of the USD tomorrow, are frankly silly questions in the short term for any who understand the broader context of the long-term.

Currencies are always the last bubble to pop, and given that gold is a store of value rather than an instrument of speculation, gold investors (i.e., those whose aim is wealth preservation not asset speculation) recognize that gold never rises, currencies just fall.

Investors in physical gold therefore measure their wealth in ounces, grams and kilos, not highly toxic, increasing debased and (forever debated) fiat currencies whose race to the bottom is literally happening right before our eyes in real time.

To dismiss such simple deductions from admittedly complex market forces as just “gold bug” thinking ignores math, history and gold cycles.

But again, no one likes to see bears, even when they’re staring at them from the Californian state Capital.

Based on all the debt destruction (and coming consequences) I see in California, the United States and the world in general, I suppose I’ll still just be a “bear” and a “bug” to most.

But both are better than a sitting duck.

Gold, Oil & Global Currencies Entering a Watershed Moment

Below we examine the historical interplay of losing wars, cornered egos, tanking currencies, greater controls and gold’s loyalty in times of open madness.

History Matters

Despite the fact that universities even in the Land of Lincoln have had a say in cancelling Abraham Lincoln (good grief…) for apparently not being “woke” enough circa 1861 to be as wise as the neo-liberal faculties of 2023, I’d still make a case that history matters, and by this, I mean all its wonderful and ugly nuances (and lessons), whether they offend modern sensibilities or not.

History, of course, is full of desperate figures and times, many of which involve desperate economies followed by equally desperate (proxy) wars and desperate turning points.

In this light, the more things change, the more they stay the same. Just look around you…

And in the largely forgotten history of war, there is no shortage of desperate generals at desperate turning points.

Wars Doomed from the Start

Napoleon, who having previously won countless battles from Rivoli to Austerlitz, found himself shivering through an 1812 Russia after losing the vast bulk of his army to General Russian Winter and remarking to one of his generals that it’s “only a fine line between the sublime and the ridiculous.”

Three years later, at Waterloo, Napoleon’s “sublime” days (and countless casualty numbers) ended for good.

At Gettysburg, on the 3rd day of July, 1863, an equally talented and grossly outnumbered Confederate States Army under Robert E. Lee, having humbled Union forces at Manassas 1 & 2, Fredericksburg, Gaines Mill and Chancellorsville, looked across an open field from Seminary Ridge to the Emmitsburg Road strewn with the dying and dead of his once bravest divisions as the U.S. Civil War reached a mathematical turning point.

Despite this carnage, the war (post Pickett’s doomed July 3rd charge) dragged on for 2 more horrendous years (and countless casualty numbers), ignoring the hard math of waning troop numbers, supplies, cannons and horses which now rendered Southern “victory” impossible.

Less than a century later, this time near Stalingrad in the winter of 1943, the seemingly invincible German Wehrmacht, having conquered Poland, France, North Africa and large swaths of the East, found itself (and General von Paulus) facing the equally mathematical reality of what once seemed like impossible defeat.

By all metrics the Germans, having engaged in a two-front war, were done, but the war (and countless casualty numbers) would continue for two more senseless years.

But what do any of these examples of doomed and costly wars have to do with current global markets and our financial “generals”?

In fact, quite a bit.

Financial Policies Doomed from the Start

The overlapping interplay of human ego, hard math, and failed strategies doomed from the start have their place in both military and financial history.

For example, once upon a time (circa 2008), our central bankers in general, and the U.S. Fed in particular, had the insanely bad idea that central banks could use fiat money created out of thin air to save bad banks, defeat recessions, manage inflation, monetize debt, win a Nobel Prize and ensure total employment with a “Pickett’s charge” of mouse-click money.

Such grand plans, like the promises of failed generals and insane wars of Lebensraum, la gloire de l’empire or the “Southern Cause,” were initially followed by a string of early “Austerlitz-like successes” (i.e., market bubbles) which brought near-term euphoria.

Unfortunately, those early and mouse-clicked victories ignored the longer-term realities/casualties, namely: historically unprecedented wealth inequality, grotesque currency debasement, the death of free-market price discovery and the birth of what amounts to little more than Wall Street socialism and market feudalism masquerading today as MMT “capitalism.”

Such short-term “glory” at the expense of longer-term ruin is a pattern all too familiar for those paying attention…

Emperor Powell, for example, thinks he can “win the war against inflation,” but like Napoleon, Lee and von Paulus, he is still unable to admit to himself (or us lieutenants) that his grand vision is doomed either way.

And so, he continues to desperately fight a losing cause at the expense of countless currencies and investors (casualties) around the world.

How can we know this?

It All Boils Down to Hard Math and Bad Options

As detailed in prior reports, the math speaks for itself.

Global debt levels are past their “Gettysburg moment”—there are no easy victories left once we start dealing in the quadrillions…

Whether Powell continues with QT or pivots to more QE, retail foot-soldiers here and abroad face either economic recession/depression or extreme inflation.

Pick your “victory” or your poison. I see both, namely: Stagflation

Equally serious is the inevitable demise of the USD’s purchasing power at home and the slowend of its hegemony in the world.

The Sad Fate of the USD

Regardless of whether the USD (DXY) rises or falls in the near-term, the end result is as inevitable and mathematical as Germany’s two-front war, Pickett’s charge or Napoleon’s Waterloo: Disaster.

Once stock and bond bubbles reach their tipping points, the last bubble to die is always the currency, which is precisely where our prize-winning (?) central bankers have placed us.

In short, and as shown below, the global economy and USD, led by Field Marshall Powell, is about to cross that infamously fine line from the sublime to the ridiculous…

The USD’s Sublime Last Moments

As in any losing war, however, there are always those clinging for hope, including those who think the USD will never, well…surrender. (In 2022, the British pound, the yen and the euro already caved…)

Recently, for example, the headlines, politicos, markets and perma-bulls were positively giddy over the stronger than expected US jobs report and non-farm payroll data. The DXY climbed in lock-step.

However, what was equally higher (60% higher…) than expected was the 2023 US Treasury borrowing estimate –aka: Uncle Sam’s increasing bar tab–$930B! –for Q1 alone.

Each of these data points has sent the USD temporarily higher, along with inflation expectations, which now seem to be embedded.

So, the big question today is this: Will the USD get stronger or weaker in 2023 and beyond?

There are two camps in this strategic debate, and two consequences depending on which camp is right. Neither are “victorious.”

Bad Scenario 1: A Rising Dollar’s Consequences

If the USD gets stronger, it kills just about every asset class but the USD…

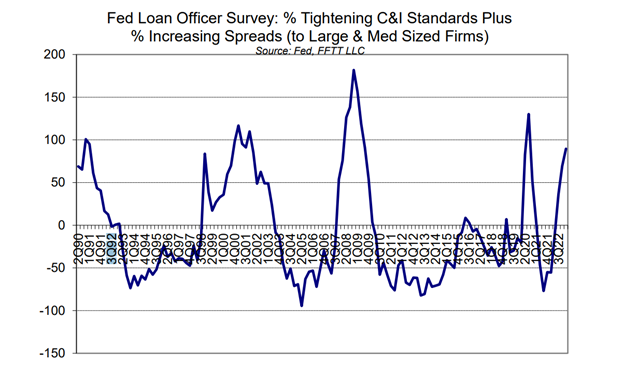

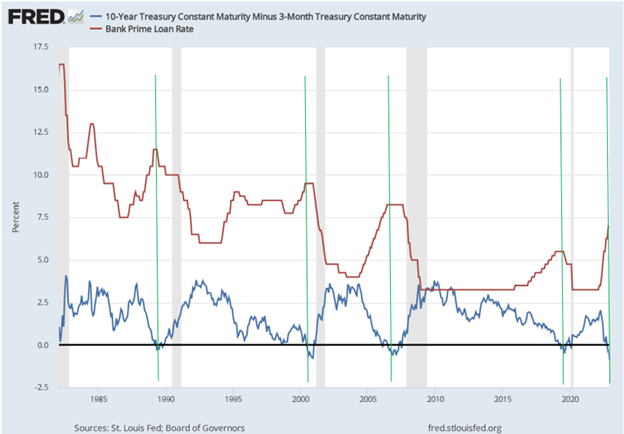

Already, we are seeing this open carnage in credit markets as rising rates and General Powell’s strong-Dollar policies cripple lending and borrowing norms of the past.

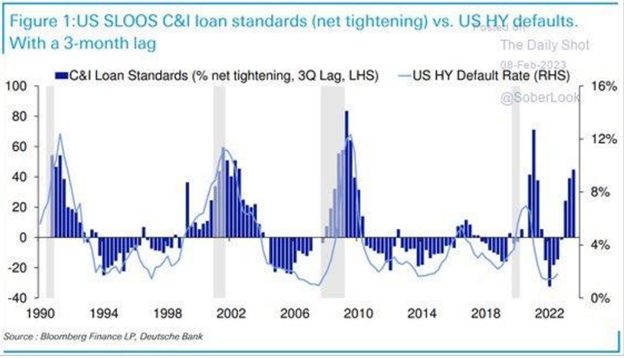

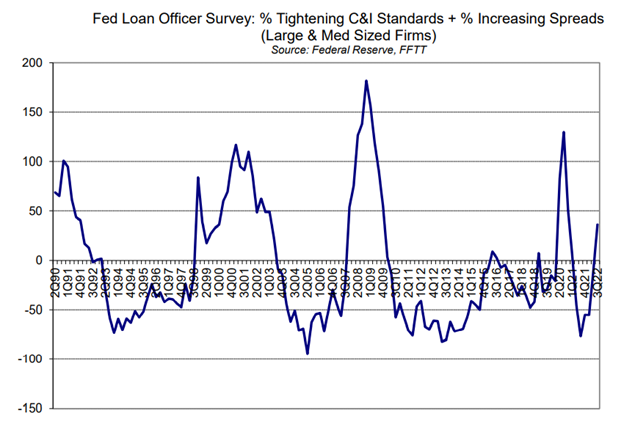

Loan officers are confirming a tightening of credit availability (and a widening of bank lending spreads, above) at levels only seen in prior recessions, adding more weight to my ongoing contention that the US is already in a recession, despite every Göbbels-like attempt in DC to redefine, cancel, ignore or downplay the same.

The equally dismal rise of defaulting High Yield bonds adds further proof of the slow (then steady) death of bleeding bonds in a rising rate and strong USD backdrop/policy.

A strengthening USD will send bonds down and hence yields and rates higher, which will be deflationary as debt-soaked America gets poorer and foreigners are forced to sell more USTs alongside a tightening Fed which is doing exactly the same thing—namely: Bond dumping and yield-spiking.

Bad Scenario 2: A Falling Dollar’s Consequences

However, if the USD gets weaker, the inflation we are already feeling will only get worse as $2T+ deficits make their steady climb North toward $3T, $4T or even $5T+ for 2023.

So, once again: Will the USD get stronger or weaker?

The answer lies in what signals (or desperate generals) you track or trust: Powell’s Fed or the UST market?

Trust What Powell SAYS?—Strong Dollar Ahead

If, for example, you follow the Fed and its bogus yet deadly-serious inflation narrative, then you will be lured into Powell’s “we must beat inflation” war cry, which boils down to a zero-sum battle-plan of “high inflation bad, low inflation good. Must beat inflation.”

Equally part of this bogus battle plan (Powell needs inflation and negative rates…) is the courageous meme that “rising rates kills inflation.”

Well… yes, but at what cost?

If Powell wins the headline battle against inflation, he loses the war for global credit markets, economies and political credibility, which loss will be immediately blamed on a virus and Russian bad guy but never on the mad generals who pushed us over the debt cliff.

However, if we get beyond linear headlines and two-dimensional thinking of central bankers like Powell, we quickly realize that the 3-dimensional UST market is perhaps the real (and superior) indicator of future probabilities.

Or, Trust What Bond Markets DO?—Weaker Dollar Ahead

Thus, rather than watch the Fed, I’m looking at bond markets to get my directional compass-North in a world of policy cannon smoke.

As said more times than I can count: The bond market is the thing.

And as for the sovereign bond market, it has seen 3 periods of complete dysfunction in recent years, namely: 1) the repo rate spike of September 2019; 2) the March 2020 “Covid” crash, and 3) last October’s gilt implosion spawned by the rising USD.

Those who follow the Fed (and this is entirely understandable given that the Fed IS the market in our post-2008 centralized nightmare) can’t be blamed for therefore expecting the USD to rise on more tightening and Powell “inflation-fighting.”

But those who follow the Fed are also ignoring those 3 bond market cracks in the ice above.

It’s my view that this ice is about to break if we have a 4th “uh-oh” moment/crack in sovereign bonds.

Thus, rather than follow the Fed, we might be wiser to look at the UST market, which is heading precisely in that “uh-oh” direction unless someone (i.e., Yellen?) pushes another meme—namely more toxic liquidity and thus a weaker USD.

But as previously argued, either way we are doomed…

Failed Battle Plan 1: Tightening into a Debt Crisis (Stronger Dollar)

Let’s play out the Fed’s current scenario first.

If we look only at what the Fed says, and it tightens, which, for now seems like the plan for Q1 and Q2, the USD will strengthen, yields and rates (5% to 5.25%) will rise further and the UST market will see such a wave a selling (foreign and QT Fed-driven), that a fourth “uh-oh” moment in the sovereign bond market will be inevitable, and likely enough to not only “crack the ice” of global bond markets, but drown everyone skating above it.

Given these realities and risks in the UST market, risks which even a fork-tongued and totally cornered Jerome Powell understands, I see no realistic way forward other than a weaker USD and thus a move from QT to QE.

Why?

Again: Because I’m taking my signals from the bond market not Powell.

To track (and trust) Powell means a tanking US Treasury and fatally rising rates, which is like kryptonite to America’s debt-based “accommodation” model.

Instead, I believe Powell will be forced to strategically consider the fact that this inflation war has killed his army of USTs and hence force him (at Yellen’s direction) to change tactics.

Or stated more simply, just as Napoleon, Robert E. Lee, and even the Wehrmacht learned that no outnumbered army can win an extended war, Powell will discover that no sustained policy of rising rates can end well for the toxic bonds/IOUs which float a bankrupt nation.

In short: Unless Powell weakens the USD and injects more QE liquidity sometime in 2023, his victory over inflation will be at the expense of America’s life-blood—namely the UST market.

Failed Battle Plan 2: Resort to More Mouse-Click “Miracles” (Weaker Dollar)

At the end of the day, and despite all this “beat inflation” rhetoric from Powell, it is my admittedly contrarian and unpopular (don’t say “gold-bug”) view that saving Uncle Sam’s IOU lifeline (i.e., the UST market) will take strategic priority over “beating inflation.”

By the way, this appears to be a view shared by none of other than that Corps Commander of toxic liquidity herself: General Janet Yellen…

In other words, expect an eventual (not immediate) capitulation to more fake money—aka, QE, i.e., “liquidity.”

This means that despite gyrating USD moves and hence DXY flip-flops today, the only direction and choice in the longer term to beat a recession and save Uncle Sam’s IOUs is a weaker not stronger Dollar.

Ultimate End-Game? Blame, Reset and Centralized Control

A weaker USD will buy time (and USTs) until ultimately the developed economies of the world, which in fact have the balance sheets of banana republics, finally realize that there’s still nothing left to save them but a great big “reset”—i.e., a global Chapter 11 or Economic “Versailles Treaty.”

The need for this “re-set” will, of course, be conveniently blamed on Putin and Covid rather than the central bankers (failed generals) who caused this horrific war on real money, sustainable debt and sound fiscal spending years ago.

At that point, history will remind us that lost wars and failed policies always devolve into more centralized controls masquerading as governmental “guidance,” payment efficiency and “democratic” leadership, nicely encapsulated in that toxic new direction of Central Bank Digital Currencies and a more Orwellian new normal…

But I digress…

How to Position Yourself?

Switching from military to equestrian metaphors, I argued in 2022 that investors, like polo players, need to think where the ball is headed, not where it lies currently.

Regardless of what Powell says today, the real play is 3 to 4 moves ahead, which all point toward an inevitably weaker USD and thus an inevitably rising gold price.

Powell, of course, is more politician than economist, and central banks like the Fed are anything but independent.

As such, Powell, DC and the creative math and fiction writers at the BLS will continue to do what all politicians (or losing armies) do when things are going against them: Lie.

Thus, the DC creative writers will continue to fudge, distort and “tweak” the CPI data to mis-report true inflation as nearly “beating expectations,” thereby allowing Powell to save face in a losing “war against inflation” while Lieutenant Yellen quietly pushes a weaker USD narrative to save the UST market (i.e., prevent more foreign UST dumping).

This face-saving policy will then allow the US to do what it does best: Borrow, spend and go deeper into inflationary debt spirals.

The Pesky Human Factor

Based on bond market Realpolitik, the probabilities point toward a liquidity pivot and weaker USD, longer term.

But history also reminds us that power-drunk figures don’t like to admit defeat. Their egos get in the way of rational decisions.

Powell, who desperately wishes to be remembered as a Napoleonic Paul Volcker rather than a comical Arthur Burns, is no exception to such human-all-too-human small-mindedness.

Unwilling to accept a Gettysburg moment that originated with Colonel Greenspan, General J. Powell could indeed push too far and too long with rising rates, a stronger USD and tanking bonds until inflation and everything else is destroyed.

We can only wait and see.

The Gold Factor

Whether on battlefields or economic cycles, man’s history of the absurd and his disloyalty to the many for the benefit of a few is nothing new under the sun.

In short, chaos eventually rears its head.

Powell or Yellen, QT or QE, inflation to deflation, left or right, Davos or DC, the chaotic results are always the same: Currencies and markets die, opportunists, lies and controls increase and the little guy (and common sense) gets trampled, drafted or “cancelled.”

Physical gold, of course, loves chaos and offers far greater loyalty to those who put their trust in this natural metal rather than flimsy paper money and the even flimsier promises from on high.

So which form of money will you trust to preserve your wealth?

A digital and speculative “coin” promoted by human cons that is anything but stable?

A fiat currency that is losing its purchasing power by the second?

Or a naturally finite monetary metal with infinite duration born from the earth rather than an anonymous code writer or over-heating printer?

The choice, of course, is yours.

Gold, Oil & Global Currencies Entering a Watershed Moment

Below we look at the interplay of embarrassing debt, dying currencies and failed monetary fantasies masquerading as policies to confirm that no matter how one turns or spins the inflation/deflation, QT/QE or recession/no-recession narratives, the global financial system is already doomed.

Recession: The Elephant in the Room

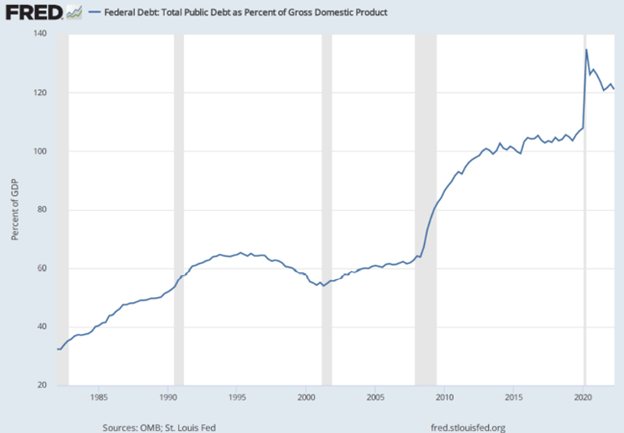

As I’ve been arguing in report after report, my view has been that the US, with its 125% debt-to-GDP and 7% deficit-to-GDP ratios, was, and already is, in a recession heading into 2023, despite official efforts in DC to re-define the very definition of a recession.

But a recession is still a recession, and an elephant is still an elephant, and both are fairly easy to see at a distance.

As of now, however, the recession has officially been avoided.

How comforting.

As with the inflation data, it’s nice when the folks in Washington can exercise their magical powers to move the goal-posts in mid-game whenever a little “cheating” helps their odds and fictional narrative.

For me, an elephantiac recession is now in the room.

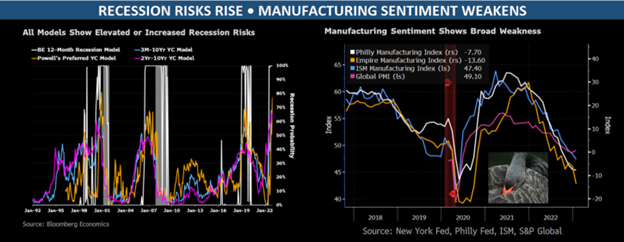

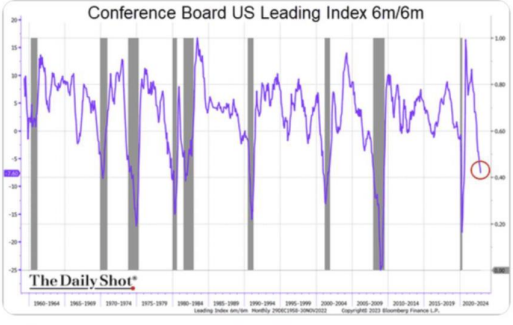

The Empire Manufacturing data in my latest report, for example, supported this recessionary outlook.

In case, however, we still need more recessionary evidence, the dramatic 6 month decline in the Conference Board’s index of leading indicators serves as yet another neon-flashing warning that the recession—if not under our bow—is certainly right off our bow.

Still Hoping for a “Softish” Landing?

Furthermore, and despite Powell’s belief that his office can manage a recession with the precision of a home thermostat, his faith in what he lately described as a “softish landing” is almost as farcical as his prior attempt to describe inflation as “transitory.”

Without wishing to appear “sensational,” as many of us blunt and math-based observers (from Burry to Middelkoop) of late are described, I will stick my tin-foil-covered head out and say candidly that I see nothing “softish” ahead.

Instead, I see either: 1) a financial crisis which will dwarf 2008 and/or, 2) an absolute tanking of the USD, whose unsustainable strength throughout 2022 was indeed “transitory,” as I argued numerous times.

The Simple Math of Liquidity

The simple math and reality of even centralized and central-bank distorted markets is quite simple: These markets rise and fall on liquidity.

Once the monetary “grease” required to maintain the MMT fantasy of mouse-click money as a debt solution “tightens” too tight or runs too dry, the entire house of cards of the post-2008 fairytale comes to a hard rather than “softish” end.

Again, we saw the first signs of this collapse in the “tightening” backdrop of 2022.

Of course, this critical “liquidity” won’t be coming from economic growth, rising tax receipts, a robust Main Street or a fairly-priced market.

Instead, and as expected, it now comes from out of thin air…

Is It a Race to the Bottom for Risk Assets?

The honest but scary numbers rather than fluffy but fictional words of our financial central planners make it all too clear that unless Powell puts his finger on the Eccles-based mouse-clicker to create more fiat money (highly inflationary), US and global credit markets will simply continue their race to the ocean floor (highly deflationary or at least dis-inflationary).

As credit markets sink and bond yields and rates rise, this also means that equity markets, who have been sickly addicted to years of central-bank repressed low rates and cheap debt, will merely join those bonds on the bottom of the dark ocean floor.

In short, bonds (and hence risk parity portfolios) won’t save you. Rather than hedge stocks, they are now correlated to the same.

More Easing Won’t Bring “Ease”

Failing outright and open bond default, it thus seems that an eventual capitulation to more magical “liquidity” and renewed QE is nothing short of inevitable, which means the USD’s fall from its 2022 highs is equally the case, as shown below.

But such “easing,” if realized, will lead to more inflationary-debased Dollars and hence more inflation dis-ease for investors.

This is hard for investors to fully grasp when the Dollar seems “strong,” but even that was an illusion, and one which hardly did any asset class any good in 2022 but for the Dollar itself.

The Damage Already Wrought by the Strong USD

In the interim, the cancerous ripple-effects of the Fed’s strong USD policies, as warned throughout 2022, continue their waves of destruction, as openly evidenced by the earnings reports from our beleaguered S&P.

Already, the early data coming from its listed companies is anything but positive.

As in the July and October earnings seasons of 2022, corporate earnings for 2023 are still drowning under the weight of the USD.

But we must also keep in mind that the DXY (which measures the relative strength of the USD) has fallen 11% (from 113.9 to 101.8) over the last quarter.

If the S&P hit an October bottom during a DXY high, what can we deduce from a now falling DXY?

Will markets rise like Lazarus?

This will be something worth tracking.

But why?

Strong Dollar or Weak Dollar, No One Wins…

Should earnings and hence stocks continue to decline despite the DXY declines, this would suggest that not even a weakening USD can save these post-08, over-stretched, Fed-addicted and debt-soaked markets.

However, should stocks rise on a weaker Dollar, the percentage gains in price will only be eaten away by the invisible tax of inflation and the increasingly debased value of the very dollars used to measure those so-called “appreciating” stocks.

In short, a no-win scenario…

For now, it seems the stock market only cares about the Fed rather than the DXY, as the Fed is the market.

That is, when QE is the meme, zombie markets rise; when QT is the meme, they fall.

Again, see for yourself:

Yellen, Squawking for a Weaker Dollar?

In fact, it was during those October market lows that the queen of toxic liquidity, former Fed-Chair-turned-Treasury-Secretary (imagine that?) Janet Yellen, was suddenly ringing the bell for more magical money—i.e., “liquidity.”

Specifically, Yellen was wondering who would be buying Uncle Sam’s IOU’s without more mouse-click money from the Eccles Building?

As my latest reports on the UST markets confirmed, the answer was simple: No one.

Instead, foreign central banks were and are selling rather than buying America’s bonds. Just ask the Japanese…

Is Yellen, contrary to Powell, silently suggesting that QT has backfired? Is Yellen, unlike Powell, realizing that there are no buyers for our increasingly issued yet unloved USTs but the Fed itself?

Perhaps these tensions within the Treasury market provide the hidden clues as to why the USD has been sliding rather than rising from the DXY’s October highs?

After all, a weaker USD means less forced need for foreign nations to dump their UST reserves to come up with the money to buy their own dying bonds and strengthen their own dying currencies as a direct response to Powell’s (and originally, Yellen’s) strong USD policy.

In short, perhaps our Treasury Secretary now wants to stop the bleeding in her Treasury market…

Weaker Dollar Ahead?

My current view is therefore this: We are seeing the slow end of the strong USD policy.

Why?

Because as warned throughout 2022, such a strong USD was a massive gut-punch to foreign currencies and hence foreign holders of USD-denominated debt.

Indirectly then, the strong USD was also a gut-punch to the UST market, which saw more sellers than buyers around a crippled globe. Hence Yellen’s backfired and back-stepping fears above…

Furthermore, and returning to the aforementioned topic of recessions, I also argued throughout 2022 that no recession in history has ever been solved with a strong currency.

Given that such a recession is, again, either directly off our bow or already under it, it is likely no coincidence that the USD/DXY is now falling rather than rising.

In short has Uncle Sam’s strong Dollar finally cried, well… “Uncle”?

Or more simply stated, has Yellen realized, in private, what we’ve been arguing in public, namely: That we are already in a recession and thus need a weaker Dollar.

Powell: Ignoring Reality & Yellen?

Meanwhile, however, you have the math-challenged but psychologically tragic Jay Powell wanting to save his legacy as a Paul Volcker rather than as an Arthur Burns.

Like a child wanting to be John Wayne rather than Daffy Duck, Powell and his rate-hiked strong USD refuses to see the $31T debt pile in front of him which makes it impossible to be a reborn Volcker, who in 1980 faced a much smaller debt pile of $900B.

In short, Powell’s America of 2023, unlike Volcker’s America of 1980, can’t stomach rising rates or a strong USD.

Or stated even more simply: Powell can’t be Volcker.

Will someone at the Eccles Building please remind him of this?

Doomed Either Way

Yellen or Powell, QT or QE, strong Dollar or weak Dollar, the global financial system is nevertheless doomed.

We either tighten the bond and hence stock markets into a free fall and economic disaster, or we loosen and ease liquidity into an inflationary nightmare.

As I’ve said so many times: Pick your poison—depression or hyperinflation.

Or perhaps both…namely stagflation.

Either way, of course, Powell, and the American economy, is now doomed. And he has only Greenspan, Bernanke, Yellen, himself and years of mouse-click fantasy to blame.

Supercore (CPI) Lies from On High

Meanwhile, the lies, twisted math and Nobel-Prize level mis-information continues…

Last week, for example, I reminded readers of DC’s latest attempt to mis-report otherwise humanly-felt inflation by tweaking an already-tweaked (i.e., bogus) CPI inflation scale.

But if that comedy wasn’t already comical enough, now welcome none other than Paul Krugman to this stage of open theatrics masquerading as economic data.

According to one of Krugman’s latest neoliberal economist tweets, “3-month ‘supercore’ CPI is below Fed’s 2% inflation target,” which naturally had those equally raggish economic playwriters at the WSJ almost galvanic with theatrical “good news.”

Hmmm.

What neither Krugman nor the WSJ seemed to recognize is that “supercore” CPI excludes food, energy, shelter and the price of used cars, so yes, absolutely, if you take away all the things that actually cost lots of money, inflation is no problem at all… Bravo!

Such shameless misuse of data and headlines, of course, is almost as shameless as the misuse of monetary policy we’ve been enjoying since the Troubled Asset Relief Program…

But as stated last week, such desperate tricks from on high will continue to mount as global financial problems do the same.

An Historical Turning Point

The astounding lack of accountability from the foxes guarding our financial hen house will one day be the stuff of history books, assuming history itself is not cancelled, as it seems the study of economics has already left the room.

The best we can hope for from the very “experts” who have brought the global economy toward a mathematically unavoidable cliff are now empty words and twisted math, as per above.

Such disloyalty from our financial generals on the eve of an unprecedented strategic and tactical economic defeat of their own making reminds me of officers sitting miles from the trenches as investors go “over-the-top” toward a row of cannons pointed straight at their trusting chests.

In short: Sickening.

Gold: A Far More Loyal Lieutenant

Gold was a far more loyal asset than stocks and bonds in the turbulent times of 2022; and given that 2023 portends to be even worse, we can expect better loyalty from this so-called “barbarous relic” of the past.

With inflation ripping and war blazing, many still argue that gold did not do enough.

Hmmm…

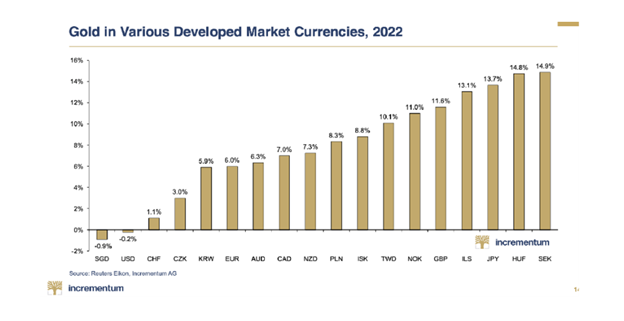

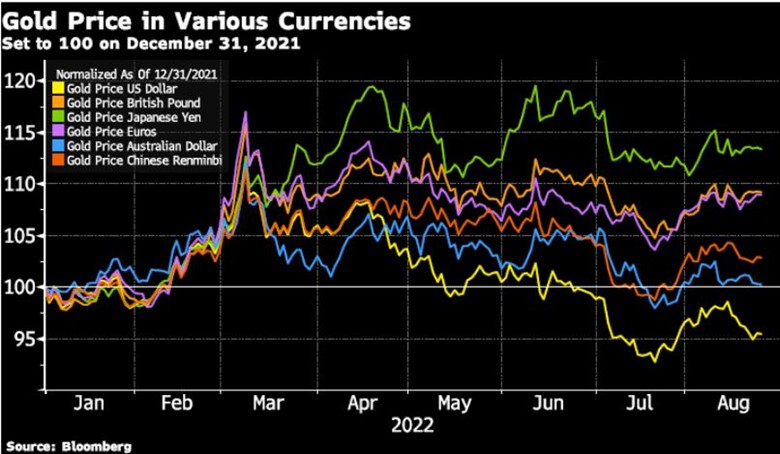

But gold in every currency but the USD (see above) would beg to differ.

Furthermore, and as argued so many ways and times, that USD strength will not hold, as gold’s price moves this year have already tracked.

Gold’s future strength and rise is thus easy to foresee, as gold doesn’t rise, currencies just fall.

It’s really that simple.

Got gold?

Gold, Oil & Global Currencies Entering a Watershed Moment

Below, we consider a blender of history, simple math, sober facts and comical arrogance to better understand gold’s loyalty in a time of disloyal financial stewardship.

Hubris Comes Before the Fall

History (whether on battle fields or sports fields) is riddled with tragi-comical examples of human blundering (and hubris) in the face of otherwise obvious and self-inflicted risk—you know: The final swagger just before imminent defeat.

Remember “Mission accomplished”?

Like well-dressed officers steaming the Titanic at full speed ahead despite repeated ice warnings, the arrogant yet misguided faith our central planners/bankers have in their “unsinkable” financial (i.e., Keynesian) models and verbal platitudes is astonishing.

If the financial model, for example, says “raise rates to fight inflation,” then the model must be right—especially given the credentials of our elite “model followers,” all collectively swimming within an echo-chamber of model-making, yes-saying, self-selecting and PhD-affirming back-slappers from MIT to Stanford, U-Chicago to Harvard Yard.

Linear Models & Thinking in a 3D World: Fantasy vs. Complexity

Yet such singularity of purpose and linear thinking (recently exemplified by openly failed COVID vaccine “models” and backfiring Putin sanctions) in an otherwise three-dimensional backdrop of ignored complexity theory reveals a staggering incapacity among our so-called policy-leaders to consider the side effects (and astonishing collateral damage) of such singular goals—such as “defeating inflation.”

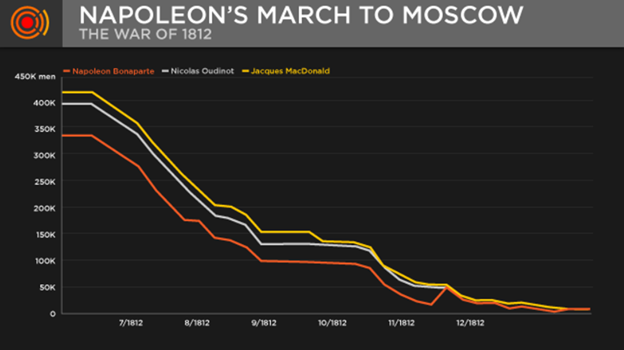

Just like Napoleon’s war (and singular focus) against the Russian Tzar in 1812 ignored the subtleties of cold weather and the panache of the Cossacks, resulting in the destruction of his Grande Armee as graphically seen here…

…the Fed’s 2022 war (and singular focus) against inflation has equally ignored the subtleties of budget deficits, currency expansion and the panache of natural market forces, resulting in the destruction of the all-mighty USD’s purchasing power as graphically seen in almost identical fashion here:

In short: Powell is missing the bigger picture.

At a recent Brookings Institute presentation, for example, a mathematically cornered J. Powell repeated his heroic aim to defeat inflation (which the year before he claimed was “transitory”) and bring CPI levels back toward the carefully-modelled 2% range.

That’s all very Napoleonic, but what a linear-thinking Powell deliberately failed to consider in his tough-talk included some other critical, percolating yet ignored 3-dimensional themes (and alternative/ignored facts) of economic Realpolitik, namely a string of crises (icebergs) relating to balance of payments, fiscal expansion, debt destruction and currency risk.

Free Advice to Expensive Leaders

Perhaps one of Powell’s sub-lieutenants ought to remind him of some of the following tactical considerations (i.e., hard realities) which the Fed has missed in its “blinders-on” effort to defeat inflation via rising rates.

In other words, here’s some free advice and timely reminders of what central bankers like Powell might want to consider, namely:

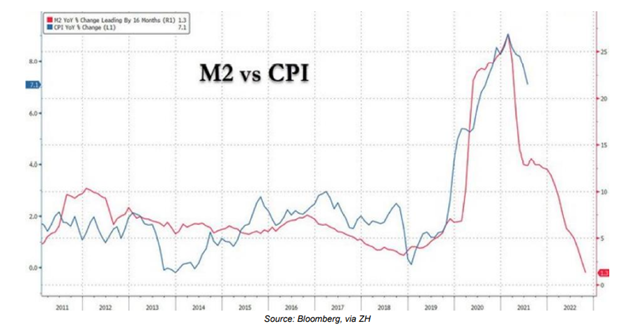

* US tax receipts (crippled by tanking capital gains from a tanking market thanks to spiking rates) have fallen 11% y/y and getting worse;

* Uncle Sam’s bar tab (USTs, or “IOUs”) is heading toward annual levels of $4-$5 trillion (with a T), which means the global supply of US Treasuries is poised to overtake global GDP growth as bonds tank and yields rise, thus killing everything in their wake except for a temporarily and Frankenstein-strong USD;

* Last month, Federal deficits expanded to record-high levels of $249 billion;

* No one wants Uncle Sam’s debt. The recent auction for 10-Year USTs was a disaster, adding more downward pressure on bonds and hence upward pressure on US yields (above 3.6%) and rates—all of which makes repaying combined US public, private and corporate debts ($90T) one step closer to its breaking point;

* By “tightening” the money supply (QT) to “fight inflation,” Powell has decapitated M2 supply growth (i.e., needed liquidity, lower line below) from 25% to basically 0%– and all he has to show for his linear “war” against inflation is a mis-reported decline in an otherwise misreported and bogus CPI rate from 8% to 7.1%. That’s what historians call a “pyric victory”: