Gold’s Rise Is Just a Recession Away

Many are asking about Gold’s rise, or better yet: When, how and why it will rise?

Toward this end, cold data in the face of historical facts and current recessionary realities will make gold’s rise easier to grasp.

Let’s start with the cold data, which centers around officially reported real rates and relative USD dollar strength, two current and key headwinds to gold’s rise.

Cold Data Point 1: Real Rates

As we’ve written previously, there is a clear inverse relationship (95% correlation) to real (inflation-adjusted) rates and the gold price.

Stated simply, when inflation outpaces the yield on the 10 UST, the net result is a negative real rate environment. Conversely, when rates (as defined by the yield on the 10Y UST) are above inflation, we have positive real rates.

Gold, as a real asset that produces no yields or dividends, shines brightest when real yields/rates are negative.

After all, when bonds produce negative returns, investors look more favorably toward real assets like precious metals.

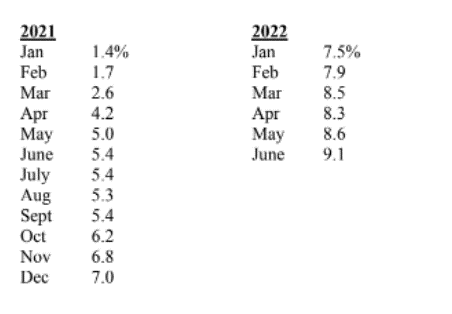

Today, one would think that soaring Year-over-Year (YoY) inflation in the U.S. at 9.1% (and closer to 18% using the more honest 1980’s CPI scale) against a 2.89% nominal yield on the 10Y UST would seem to be a screaming indicator of negative real rates and thus a profound tailwind for gold, right?

And as to inflation, we said over a year it ago it would skyrocket while Powell promised it was “transitory.”

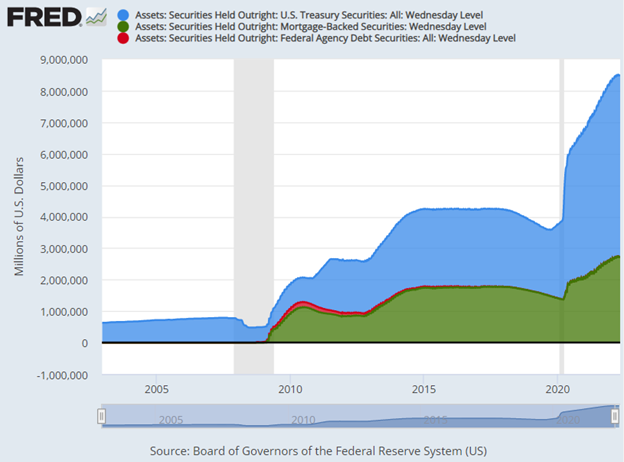

After all, when a nation expands its money supply by 40% in a two-year period prior to COVID and Putin, one can’t just blame inflation (or a later Fed Balance Sheet expansion from $4.2T to $8.7T) on a virus or Russian bully.

Based on these cold facts and the subsequent (and monthly YoY) CPI figures, who was more candid (and accurate) about transitory inflation? See a trend?

Getting back to real rates, a 2.9% nominal yield minus the above 9.1% inflation rate = negative 6.21% real yields.

Easy-peasy and good for gold’s rise, right?

Well, nothing is that simple in our new central bank normal…

Fudged Math

Whether you believe in central banks or “official” inflation data (and we certainly do not), this doesn’t change the equally cold fact that central banks (or central controllers) are nevertheless always right, even when they are empirically wrong.

According to the Fed, for example, the Real Rate on the US 10Y UST is +1.06%.

See for yourself.

Huh?

How does a negative 6% become a positive 1%?

Short answer: Clever Fed math (mixed with deflationary expectations priced into the duration of the bond).

Huh?

As indicated in many prior reports, the Fed, much like Al Capone’s accountants, are masters at manipulating, downplaying, obfuscating or just flat-out non-reporting embarrassing facts, including severe inflation realities, to create fictional calm.

Thus, when publicly charting otherwise embarrassing real rate data, they employ a spiders-web of clever math and proprietary models to come up with a downplayed inflation rate against which they measure nominal rates to derive a fictional “inflation-adjusted” real rate.

In other words, they fudge the numbers.

In the example above, rather than using the otherwise simple 9.1% YoY inflation rate, the Federal Reserve Bank of Cleveland offers us an official mash of “expectations”, “risk premiums,” “real risk premiums,” the “real interest rate,” as well as a “model” that mixes “data, inflation swaps” and even “surveys” just to avoid stating what is already abundantly clear: Real rates today are -6.21 not +1.06.

In essence, the foregoing Fed math hides the blunt reality of current inflation by saying they foresee deflation ahead over the duration of the 10Y UST.

And as we discuss below, they may ironically be correct but for all the wrong reasons…

For now, and given the “official facts” as presented by the never-wrong Fed, current real rates on the 10Y UST are often mis-presented as slightly positive rather than honestly reported as deeply negative.

And as stated above, this fiction has been a clear, deliberate (and temporary) headwind for gold’s rise.

Cold Data Point No 2: Rising (but Short-Lived) U.S. Dollar Strength

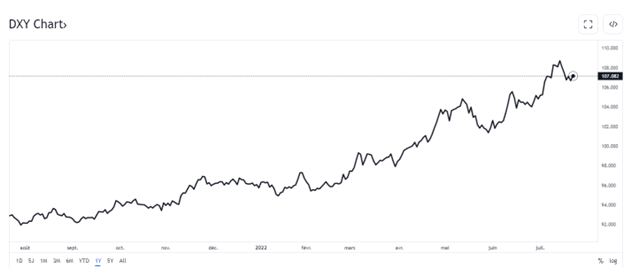

The USD, of course, has been rising at astronomical levels (7% in Q2), and this too is often a headwind to gold’s rise, as a rising dollar appears/appeals to many investors (foreign and domestic) as a safer haven than precious metals.

In fact, a rising USD and rising rate environment was immediately (and predictably) bad for just about every asset class, though far less so for gold’s rise. There were few places to hide.

Percentage declines across asset classes for 1H 2022 proved this point:

NASDAQ 100 Down 29.3%

S&P 500 Down 20.0%

Emerging Markets Down 17.2%

US Govt Bonds (TLT) Down 21.9%

Real Estate (XLRE) Down 20.1%

HY Bonds (HYG) Down 13.8%

Muni Bonds (MUB) Down 7.8%

Gold Bullion Down 1.2%

We’ve explained this dollar rise in prior reports as a desperate yet explicable attempt by Yellen and Powell (and Biden and Summers) to attract foreign inflows into U.S. markets wherein the USD is seen as a relatively superior “safe haven” when compared against other global currencies, like the Euro, whose debt levels (and non-reserve currency status) can’t endure equally hawkish rate hikes.

That is, by pursuing deliberate and well-telegraphed rate hikes (50 bps in May, 75 bps in June and potentially more to come in July), the Fed, for now, has made the USD the best currency horse in the international fiat glue factory.

This deliberate policy to make the USD stronger is a temporary tool to “fight” inflation, as it reduces the cost of import prices within the U.S.

A German toaster, after all, costs less when the USD reaches parity with the Euro.

But a stronger USD also strangles U.S. export competitivity and adds to increased U.S. trade deficits longer term, which is one (but not the main) reason the strong USD policy will be short-lived (see below).

Why short-lived?

Because as indicated above, historical facts and current realities all converge toward a recessionary landscape in which weaker currencies and lower rates are the only path forward.

What makes us think so?

The Historical Facts and Cold Math of Recessions

Despite the post-2008 Fed’s valiant yet vain (really vain) attempts to convince the world that recessions have been made extinct by mouse-click monetary policies, the simple yet common-sense reality is that recessions have not been outlawed (but merely postponed) by such fantasy fiat dollars.

Deep down, we all know this, even the market bulls: You can’t solve a debt crisis with more debt paid for with money created by a computer rather than GDP.

The other simple yet common-sense and historical reality is that no recession (not one, not ever) can be defeated in a backdrop of high rates and a strong currency, the very policies which the US is currently and temporarily pursuing.

Despite the fatal hubris and immense power of the Fed, the U.S. will be no exception to these recessionary realities and consequent policy shifts.

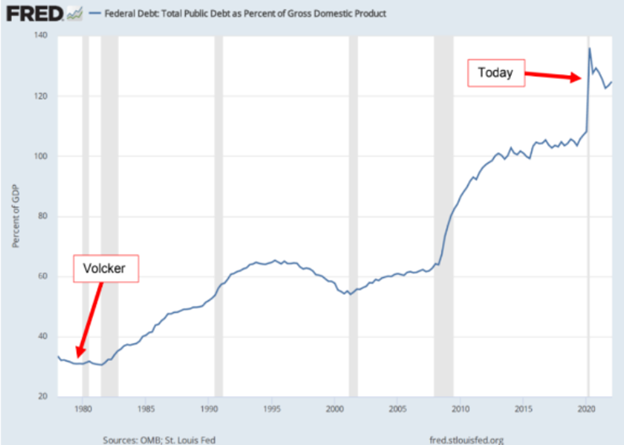

The markets (from the NASDAQ to Muni-bonds) can’t afford rising rates and will continue to fall as Powell pretends to be a rate-hiking Volcker despite forgetting that Volcker was facing a 30% debt to GDP in 1980, not 125% ratios in 2022.

Powell may want to believe he’s a Volcker, and I’d like to ride a horse like Adolfo Cambiaso or throw a fast ball like Nolan Ryan, but it ain’t gonna happen.

In short: Powell will pivot as the grotesquely over-heated bubble markets the Fed created start tanking further.

Tech stocks (of which we consider BTC to be) are uniquely poised for further pain…

Like the Q1-Q4 2018 rate-hikes to the predictable 2018 Q4 market beat-down (and hence 2019 pivot), the Fed will reduce rates and the USD will weaken in a QT to QE pivot once the recession off (or already under) our bow slams into our debt-soaked and sinking Titanic economy and markets.

Current Realities: Recession Ahead (or Already Here?)

Recessions become official (and lagging) once the number-crunchers (i.e., fiction writers) in DC officially tell us so, namely, once they report 2 consecutive quarters of negative GDP (i.e., too late for most retail investors who still trust the Fed).

Thankfully, there’s no need to hold our breath. Despite already feeling like we are in a recession, the Atlanta Fed GDPNow data has confirmed a negative Q1 GDP (-1.5) and foreshadowed a 0 to negative Q2 GDP.

In short, we are likely already in recession, and this neither bothers nor surprises the Fed. After all, the same bankers who built the inflationary bubble will trigger the deflationary recession to follow.

Stated more simply, and when it comes to market bubbles, the Fed giveth and the Fed taketh away.

The Fed’s Real Anti-Inflation Weapon: A Deflationary Recession

Despite pretending to fight inflation with rising rates, the Fed knows its nervous rate hikes (be they at 50, 75 or even a 100 bps) won’t defeat current inflation, which is considerably much higher than officially reported. Negative rather than positive real rates are already (albeit unofficially) in play to deliberately “inflate away” some of Uncle Sam’s embarrassing debt.

By lying about (i.e., “fudging”) the inflation data, the Fed therefore gets to have its cake and eat it too; namely it can privately exploit extreme inflation while publicly pretending/reporting it lower than it actually is, even at these embarrassing levels.

(Of course, another way to calm inflation fears is to intentionally repress the paper price of gold on the COMEX, of which we’ve written extensively.)

Yet looking ahead, the historically most accurate tool for fighting inflation (and crushing Main Street), of course, is a recession, wherein economic growth and consumer demand weakens and hence prices (and inflation) fall—i.e., deflationary forces.

The Fed knows this too. Nothing fights a Fed-created inflation like a Fed-induced recession. Thanks Mr. Powell.

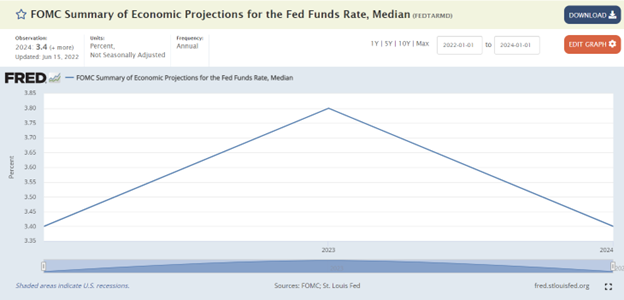

The current chest-puffing claims by the Fed to send the Fed Funds Rate to a “projected” 3.8% by 2023 is, in my opinion, just another Fed ruse, as nearly all its “projections” have been in the past.

At $30T+ in public debt, Uncle Sam (or Mr. Market) can’t afford such “projections.”

For every 1% rise in rates, the cost of servicing Uncle Sam’s $30T+ bar tab rises by $27 million per day.

And WHEN not IF the recession hits the U.S., the Fed knows all too well that there is no way out of that dis-inflationary (and long-term) recession other than lower rates and a weaker USD—all good for gold’s rise.

As our advisory colleague, Ronni Stöferle recently observed: “The current cycle of interest rate hikes could go down in history as the shortest and weakest in recent decades.”

Why?

Because, 1) economic activity and growth is slowing (and has been for years), 2) indebted nations can’t afford meaningfully higher rate hikes, 3) inflationary debt relief is counter-acted by increased government spending, and 4) markets are already pricing-in inevitable rate cuts.

The Return of the Money Printers—Just a Recession Away

And what’s the best method to 1) cap or cut rates (as Japan’s current YCC confirms), 2) weaken the currency and 3) spur “growth” in a recession?

Easy: A money printer to artificially suppress bond yields and weaken (debase) the currency.

Again, this means the inevitable pivot from current hawkish tightening to future dovish easing is just a recession away.

For now, and as stated elsewhere, the Fed’s (and Canada’s) hawkish rate hikes today have been engineered not to fight inflation, but simply to have room to cut rates tomorrow when the recession our central banks have been postponing with mouse-click dollars comes painfully home to roost.

Gold Price Reaction, Gold’s Rise

This inevitable shift from a rising dollar and rising rate setting to a falling dollar and repressed (but still negative) rate reality in a recession will be an extreme catalyst for gold’s rise, now currently and intentionally suppressed by: 1) an openly rigged COMX market, 2) a disingenuous “anti-inflationary” rate hike policy and 3) a short-term strong dollar policy to fight mis-reported (i.e., much higher) inflation.

My colleague, Egon von Greyerz, would remind that gold’s rise is based on more than just inflation and deflation fluctuations or rising or falling rates.

Indeed, gold’s rise in the past has occurred in environments of a strong dollar, a weak dollar, a rising rate and a falling rate.

There are many specific reasons and contexts for this, too numerable and nuanced to unpack in an article, which is why we’ve authored a book (Gold Matters) to explain the same in greater detail.

There’s More to Gold’s Rise than a USD

Furthermore, and as anyone owning gold in currencies other than the USD already knows, gold’s rise has been considerably stronger against currencies who don’t have the bullying power of the USD—namely the power to export inflation or pivot from Hawk to Dove to Hawk because of a world reserve currency status.

The EU and its central bank, for example, are so thoroughly debt-strapped and dependent upon USD-based markets, debts and settlement policies that even an ECB rate hike move from 25 bps to 50 bps has LaGarde shaking in her designer boots.

France, from where I sit, has a total debt to GDP ratio of over 350% and Italy, whose debt and political coalition confusions are no mystery to European citizens, is an early warning sign of future economic and political fracturing in the EU.

Germany, meanwhile, will soon (2023) have to pay the bill for the inflation-adjusted bonds it issued in prior years, the cost of which will be 25% of the nation’s total debt.

And as for Japan and its dying Yen (at 50-year lows and down 24% in dollar terms in the first half of 2022 after decades of mouse-click money madness/QE), this nation is effectively a financial zombie.

Again, these are just cold facts.

Not Even the USD Can Avoid Nature

Despite the slow, very slow process of de-dollarization set in motion by openly failed/backfiring sanctions against an energy-rich Putin, the USD remains uniquely positioned (via its petrodollar, its SWIFT pre-eminence and its post-war reserve currency status) to sin deeper and longer with its centralized money printers, fictional CPI authors and disingenuous rate policies.

But not even the USD and an artificially engineered and controlled market economy can escape the inevitable and natural consequences of over-expansion, over-dilution/debasement and over-indebtedness.

Regardless of how the Fed and other central banks misreport inflation, recessionary realities will make the genuine nature and future of negative real rates a reported reality, which will create an optimal setting for gold’s rise.

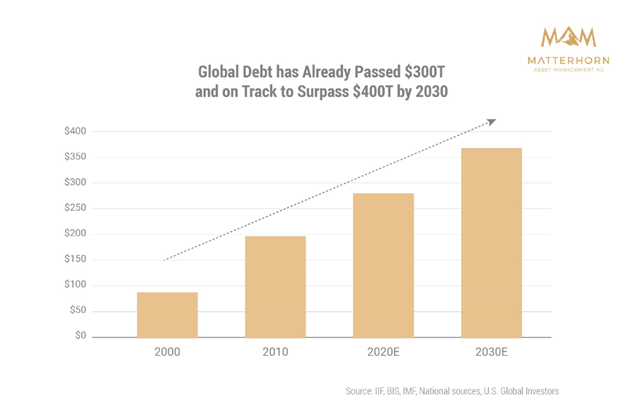

As I, Ronni Stöferle and many others have argued for well over a year, the developed economies (which are in fact little more than debt-soaked banana republics on paper) cannot endure (ertragen) the reality of an international debt crisis which would surely follow any prolonged policy of rate hikes into a global debt swamp of over $300T.

Gold owners will benefit most from these inevitable changes and realities, as all currencies and all central banks are running out of tools, options and excuses.

As in hockey, polo or asset prices, the best players look to where the puck or ball is headed, not where it currently sits.

The forces discussed above (recessionary, rate and currency) collectively, historically, empirically and common-sensically point toward new highs for gold, whose bull market, which began to stretch its legs after the 2016 bottom of $1050, has yet to sprint ahead.

But gold will sprint fast and higher north, even if it does not feel like it today.

Gold’s Rise Is Just a Recession Away

As repeated in numerous articles and interviews, global central banks in general, and the Fed’s Jerome Powell in particular, have placed themselves and the global markets and economy in a trap from which there is no escape short of biting off their own feet, as they’ve had a foot in their mouths for years.

Or as Mohamed El-Erian said best: “The Fed has no good scenarios left.”

This blunt point simply can’t be repeated enough.

Candor (and Debt) Matters

With global debt at $300T+, and combined U.S. corporate, household and public debt well past $90T, the Fed’s “face-saving” attempt to raise rates (even to the unsustainable level of say 4%-5%) as a weapon against 9% reported (i.e., under-rated) CPI inflation is a failed strategy from the start.

In fact, it is delusional at best, and more likely dishonest at worst. Full stop.

Simply stated, an historically debt-soaked market, economy and government addicted to years of artificially repressed free money can’t suddenly afford a meaningful rate hike (i.e., expensive money) without a fatal string of credit defaults, from investment grade to sovereign bonds.

Facts Portend the Future

Toward this end, we’ve dedicated years to fact checking, BS-detecting and calmly disclosing a long string of open rigging, lies and errors masquerading as policy which have poured from the lips and policies of figures like Greenspan, Bernanke, Yellen and Powell.

Despite the stubborn honesty of such facts and dishonesty of our bankers, many FOMO investors have clung to the cognitive dissonance of believing central banks had their backs—and their markets and currencies in eternally safe hands.

Now, as the transitory inflation lie has broken the credibility of these lost shepherds and the faith of their sheep, the financial word is facing the first chapters of a global “uh-oh moment” (i.e., geopolitical risk, falling markets, debased currencies, failing leadership, and increasing social unrest), the inevitability of which we’ve warned in two published books and countless reports.

Most reading this, of course, are not among the sheep nor the surprised. Yet even for you and us, the continued hubris, ignorance and dishonest desperation of our so-financial “leadership” never fails to astonish.

Let’s see why.

Apparently, Powell is afraid of going down in history as the next Arthur Burns.

Not surprisingly, he appears more pathologically concerned about his personal legacy than the fatal legacy he and his predecessors have left the inflation sick nation after inflating the Fed balance sheet from $800B pre-08 to over $9T today.

Despite the obvious and direct inflationary consequences of such balance-sheet expansion, everyone in a DC office (from Biden to Powell) wants to save their reputational behinds and blame the consequences of decades of their openly inflationary monetary policies on a virus and a bad guy in Russia.

How’s that for profiles in courage?

And even now, Powell still thinks he can emerge as the next Paul Volcker by raising rates to fight the inflation he helped create.

Man, the ironies do abound.

Folks, Powell is no Volcker.

A Lesson for Mr. Powell: Debt Matters

Mr. Powell, if you are reading this, let us remind you that when Paul Volcker was raising rates, the US public debt was below $900B, not the current $30 TRILLION debt level which the Greenspan generation (i.e., that includes YOU) directly created.

Let us also remind you that the “Volcker era” U.S. debt-to-GDP ratio between 1979 and 1981 was 31% and our deficit-to-GDP level was only 2%.

TODAY, our debt-to-GDP ratio is over 125% and our deficit ratio is approaching 7%.

Math, facts and debt are stubborn things, no?

This, Mr. Powell, explains why Volcker was able to raise the Fed Funds Rate (FFR) by over 1000 basis points to fight inflation, and this is further why even a pathetic 300 basis point rate hike under your watch by 2024 will be as ineffective to fight inflation as a submarine with screen doors.

By the way Mr. Powell, even a meek 3% FFR as you so “hawkishly” propose would leave our FFR rate lower than it has been for 98% of the last 67 years.

In short, if you are honestly pretending to fight inflation with a wimpy little rate hike like this (because 300 bps is about all that the gasoline-debt-soaked USA can afford thanks to you, Yellen, Bernanke and Greenspan making us debt broke), you are effectively bringing a knife to a gun fight (i.e., you’re gonna lose).

Furthermore, your proposed rate hikes (far too little, far too late) will raise the cost of Uncle Sam’s embarrassing bar tablevel from 7% to over 11% of our ever-dwindling GDP.

In short, Mr. Powell, you’re dreams of Volcker glory, or even Volcker efficacy, are only that: Dreams.

Dreams to Nightmare

For the rest of us, however, the nightmare you’ve unleashed and the “solution” you’re proposing is rigged (doomed) to fail.

Your FFR rate hike will create debt pains that will last for years, as the government’s average debt maturity is greater than 4 years.

Even these meager yet higher rates will (and already have) disrupted financial markets, strangled GDP growth, augmented welfare spending and shrunk U.S. tax receipts by 16% YoY in May and likely by 30% in June.

Ouch.

Mr. Powell, while crunching numbers in school, did you ever bother to read Hume or von Mises?

They would have shown you (with numbers not hard words) that GDP growth is mathematically impossibleonce debt levels are greater than 100%.

Or just ask Kuroda, as you can no longer ask Abe.

Although you will never be the next Volcker, you may want to purchase a biography of Benjamin Strong, the first Fed Chair to trigger a depression by not allowing inflation to run hot as mandated by the rules then in place (i.e., when the USD was tied to gold) …

Powell’s Real Plan? Let Inflation Rip

But then again, Strong’s mistake of not allowing inflation to run hot enough to “inflate away” U.S. debt may not be your mistake, but deep down your real plan?

In short, I’m guessing that more rather than less inflation is your only real option and plan, despite headlines (and rate hikes) to the contrary.

I’m guessing you’re only raising rates now so that you’ll have something, anything at all, to cut when markets truly tank, and we both know they will tank much further, unless…unless…

…unless you are waiting for markets to break so that you can grab a coffee and doughnut, walk into that dark room at the Eccles Building with all those glowing screens and start adding magical 0’s to your balance sheet (i.e., mouse-clicking more fake money), which we both know is INFLATIONARY.

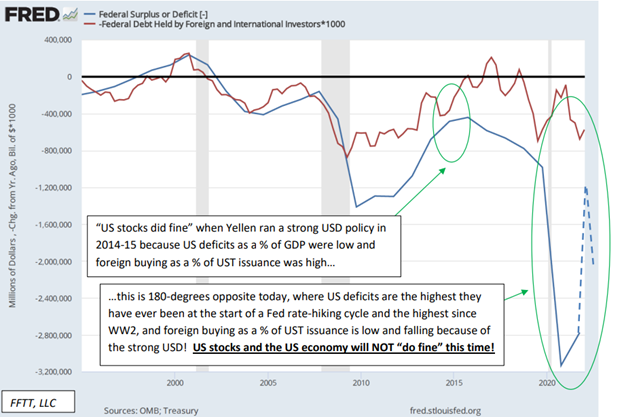

Sure, your ol’ Pal Yellen (who slithered from the private Federal Reserve to the Treasury Secretary’s desk a few blocks away) has tried to push the USD (and DXY to 110+) to fight Putin’s inflation (?), but that too was just another knife in a gun fight…

Yellen believed she’d pull a Reagan-era 2.0 with a stronger USD and hence attract foreign money to make a stronger market.

But as revealed above, our debt levels (thanks to folks like you and Janet) aren’t the same as the 1980’s or even 2014, and her strong USD “plan” was a disaster rather than swan song for the markets, as we previously warned and as the following graph from Tree Rings makes all too clear:

This “strong USD” plan has crippled just about every asset class but the USD, and only managed to lure a few foreign suckers into a tanking US market.

So, Mr. Powell, you’re in a debt corner of your own (and Janet’s, Ben’s and Alan’s) making, and I’ll say what you won’t, namely: You want more not less inflation to get Uncle Sam out of debt in the same way every broke regime from Rome to Paris to Tokyo to Ankara to DC has done and will do again–by inflating away their debt, crushing the (angry) man on the street and blaming the inflation (i.e., currency debasement) on anyone but themselves?

Mr. Powell, why not just say it out loud? Truth may be a rare political tool, but it is an equally stubborn thing.

Waiting for Gold

Meanwhile, and it the midst of so much political, cultural, financial, military and social chaos in 2022, gold’s performance has been less than favorable.

Retail investors are getting out of gold ETF’s ($1.7B last month) at the wrong time, which sadly, is what retail investors often do.

Ironically, and not surprisingly, the biggest buyers of gold of late are the central banks themselves, who having colluded to paper squeeze the gold price down before buying, are reaping the rewards of their manipulation games.

Foreign central banks are seeking gold as an alternative to a USD whose days of hegemony are coming to end.

As argued, US attempts to lure foreign money into tanking US markets via a stronger dollar and rising rates are both unsustainable and backfiring, but these forces have certainly put a temporary dent in the gold price trading in the 1700 range.

Of course, when measured against other currencies outside the USD, gold has done far, far better.

It’s fair, of course, to also remind that gold has suffered far less than bonds (S&P bond index down 9%), cryptos (down 75%) and stocks (S&P down 20%), but patient gold investors already know that.

Higher rates are a gold headwind, but not forever. Gold soared between 1971 and 74, and again between 1977 and 1980, as rates in the US were rising not falling.

Remember: Gold is a monetary metal, a store of value. It’s not a tech or growth stock. It’s loyal, and as such, it consistently surpasses its prior peaks, especially in the backdrop of rising inflation.

Stated simply, its bull market has yet to begin.

Gold’s Rise Is Just a Recession Away

The current and open fraud regarding the paper gold price in the COMEX market is now as plain to see as the open desperation in the global financial system, which is unraveling in real-time all around us.

As risk assets tumble foreseeably into bear territory before a headwind of deliberately rising rates, precious metals have seen headline-making falls as well.

Below, we explain why.

Tracking the Paper Gold Price —The Standard Answer

In prior reports, we’ve noted that precious metals typically behave sympathetically when markets tank; thereafter, gold then surges north. We saw this pattern in October of 2008 and March of 2020.

Furthermore, when a Hawkish Fed pursues a temporary yet face-saving policy of rate hiking and quantitative tightening, this makes the USD the relatively stronger horse in the global currency glue factory.

And a relative rise in the USD, of course, is a headwind to gold.

Explaining the Paper Gold Price —The Rigged Answer

But let’s get to the real heart of the matter, namely: Legalized paper gold price manipulation (i.e., fraud) in the COMEX market, a topic we’ve addressed more than once, here and here.

As we’ve openly argued for years, nothing embarrasses an otherwise discredited fiat currency like a rising gold price.

As I’ve described it, rising gold prices are a middle finger to debased currencies whose declining purchasing power are the DIRECT result of the failed and drunken monetary policies (i.e., mouse-click trillions) of a central bank near you.

Or as Ronan Manly more distinctly observed: “Gold to central bankers is like sun to vampires.”

And that, folks, is precisely why the big banks (under the direction of the BIS) are deliberately (and if law school serves me correctly) as well as fraudulently manipulating the paper gold price.

Facts vs. Manipulation

In the first quarter of 2022, we saw record high purchases of ETF gold, physical gold and central bank gold. Even Goldman Sachs’ head of commodity research was targeting $2400 gold this year.

Instead, the gold price has been falling as gold demand has been rising.

Huh?

It reminds me of 2008 when mortgages were defaulting en masse yet the ABX index for sub-prime mortgages was rising.

In short, complete (and temporary) manipulations were going on behind the curtains of a few wayward banks, including Morgan Stanley.

Today’s gold behavior (i.e., surreal manipulation) is no different and no less of an insult to the natural forces of supply and demand, which central bankers have attempted to destroy for well over a decade.

But the jig will soon be up on these masters of open fraud and Wall Street socialism.

The Paper Gold Price & The Horse’s Mouth

For now, and in case you fear I’m just acting as a “gold bug” apologist, let’s go straight to the horse’s mouth and examine the confessions and facts of open price manipulation in the precious metal markets.

And I swear, you really can’t make this stuff up, it’s just that obvious and distorted.

In a recent article by Peter Hambro published by the British news site, Reaction, a 3rd generation gold insider (Petropavlovsk, Bank Hambros) made the open secret of paper gold price manipulation abundantly clear and incontrovertible.

It’s also worth adding that Mr. Hambro’s entire career was that of an heir to a banking dynasty all too familiar with the insider machinations of the London bullion markets and London Stock Exchange.

In short, when Mr. Hambro discusses gold price manipulation, it’s worth listening.

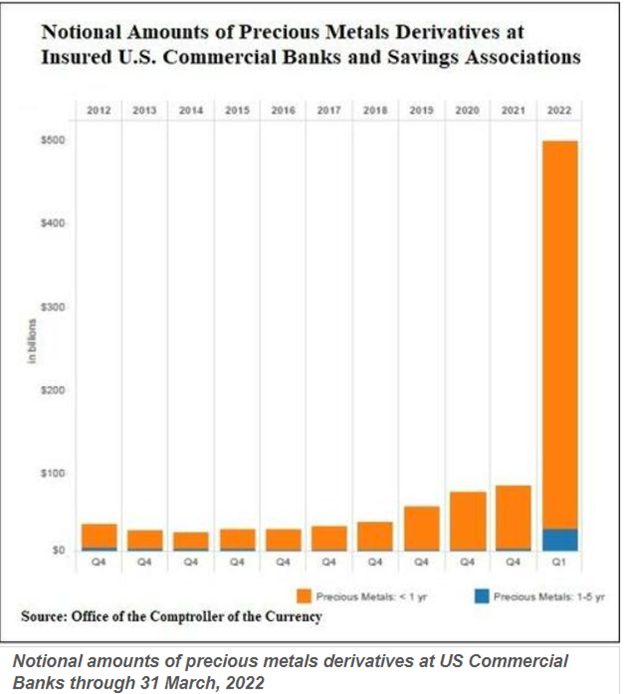

A Chart Says a Trillion+ Words

More importantly, and for those who prefer facts over human confessions or “gold bug whining,” the following chart from the U.S. Office of the Comptroller of the Currency (OCC) clearly reveals the extreme extent by which just a handful of highly pocketed (and central bank supported) banks like JP Morgan and Citi can use extreme turns of derivative-based leverage to short (i.e., keep a permanent boot to the neck of) the paper gold price:

That rising bar on the far right is nothing more than crime scene evidence.

As Hambro remarks, a long history of media and bank supported mis-information has tried to keep a lid on the desperate attempts by just a small number of BIS minion banks like JP Morgan and Citi to effectively prevent free market price discovery on the paper gold price.

Despite thousands of daily long contracts (i.e., buy orders) in the OTC forward contract markets, if just 7-8 banks wish to use massive leverage (rising bar on the right) to short the same metal, they can effectively fix the gold price via artificial manipulation of derivatives contracts, to which only a small number of banks have access.

All of this open yet legalized fraud is managed by the central-banks central bank, namely the Swiss-based Bank for International Settlements.

As Hambro states, and as taken from a recent article published by Ronan Manly:

”[s]ince 2018 the Financial Stability Desks at theworld’s central banks have followed theBank for International Settlements’ (BIS) instruction to hide the perception ofinflationby rigging the gold market.”

Hambro further observes:

“With the help of the futures markets and the connivance of the Alchemists, the bullion traders – yes, that includes me, I was Deputy Managing Director of Mocatta & Goldsmid – managed to create an unshakeable perception that ounces of gold credited to an account with a bank or bullion dealer were the same as the real thing. ‘And much easier, old chap! You don’t have to store or insure it’”.

So, there you have it: Banks acting badly, very badly.

No shocker there…

The Greenlight from Big Brother

In essence, a handful of 7-8 LBMA institutions creates an almost limitless amount of synthetic paper representing unallocated gold (i.e., gold they don’t actually own) to short the paper gold market.

Why?

Again, because the central bankers mouse-clicking and hence destroying trillions worth of sovereign currencies (since Nixon took the gold chaperone away in 1971) are utterly terrified of a neutral and relatively fixed/scarce monetary metal like gold—i.e., real money.

Indeed, gold is money, the rest is just debt and toilet paper masquerading as currency.

Furthermore, the policy makers (or central controllers) are embarrassed to confess the inflationary consequences of their absurd money printing, and nothing reveals those consequences more than a naturally rising gold price.

Solution?

Easy: Lie about inflation and rig the paper gold price with leverage, derivatives and a greenlight from the BIS, aka: “Big Brother.”

In Rigged to Fail, I revealed how central bankers rig the bond and hence stock markets. Here we are just showing you how the same bankers rig the gold price to hide a failed currency market.

And if you want to put a handsome face to the farce, here’s an unforgettable one:

What About Don’t Fight the Fed?

Of course, most of you may be angry yet not the least bit surprised to see such rigging hiding in plain sight.

And even if your eyes have been (or now are) wide open, you’re also likely to say, “great, thanks for the news, but how the heck can we (or gold) fight all the central banks?”

Fair question.

As I’ve said, even if you know about a dirty cop, there’s almost no point in fighting one, right?

The Jig (Rig) is Up

We may be a bit jaded and realistic, but that doesn’t make us naive. Gold will get the last and honest laugh over such a corrupt and dishonest “policy.”

As central banks continue to lose more and more credibility, and as investors become more and more fluent in, and aware of, the absurdity of the lies that have been sold to us for years by central bankers and MMT midgets who claim that a debt crisis can be solved with more debt, which is then paid for with trillions created out thin air, the system unwinds.

As the inevitable inflation crisis emerges from precisely such absurd “policies,” the central bankers can no longer blame the obvious and long-dated/repressed inflationary consequences of their drunken monetary policies on a virus or Putin.

Nor can they continue to peddle the lie that inflation was merely “transitory,”a fact we made clear long before Powell confessed it was not so.

Stated otherwise, more and more folks are catching on to the fraud.

The math plainly shows that expanding the broad money supply (and central bank balance sheets from $6T to $36T in just over a decade) is the real cause of the inflation in your neighborhood and the debasement in your wallet.

The First Cracks & the Last Straws

Geopolitical shifts, assassinated prime ministers, fired prime ministers, angry truck drivers, stormed capitals and Sri Lankan protestors are just the first tragic cracks in a growing social unrest driven by declining wealth and growing wealth disparity, all classic and historic symptoms and patterns of when a debt crisis leads to a political crisis, and sadly (and ultimately) more centralized controls over our markets and lives.

But as even Hambro observes, eventually the last straw breaks the back of a rigged camel, and the “straws blowing in the wind are often said to presage great tempests and I believe that {the chart above] shows just such a straw.”

Years of distorted, rigged and entirely reckless debt-and-print polices have made global economies and currencies weaker, not stronger.

The weaponized USD in the wake of the failed Putin sanctions is just further proof of how weak Western economies have become.

Dying Faith, Rising Gold

After years of profligate central bank policies, the so-called “developed economies,” which are now little more than glorified banana republics, are losing credibility, options and most importantly public faith.

This is critical.

In the end, when faith in a system ends, so does its currency.

We’ve written before how impossible it is to market time “the end of faith,” but charts like the one featured herein help to point out the rigging and hence accelerate the inevitable end to derivatives-based fraud, centralized price-fixing and, eventually, the OTC casino in particular.

Meanwhile, the current buy window for repressed precious metals is remarkable, and once central banks cripple the markets to their deflationary pain points, chaos will return, along with the inflationary money printers—all of which will send precious metals higher and fiat currencies and markets to their mean-reverting lows.

Gold’s Rise Is Just a Recession Away

What the U.S. in particular, and the West in general, are failing to confess is that today’s so-called “Developed Economies” are in actual fact more like yesterday’s debt-straddled Emerging Market economies, and like a real banana republic, the only option ahead for our clueless elites is inflationary (and intentionally so).

Titanic Ignorance

I’ve often cryptically joked that listening to investors, mainstream financial pundits or downstream politicians debating about near-term asset class direction, inflation “management” or central bank miracle solutions is like listening to First Class passengers on the Titanic debating about desert choices on the menu in their hands rather than the debt iceberg off their bow.

In short: The real issues are right in front of us, yet ignored until the economic ship is already dipping beneath the waves.

Rising Debt + Declining Income = Uh-Oh.

As for such hard facts (i.e., icebergs), the most obvious are fatal global and national debt levels rising at levels which can never be repaid….

Meanwhile, national income from GDP and tax receipts are falling, which means debts are grossly outpacing revenues, which any kitchen-table, boardroom or even cabinet meeting conversation should know is a bad thing…

Toward this end, it’s worth lifting our eyes above the A-deck menu and taking a hard look at the following iceberg scrapping the bow, namely: Tanking US tax receipts:

What Biden and Powell might wish to remind themselves is that U.S. tax receipts have fallen YoY by 16%, and are likely to fall even further as markets continue their trend South at the same time the US steers toward a recessionary block of ice.

No Love for Uncle Sam’s IOUs

What’s even more alarming is this stubborn fact: as U.S. Federal deficits are rising, foreign interest in Uncle Sam’s IOU’s (i.e., U.S. Treasuries) are tanking.

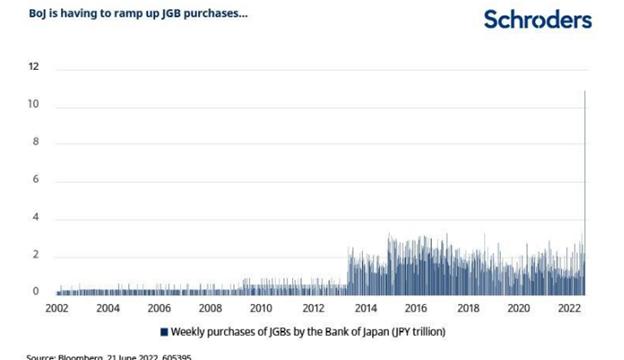

China’s interest in U.S. Treasuries, for example, has hit a 12-year low and Japan, as I’ve warned elsewhere, is too broke (and too busy buying its own JGB’s with mouse-klick Yen) to afford bailing out Uncle Sam.

The level of magical Yen creation (reminiscent of the Weimar era) coming out of Japan to “support” its pathetic bond market is simply mind-blowing:

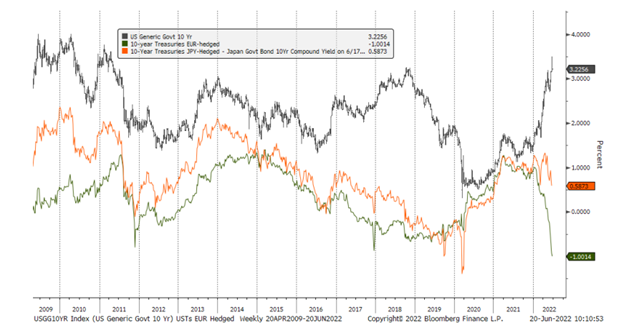

Given the artificial and relative current strength of the USD and the fact that FX-hedged UST yields are negative in EUR, it’s fairly safe to conclude that there will be more sellers than buyers of UST’s. That means rising yields and rates near-term.

Ouch.

That’s a bad sign for Uncle Sam’s bloated and unloved bar tab. Who but the Fed (and hence more QE) will buy his IOUs by end of August?

Filling the Deficit Gap: Print or Default?

In the past, the spread between rising debts and declining faith in U.S. IOUs was filled by a magical money printer at the not-so-federal “Federal” Reserve.

But with a cornered Fed still tilting toward QT rather than QE, where will this magical money come from, as it sure as heck aint coming from tax receipts, the Japanese, China or Europe?

As I see it, the Fed has only two pathetic options left if it wants to fill the widening gap between its growing deficits and declining faith from foreign bond buyers (or even US banks, see below).

Namely: It can 1) default on its embarrassing IOU’s and send markets over a cliff, or 2) pivot from QT to QE and create more magical (i.e., inflationary and toxic) money.

When it comes between embarrassment or toxicity, my bet is on option #2, which means expect more rather than less QE and inflationary currency debasement ahead.

Why?

Saving the Politico’s, Drowning the Citizen

Because neutering one’s currency is the classic/desperate policy taken by all debt-soaked regimes to create a negative-real rate lifeboat for themselves while leaving the average Joe Citizen shivering in an inflationary ocean of pain.

As I’ve said countless times, the Fed WANTS INFLATION to inflate away its debt nightmare and only pretends to fight it.

Rising rates are simply no option as higher rates are simply too expensive for Uncle Sam.

YoY interest payments alone on Uncle Sam’s bar tab were already at $666B by end of May. If one tacks on the extra interest owed on Treasury Bills and maturing notes, that interest expense climbs to just under $900B.

Again, that’s just the interest expense. Do you really think Uncle Sam wants to (or can afford) to charge himself more (i.e., by raising rates) for his own (and otherwise unpayable) debt?

I Could Be Wrong?

But one must hedge even one’s own highest convictions, and I suppose the Fed could try to increase demand for UST’s (as a so-called “Safe-Haven”?) by lifting rates and crashing the stock market rather than re-heating its money printer.

Anything is possible in a world bereft of good options and riddled with bad financial leaders.

But such an equally pathetic option (i.e., an induced market implosion) just means less capital gains tax receipts from the stock-rich and hence places the Fed right back where it started: Starring down the barrel of even less incoming cash, even less consumer spending and hence even less GDP.

In short: I just don’t see anyway around the pathetic QE and pro-inflation end-game ahead, which the Fed pretends to ignore and the feckless corporate media can’t even fathom.

Seeking Rather than Fighting Inflation

And so, I’ll say it again and again: The Fed is not fighting inflation, it wants inflation.

Or in plainer English, and as no surprise to Fed-watchers like me: The Fed is, once again, simply lying to the public.

The West: Just Another Banana Republic

Today, whether we wish to admit it or not, the so-called “Developed Economies” in the U.S., Europe and Japan are really nothing more than debt-broke economies, veritable banana republics.

This means their economic profiles, and hence economic policies, more resemble those of “Emerging Markets” rather than “Developed Markets.”

And what have we learned of the EM policies from Argentina to Yugoslavia and every other debt-strapped nation in history?

It’s simple: INFLATION MUST BE KEPT ABOVE INTEREST RATES TO REDUCE DEBT BY “INFLATING IT AWAY.”

The Volcker Option is Dead

This means inflation levels in the West can eventually reach a base-case similar to that of the 1970’s, but unlike that Volcker era, today’s drunk central bankers can’t induce a recession (i.e., raise rates above the inflation rate) when the public debt is above $30T rather than $900B level of the Volcker era.

Folks, US debt to GDP is 122% today, under Volcker it was 30%. There is no going back to a Volcker (i.e., rate hike) option. Period.

Stated simply: Short of outright default, the US is in too much debt to conduct anything but an inflationary policy.

The Endless Larry Summers

Meanwhile, an increasingly tired (and let’s be honest, failing) President Biden stands on a Delaware beach and pretends we are good hands, telling reporters he has just been on the phone with none other than Larry Summers to create a plan to fight inflation.

Oh, how the ironies do abound.

Larry Summers, the de-regulating patient-zero of the 2008 derivatives debacle and co-signer to the two most destructive pieces of financial madness since World War II (i.e., the repeal of Glass-Steagall and the 2000 Commodities Modernization Act—aka: Enron “loop hole”), is gonna save us?

From what most know of Larry, he’s always looking for an angle to appear like an expert and be at the center of power, while forgetting to remind anyone, including Ray Dalio, that he has been at the very eye of more than one financial hurricane.

In fact, there’s no one I’d trust less to “solve” any financial problem, including the Harvard endowment, which former University President Summers helped crush in 2008 by filling it with the very same toxic derivatives which he had “de-regulated” a decade prior when I was limping around Harvard Yard.

For now, the endless Larry Summers somehow feels a stronger USD and rising bond yields will give foreigners positive real returns and hence attract badly needed foreign interest in U.S. credit markets, when such a plan is likely to have the opposite effect (as per usual with effectively all of Larry’s “plans”).

Big names like China, and broke names like Japan, as noted above, are selling, not buying our debt.

Instead, by raising rates/yields and tightening rather than easing, the “Summers Solution,” like the Powell policy, will merely hasten the demise of the U.S. economy while simultaneously increasing the risk of a U.S. default.

Why?

Because Larry seems to have forgotten that current US debt levels can’t endure rising yields/rates.

Simple History Lesson: Gold Rises as Currencies Debase

Again, the only option left for a debt-soaked banana republic like the U.S. is to look in the mirror and act like the banana republic that it truly is—which just means more QE will re-appear, and more inflation and more currency debasement lies ahead.

Even commercial banks (Goldman, Citi, JP Morgan, Deutsche Bank) are now extremely risk averse, with bond desks recently refusing to execute client trades if it means holding client collateral (i.e., increasingly toxic bond hot potatoes) for even a brief period.

Without central bank “support” for these toxic bonds, no one wants to touch them—not even the big boys. When liquidity dries up, QE will have to replace current QT.

When that happens, cue the inflation warning bells as more fiat liquidity floods an already-drowning financial system.

See why gold’s golden era has yet to even begin?

Eventually, the rising tide of more debased fiat currencies will be impossible to hide and gold’s openly repressed and manipulated pricing levels will rise from the ashes of a broken financial system and an increasingly neutered/debased USD.