Von Greyerz: There’s No One to Save This Broken System of Debt, War & Currency Destruction

In his first interview with Dunagun Kaiser of Liberty & Finance, Matterhorn Asset Management founder, Egon von Greyerz, offers his insights on the latest geopolitical and financial headlines.

Von Greyerz opens by discussing the patterns and parallels of debt, currency, geopolitics, oil and gold. Specifically, von Greyerz squarely addresses the historical use of war as a disturbing policy tool to excuse debt and justify further expansion of the same. Oil, of course, is often a protagonist in such an historical stage, and von Greyerz considers the various ways in which current conflicts within the Middle East and the Ukraine can escalate into a more global danger. Western policy, he maintains, has a woeful lack of statesmen. US leadership, in particular, remains mysterious, weak and marked by sending money and weapons rather than sophisticated peace negotiators.

War, of course, has immense implications on financial conditions, at home and globally. Wars, von Greyerz reminds, are costly. But where will the money come from given US debt levels? Sadly, the answer is “out of thin air,” a pattern for which markets and central banks are all too familiar. Ultimately, this makes sovereign bonds and currencies in general, and USTs and USDs in particular, increasingly weaker and unloved. This trend, as well as distrust, away from the Dollar has only been accelerated by the weaponization of the USD following the war in Ukraine. Eastern central banks are thus selling USTs and stacking physical gold as confidence in, and trust for, the world reserve currency openly unwinds. This places pressure on credit markets already cracking under the immense weight of grotesquely over-levered derivative markets.

Taken together, these debt, currency and geopolitical risks have created a setting of risk unlike any von Greyerz has seen before. Money printing can no longer solve this convergence of open deterioration. Informed individuals, however, can protect their own financial conditions by doing what their leaders and 99.5% of their peers have failed to do—namely: Protect their purchasing power via direct investment in physical gold, a timeless asset whose real journey has yet to even begin. History, of course, confirms such a minority of investors are always rewarded for thinking carefully, wisely and differently; but as Egon concludes, gold’s rise will be significant, yet sadly because the fall in global welfare will be equally so.

Von Greyerz: There’s No One to Save This Broken System of Debt, War & Currency Destruction

Below, we follow the breadcrumbs of simple math and bond market signals toward an oft-repeated pattern of how once-great nations become, well…not so great any more.

Debt Destroys Nations

Debt, once it passes the Rubicon from extreme to just plain madness, destroys nations.

Just ask the former Spanish, British or Dutch empires. Or ask the inter-war Germans. Ask the Yugoslavians of the 1990’s or ask a historian of Ancient Rome or a merchant in modern Argentina.

It’s all pretty much the same story, just different a different stage or curtain call.

Like Hemingway’s description of poverty, the process begins slowly at first, and then all at once.

Part of this process involves currency debasement needed to pay down more desperate issuance of IOUs, a process evidenced by rising rather than “transitory” inflation.

Thereafter, comes increased social unrest, and hence increased centralization from the political left or right in the name of “what’s best for us.”

Sound familiar?

Centralization—The Last, Failed Act

Centralization never works in the long run, but that has never stopped opportunists from trying.

Just look at our central bankers.

In a centralized rather than free market, the very name “central bank” should be a dead give-away as to their real role and profile.

As private central banks have been slowly increasing their hidden power and control over national markets and hence national welfare, the very notion of free price discovery in bonds, and indirectly in stocks, is now all but an extinct financial creature in the neo-feudalism which long ago replaced genuine capitalism.

How the Central Game is Played—From Temporary Prosperity to Permanent Ruin

When central banks like the Fed repress rates and print gobs and gobs of money, bonds are artificially supported, which means their prices go up and their yields are compressed.

When yields are low, rates are low, which means the cost of credit is cheap, allowing otherwise profitless names in the stock markets to borrow money and time for years of temporary prosperity—like a 600% rise in a post-08 S&P…

In short: central bank repressed rates are a profound tailwind for otherwise mediocre risk assets.

But when central banks like the Fed raise rates (ostensibly to “fight inflation”), the opposite effect happens—and things break. I mean really break.

I’ve written and spoken ad nauseum about what has broken, is breaking and will continue to break; furthermore, I’ve written and spoken at length about the quantifiable irony that Powell’s so-called war on inflation will only end in more inflation.

Yep, the ironies just abound in this world of so-called experts, which is little more than an island of misfit toys.

Postponing Pain Only Heightens It

In normal, free-market cycles devoid of central bank “support,” bonds and hence rates rise and fall naturally based on natural demand and natural supply.

Imagine that?

This leads to frequent but healthy moments of what von Mises and Schumpeter described as “constructive destruction”—i.e., a cleaning out of debt-soaked and crappy enterprises in naturally occurring recessions and naturally occurring market drawdowns.

But central banks somehow thought they could outlaw recessions by printing money out of thin air to support bonds and repress yields. You know—solve a debt crisis with more debt. Brilliant…

This was hubris at the highest level, and the stupid just became a habit and even received a fancy name to justify it—Modern Monetary Theory.

Natural Market Forces Are Stronger than Central (Bank) Forces

But the longer central banks postponed pain to win Noble Prizes and ego-lifting acclaim from the un-informed, the greater the natural pain (ticking time bomb) these central planners created as they now slowly realize that the bond market, like an ocean, is more powerful than a band of unelected market stewards.

In fact, a bunch of FOMC officials (Kashkari, Bostic, Waller et al.) are now running around like headless chickens and declaring that higher bond yields may now be more powerful than the Fed Funds Rate.

In other words, after months of hawkish chest-puffing, they are saying that perhaps enough is enough with the “higher for longer” meme…

Central bankers, it seems, are beginning to realize what informed credit market jocks have always known, viz: The bond market is stronger than any central bank.

Price Matters

That is, eventually central bankers lose control of artificial bond pricing.

Which means that eventually the great weight of sinking bonds and hence rising yields and rates becomes more powerful than central bank money printers to keep those bonds artificially “supported.”

I’ve been saying this for years despite “journalists” at the WSJ and Financial Times calling math-based realists like me “kooks.”

But recently even the fine folks at the WSJ or Financial Times (FT) are beginning to worry out loud as UST supplies far outstrip natural demand, causing bond prices to fall and yields and rates to rise fatally higher than central bankers once thought safely under their control.

We’ve warned of this for years—and this grotesque supply and demand mis-match has only risen exponentially in recent months.

America: Running Out of Takers/Suckers for Its Ever-Increasing IOUs?

The trillions in spending forecasted for year-end and into 2024 just don’t have any real money behind it, which means more IOUs will be spitting out of DC with less and less love/demand for the same.

This, of course, has been a real problem hiding in plain site for a long, long time.

As supply outpaces demand for sovereign bonds, their prices sink, their yields rise and hence interest rates—the cost of debt—becomes fatal rather than just painful.

The journalists at the FT, most of whom never sat at a trading desk, however, still have a very hard time imaging the unspeakable—i.e., a total implosion of sovereign bonds, and hence a total implosion of the financial system.

Thinking About the Unthinkable

They still see the UST as too big to fail—or to use their own words, any failure of this sacred US Sovereign bond is “unthinkable.”

Well…think again.

But at least the main-stream-financial pundits are crying that any real threat to Uncle Sam’s IOUs “would force the state to act.”

For once, I actually agree with these “journalists.”

But let’s clarify what “forcing the state to act” really means—i.e., in simple speak.

When There’s No Good Acts Left to Take

In short, this means the “state” would have to “act” by saving the bond market in particular and the global financial system in general via trillions and trillions of printed dollars to purchase otherwise unloved IOUs from Uncle Sam.

In other words, the only way to save bonds is to kill currencies.

This, by the way, is a now familiar trajectory to any one paying attention (think of the September 2019 repo crisis, the March 2020 Covid crash or the 2022 Gilt crisis in the UK) the implications of which we’ve been warning well ahead of the pundits.

Such “state action,” of course, slowly kills the USD—but as I’ve also warned for years, the last bubble to pop in every centralized, debt-soaked financial failure throughout history is always the currency.

The once exceptional USD, sadly, is no exception. It just takes longer, a lot longer, to bring down a world reserve currency.

This, by the way, is not “gold bug sensationalism” but simple history supported by simple math—two disciplines our leaders, financial journalists and even bankers either don’t grasp or do their best to ignore, cancel or dismiss.

Again, with the ironies.

Even the Media Can’t Deny the Obvious

But at least the main stream pundits are catching on. This is only because the problem of unprecedented deficits alongside rising bond yields and hence debt costs are now too obvious to ignore.

The WSJ recently wrote that “deficits finally matter.”

Hmmm. They have mattered for a long time—just saying…

Telegraphing a Weaker USD?

In the end, and as warned over and over and over (and as confirmed, it seems, even by the squawking Fed officials above), the facts and Fed-speak all point toward a talking down of the USD in favor of Uncle Sam’s broken IOU.

That is, the media is already planting the seeds for the USD’s painful endgame.

This comes as ZERO surprise, despite the Greenback’s relative status as the best horse in the global glue factory.

And, at least for now, that USD is breaking well off its prior uptrend…

This weaker USD will provide needed liquidity relief for an over-stretched UST market.

But the USD (and DXY) will have to come down much further, in my opinion, to buy sovereign bond markets needed time.

Pick Your Poison: Busted Financial System or Neutered USD?

Eventually a choice will have to be made between saving the system (of which sovereign bonds are the foundation) or sacrificing the currency.

In other words, get ready for more dollar-destroying “state action” from that non-state/private enterprise otherwise known as the Fed—all in the form of direct magical mouse-click money.

The Postponed Pivot Already Began

For over a year, this inevitable Fed pivot toward QE was delayed by back-door QE-like measures from Yellen’s Treasury Department (i.e., refilling the Treasury General Account with T-Bills) or the dual (and multi-trillion) accounting tricks of BTFP bank-bailout (by which Uncle Sam guaranteed par value return to the banks but market value losses to the suckers on Main Street…)

Or War Might Be in Order? Ask Hemingway

In fact, the only thing that could publicly justify (and partially absorb) another massive dose of 2020-like money printing (and hence currency debasement) would be a big, fat, ugly war with war-like “emergency measures” whereby our leaders can blame decades of debt-addiction on battle smoke (or COVID, Putin, and men from Mars) rather than their own bathroom mirrors.

Again, Hemingway was likely onto this trend long before the WSJ or FT:

Around and Round We Go

But with conflicts now red hot in both the Ukraine and Israel, Biden and his broken bond market are hitting an inflection point where the USA just can’t really afford more war support to its allies without thinning the USD and over-stretching its UST.

And so, folks… around and round we go in the ultimate vicious circle within which all debt-soaked nations throughout history ultimately find themselves.

That is: 1) poorly managed nations get too drunk on debt, and then 2) debase their currency to pay their debt; thereafter, 3) inflation comes, followed by 4) rising rates to fight that inflation, which in turn means 5) higher debt service costs, which means 6) more inflationary currency creation is rolled out to pay those higher rates.

Stated more simply, the USA has hit the Fiscal Dominance arc of the debt-cycle vicious circle wherein fighting inflation just creates more inflation.

The World Is Catching On…

We, of course, are not the only ones who see this.

In fact, pretty much the entire world is catching on, with the BRICS+ nations making the first steady moves (de-dollarization) as eastern and other central banks continue to stack physical gold at record-levels in preparation for the slow but steady decline (not death, nod to Brent Johnson) of the World Reserve Currency.

As I recently wrote, just like kings bring horses and canons to their borders to defend against an approaching invader, central banks are stacking physical gold to defend against a debased USD.

It’s just that obvious.

This may explain why gold continues to rise in London and NYC despite so-called “positive real rates” and a still relatively strong USD.

That is, the world, including the Shanghai gold exchange, is seeing the golden lighthouse through the smoke of burning currencies.

Are you?

Von Greyerz: There’s No One to Save This Broken System of Debt, War & Currency Destruction

Egon von Greyerz joins his dear friends and Matterhorn Asset Management advisors, Grant Williams and Ronnie Stoeferle, to address the unique risks—economic, geopolitical, military—making headlines at an alarming rate.

This timely and highly important conversation opens with the financial, political and trade moves from West to East as evidenced by the growing BRICS momentum and its near and longer-term impact on the price of gold as prosperity moves from West to East. Consumer gold demand from India and China, increased central bank demand in the East and rising gold premiums on the Shanghai Exchange suggest that the LBMA hegemony over gold pricing is shifting, as Ronnie discusses.

As to rising gold prices, Grant reminds that gold does nothing, currencies just continue to weaken. Strangely, however, investors continue to erroneously wait for gold price spikes before investing in gold, a point which Egon addresses.

Grant unpacks the failure of Western sanctions and the weaponization of the world reserve currency as the key driver away from USDs/USTs and toward physical gold. We are entering a period of tremendous geopolitical shifts for which gold’s role will be central as a wealth preservation asset, a role which Egon has steadily maintained for more than two decades. Despite such a clear direction, many Western individuals fail to make physical gold a core part of their portfolios, an issue which Ronnie addresses at length—giving particular attention to misunderstood bond markets and the total return losses therein.

Grant adds his thoughts on gold allocation percentages in the context of gold’s global market share, which is finite despite fiat money’s infinite (and hence inflationary) range. The West, unlike the East, has not fully understood inflation risk and portfolio reactions to the same.

Egon then asks if we are looking at an existential crisis given increased global conflicts, to which Grant and Ronnie add their insights/concerns. Grant sees a complete failure of diplomacy before, during and after events in Ukraine and Israel made headlines. As Egon argues, it seems the US policy is little more than sending money and weapons at every problem, not statesmen.

Of course, gold can’t protect investors from every risk making headlines today, but it has a clear role in protecting against financial risk, a point which Ronnie, Grant and Egon address at length in the closing minutes of this spirited discussion.

Von Greyerz: There’s No One to Save This Broken System of Debt, War & Currency Destruction

What a bloody mess! Well, economic collapses and wars always are.

But sadly it will become a lot messier!

We now have two dangerous wars, maybe we will have a global war. We have a coming collapse of stock markets and debt markets and a banking system which probably will not survive in its present form.

But there is always another side of the coin.

There will be opportunities of a lifetime not just to preserve your wealth but also to amass an incredible fortune. More later.

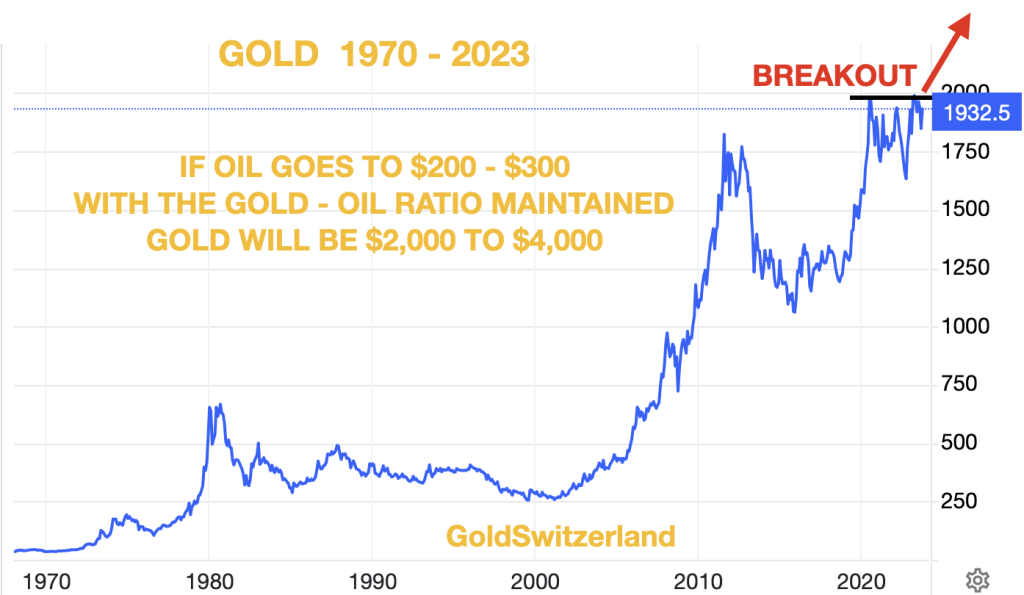

WHERE BLACK GOLD GOES YELLOW GOLD WILL FOLLOW

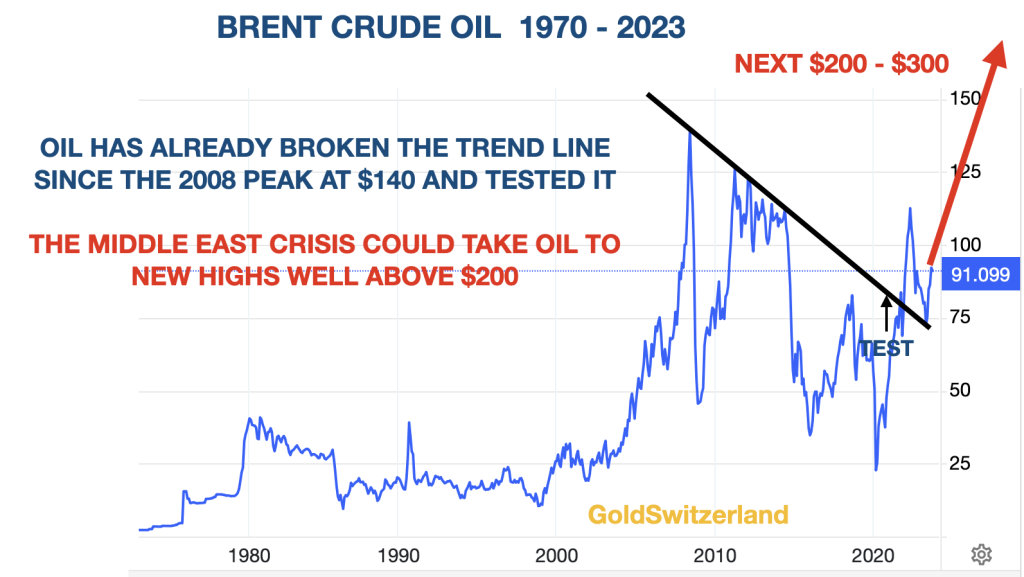

Oil and gold are best friends. As the chart of the Gold – Oil ratio for 50 years shows, below, gold and oil move very much in tandem within a narrow range. So if oil now goes up due to the Middle East crisis, gold will follow.

AS IF CLIMATE CHANGE, VACCINES, LOCKDOWNS, WOKENESS, STOLEN ELECTIONS, CBDC, DEBT etc WASN’T ENOUGH

As if all the above wasn’t bad enough, adding a Middle East war to this makes the crisis properly global and the step toward a Global or World War is very short even dangerously short.

We thought we had enough trouble with climate change, ESG (Environmental, Social, Governance), wokeness with 27 genders and canceling history, forced vaccines and lockdowns, high taxes, high inflation and debt that can never be repaid.

Hard to understand what happened to the world since I was born 78 years ago.

Add to that incompetent governments in the entire Western World and not a single statesman around. All of that is more than most people can cope with.

The US government and Biden have no policy, no ideology. They have also lost their manufacturing base and their military power is declining rapidly.

On top of that, the US is also spending money like a drunken sailor who will never sober up but only spend or drink more to drown his ever increasing debts and sorrows.

And then we started to get used to the “local” war in Ukraine which the poor Ukrainians could never win against a superpower.

We are now talking about the greatest uncertainties in my 78 year lifetime which started at the end of WWII 1945.

No one can predict where the current two wars will lead, although our worst fears can sadly be realised sooner than anyone could believe.

At this stage we cannot say if these crises will lead to a major destruction of the fabric of the world and the death of many, many people.

But what we can say with much greater certainty is that economic and financial risk is now at a level which is likely to lead to the destruction of wealth on a level never before seen in history.

I was born right in between the end of WWII in Europe and before it ended in the Far East. So I naturally don’t remember anything from that era. My father was an officer in the Swedish army at the time and Sweden unofficially assisted Norway which was occupied by the Germans.

But I can well remember my early life in Sweden which was a prosperous and stable country with a homogenous population. The 1950s were a period when church doors were open and the church silver could be left unprotected. Today, the copper roof, the gates and anything of value is long gone. Obviously the silver is either locked in or stolen. Police and teachers were greatly respected with ethical and moral values very high. Now people swear and spit at them.

But the stability of the early 1950s (except for the Korean War) soon led to wars in Vietnam, Middle East etc with the invasion of Hungary and Czechoslovakia and Yom Kippur in 1973 being the first Palestine conflict I can remember. Petrol prices in the UK where I lived at the time were 7.5 pence per litre.

That was the first major oil crisis I experienced. Today petrol in the UK is £1.90 per litre and unlikely to stay that low for long. But a 26X increase in the last 50 years of petrol (US gasoline) is probably going to be seen as a bargain in a few years time.

let’s start with your most important decision which you need to take toDAY

Buy as much physical gold as you can afford and then buy much more.

We have warned investors for some time that the Everything Bubble will turn into the Everything Collapse.

Well that time is now coming very soon.

The current pattern of the Dow looks very similar to October 1987. If that is correct, a stock market crash could be imminent.

Stocks will be down 70-90% or more, in real terms, before this crisis ends.

Most bonds will become worthless, even Sovereign bonds.

Higher rates and defaults will see to that.

So get out of all general stock and all bond investments if you want to have any money left at the end of the coming calamity.

Interest rates will continue the long term, 20-30 year uptrend, obviously with corrections. No one will want to lend to a drunken sailor who can never get sober. Defaults and a banking crisis will lead to higher debts and higher rates. But the US with record borrowings can’t afford the rising interest costs. The dollar will be sacrificed.

So in all a perfect but vicious debt and currency cycle leading to guaranteed perdition.

The only question is how long it takes.

GOLD WILL BE YOUR SAVIOUR

We have been advising investors to hold important amounts of physical gold for wealth preservation purposes since the beginning of 2002. Since that time gold is up 6-8 times in most major currencies and much more in weaker currencies.

But as I keep telling colleagues and investors, gold’s real journey hasn’t started yet.

What I often tell our clients is that they mustn’t wish for gold to go up substantially.

Because when gold goes to the levels which I now feel certain it will, the quality of our lives will be considerably worse than today.

The factors that will fuel gold’s rapid rise to new substantially higher levels are obvious:

WARS

It is both fascinating and frightening to follow how regional disputes lead to superpowers quickly taking sides and lobbying or forcing its allies to follow suit.

There are always two sides to a dispute. One of my very important principles is that before you judge someone, you must walk three moon laps in his moccasins. (An old American Indian saying). But sadly most people including superpowers totally ignore such advice. The Russian argument is that the Minsk agreement was meant to avoid a deepening of the dispute and should have been followed. The US side is that Russia must be stopped at any price and Germany separated from a dangerous rapprochement with Russia. And Europe was given no choice but to follow the US.

As Bush Jr said to congress in 2001:

“Either you are with us, or you are with the terrorists!”

The sanctions are severely affecting Germany and most of Europe but the worst consequences are still to come this winter. The Middle East conflict is likely to make the consequences exponentially greater.

Like with all wars, ordinary people on either side don’t want it. And democracy doesn’t exist when a nation goes to war. Both Ukraine and the US went to war without the consent of either the people or their parliaments.

THAT IS HOW WARS AND WORLD WARS START – Idiosyncratic leaders with sycophantic lieutenants take erratic decisions without understanding the consequences.

WHO IS ACTUALLY RUNNING THE US?

And when the leader is past his sell by date it makes the whole process utterly dangerous.

Everybody gets old and I am no spring chicken either. But if for whatever reason I don’t have the wits to resign when I should, I hope that my wife and my team will tell me so.

IT IS EXTREMELY DANGEROUS FOR A SUPERPOWER TO BE LEAD BY SOMEONE WHO IS NOT CAPABLE OF LEADING.

Even more dangerous when an unaccountable and unidentifiable group takes all the decisions.

UKRAINE AND PALESTINE – REGIONS UNDER CONSTANT STATE OF CHANGE

As Heraclitus, the greek philosopher said 2,500 years ago:

“Change is the only constant in life.”

Modern Ukraine was occupied by a number of different people throughout history like the Scythians, Greeks, Romans, Goths, Huns and the Slavs as well as the Mongols. Later Poland and Lithuania and the Ottomans were involved. In 1709 the Swedish King Charles the XII lost against Peter the Great of Russia due to the Great Frost (the coldest winter in 500 years) which weakened the Swedish Army just like during the Napoleon and Hitler invasions.

So Ukraine is hardly a stable country with deep roots and a homogenous people.

The same with Palestine, the Land of Israel, the birthplace of Judaism and Christianity which has been controlled by, among all, Ancient Egypt, the Persian Empire, Alexander the Great, the Roman Empire, Muslim Caliphates, the Crusaders, the Ottoman Empire and the British Empire after WWI. In 1948, Britain divided the region into Israel, the West Bank and Gaza.

The history is too long and complex to delve into the details here but suffice it to say that the modern split of the region has created a constant period of dispute (constant change again), misery, wars and deaths.

No one is prepared to wear the other side’s moccasins and the situation could now escalate to a world war between the Muslim world and the West. This is likely to result not just in a major war but also terrorism around the world.

Just like in Ukraine, the US and the West are more likely to send money and weapons to the Middle East rather than to peace makers.

It is unfathomable that the West chooses war over peace. This certainly does not bode well for a peaceful solution to the two conflicts.

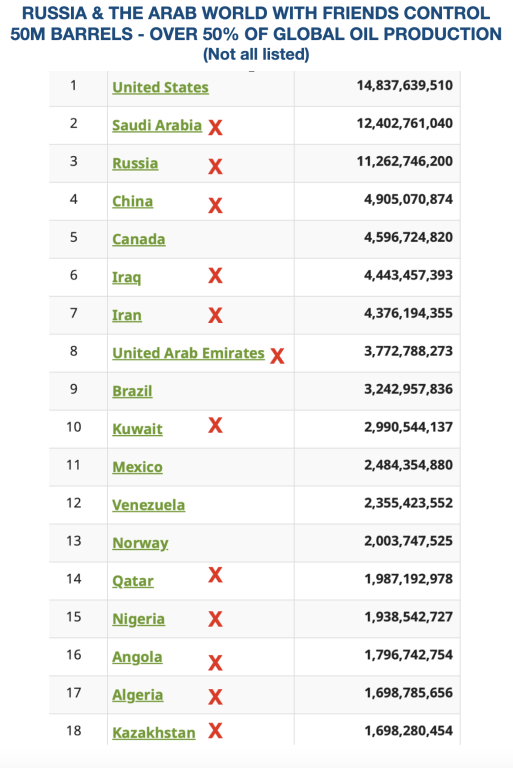

OIL

Since most wars in modern times involve oil, the current ones are no exception.

There are two major camps controlling the global oil supply.

Around 22 million barrels of oil go through the Strait of Hormuz between Dubai and Iran.

It would be virtually impossible to prevent Iran from blocking this area off, stopping all shipments of oil and gas, if necessary with the help of Russia.

That would turn off 22 million barrels of oil or 23% of global supply. Enough to make the oil price go to $500 – $1,000 and paralyse the world.

DEBT AND CURRENCY COLLAPSE

I have since the 1990s been certain that the world economy would end in a debt and currency collapse. That is a very obvious projection since history always repeats itself, or rhymes, and every economic period in history ends this way.

The difficulty is to time the cycle but as I often stress, exact timing is less important. The key is to prepare early and buy the fire insurance or protection well before the fire starts.

So whether we call it a Fourth Turning like Neil Howe or a debt and currency collapse like von Mises, the end result is the same and devastating.

When I discuss my economic scenario most people (but obviously not our clients) call me pessimist or a prophet of doom and gloom.

But I am an optimist and consider life to be a wonderful journey. The key is to help other people, family, friends, and clients. Real happiness is making other people happy. It clearly doesn’t always work with people who believe you are a prophet of doom and gloom. But it does work extremely well for people who need help.

So enjoy life with family, friends, nature, music, books etc for as long as you can. Remember that the quality of your life is determined by how you deal with adversity.

JIM SINCLAIR – MR GOLD

Our good friend Jim Sinclair died last week of a heart attack. Since the 1970s he has been one of the foremost gold experts in the world. He traded the whole run from $35 in the early 70s to $850 in 1980 where he got out making substantial returns.

Above all Jim was Mr Gold with a superb understanding of the world economy, markets, politics, wealth preservation and of course gold.

Many people around the world followed his wisdom through his website JS Mineset.

I had the privilege of meeting Jim many times around the world. He was always gracious with his advice and support. He often told investors to “Go to Egon” and posted both my mobile number and private email on his site. At times we were totally inundated with potential clients. He had a tremendous following.

We will miss you greatly, Jim. I know that you wanted to experience the coming surge in gold that took longer than many of us expected. But you always knew that this move was inevitable. Still, your legacy will certainly be with the whole gold community and we will send you thankful thoughts regularly as gold continues to move up.

Von Greyerz: There’s No One to Save This Broken System of Debt, War & Currency Destruction

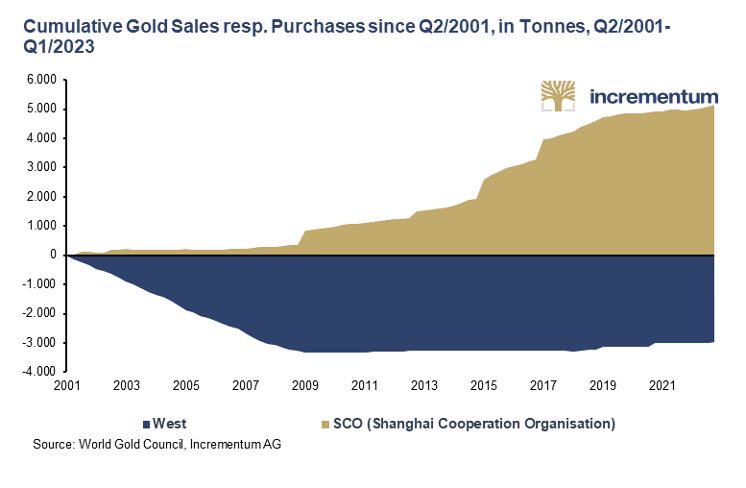

The reshaping of the world economy and the global (political) order is in full swing. It is a long process, the concrete outcome of which is uncertain in advance and associated with numerous imponderables. Nevertheless, there are powerful factors, such as the shift in economic, demographic and military weight, that are driving the readjustment in the (geo)political arena. And this readjustment is also reflected in the change in gold flows. They are increasingly shifting from West to East, since “Gold goes where the money is,” as James Steel pointedly put it.

The central banks of the states of the East are among the strongest buyers of gold – also within the West

This is also reflected in the continuing enthusiasm of central banks for gold, especially in non-Western countries. 2022 saw the largest purchases of gold by central banks since records began more than 70 years ago, at 1,136 tons. The first half of 2023 saw a continuation of this trend. Despite a weaker second quarter, central bank purchases in the first half of the year set a new half-year record. Central banks increased their gold reserves by a total of 378 tons from January to June. The previous half-year record from 2019 was thus slightly exceeded. China made the largest purchases, followed by Singapore, Poland, India and the Czech Republic. So even in the West, it was countries in the East that made additional purchases.

The following chart shows the extent to which institutional demand for gold has shifted to the East. It compares the cumulative gold sales of Western central banks with the cumulative gold purchases of the Shanghai Cooperation Organization (SCO or SOC) since 2001.

Looking at the BRICS, we also see a striking overlap, with central banks from four of the five BRICS countries – Brazil, Russia, India and China – buying a cumulative 2,932 tonnes of gold over 2010–2022.

Holdings of US Treasuries are reduced

In turn, the BRICS continue to reduce their share of the soaring US government debt. In other words, gold is becoming more and more interesting as a reserve asset because US Treasuries have been becoming less and less interesting as a currency reserve for more than a decade. The militarization of money by freezing Russia’s foreign exchange reserves just days after Russia’s invasion of Ukraine in late February 2022 added emphasis to this process, but did not kick it off.

The BRICS now hold only 4.1 percent of all US government debt, compared with 10.4 percent in January 2012. That is a decline of more than 60 percent. The rest of the world has reduced its exposure to US government debt by much less. In January 2012, the rest of the world held 22.0 percent of all US government debt on their books; currently, they hold 19.3 percent. That is a decrease of more than 12 percent.

The East is expanding its infrastructure for gold trading

However, the East is not only stocking up on gold and mining gold itself on a large scale. China and Russia have ranked among the top 3 gold producing nations for years.

Countries such as China, the United Arab Emirates and even Russia are expanding their gold trading infrastructure. This is to establish a permanent infrastructure for the detour of gold trading from gold trading centers in the West such as London, New York and Zurich. This testifies to the changing understanding of roles: The East increasingly no longer sees itself as a customer of Western infrastructures, but offers the infrastructure itself.

Key developments include:

- SGE & SFO NRA: Cooperation between the Chinese and Russian gold markets

For some time now, China and Russia have been working hard to link their gold markets through cooperation between the Shanghai Gold Exchange (SGE) and the Russian financial authority, the National Financial Association (NFA). The NFA is a Russian professional association representing the entire Russian financial sector, including the Russian precious metals market.

In the face of Western sanctions, Russian gold exports to China have already surged since mid-2022. As three Russian banks – VTB, Sberbank and Otkritie – are already members of the SGE International Board of the SGE, which was founded in 2014, this cooperation between the gold markets of Russia and China is likely to intensify in the future.

- Memberships in gold-related institutions

As gold flows from west to east and the importance of eastern gold markets increases, these markets will also have greater representation and influence in the global institutions that represent the gold market, such as the LBMA and the World Gold Council (WGC).

In 2009, only six Chinese refineries were on the LBMA’s Good Delivery List, but now there are thirteen. While just 15 years ago there was only one regular (full) member of the LBMA from China, the Bank of China, there are now seven. China’s growing influence is also reflected in the World Gold Council. In February 2009, only one Chinese gold producer was a member of the WGC; now there are four.

- India International Bullion Exchange (IIBX)

In addition to its sophisticated OTC gold trading market, India has also established a trading infrastructure for gold futures contracts on the Multi Commodity Exchange of India Limited (MCX). In July 2022, the India International Bullion Exchange (IIBX), supported by the Indian government, was officially opened for trading spot gold contracts backed by physical metal. IIBX is located in a special economic zone in GIFT City in the Indian state of Gujarat, and the gold underlying the contracts is stored there. One goal of IIBX is to allow qualified buyers to import gold directly into India without the need for banks or authorized agencies. So far, however, trading volumes have been minimal.

- Establishment of a Moscow World Standard

At the end of February 2022, when sanctions against Russia were imposed by the West immediately after the start of the Ukraine war, the London Bullion Market Association (LBMA) excluded the three Russian banks VTB, Sovkombank and Otkritie. A few days later, the LBMA removed all six Russian precious metals refiners from the LBMA Good Delivery List and the CME Group followed suit, removing the same refiners from the list of approved COMEX refiners.

As a result, Moscow announced in July 2022 that a new infrastructure for precious metals trading independent of the LBMA and COMEX would be established. According to Moscow, this is intended to break the supremacy of London and New York in global precious metals pricing. This proposal calls for the introduction of a Moscow World Standard (MWS) for precious metals trading, similar to the LBMA’s Good Delivery List, the establishment of a new international precious metals exchange in Moscow based on the MWS, the Moscow International Precious Metals Exchange, and the creation of a new gold price fixing based on the MWS so as to establish gold prices and reference prices different from those of the LBMA and COMEX.

Private gold demand shifts to the east

EAST’S increased interest in gold is also evident in the non-governmental sector. Chinese consumer demand, for example, increased from 292.6 tons to 824.9 tons (2022) since the turn of the millennium. This is an increase of 181%. Annual consumer demand in India has also increased since the turn of the millennium, albeit from an already high level in 2000. China and India, which together accounted for only 28.7% of consumer demand in 2000, account for almost half of global consumer demand (48.4%) in 2022 and together acquired 1,600 tons of gold last year.

Consumer Demand for Gold – 2000 vs. 2022

| 2000 | % of Global Demand | 2022 | % of Global Demand | 2022 vs. 2000 in Tonnes | 2022 vs. 2000 in % | |

| India | 723.0 | 20.4% | 774.0 | 23.4% | 50.0 | 7.0% |

| China | 292.6 | 8.3% | 824.9 | 25% | 532.3 | 181.9% |

| Japan | 105.1 | 3.0% | 4.3 | 0.1% | -100.8 | -95.9% |

| Middle East | 457.9 | 12.9% | 268.2 | 8.1% | -189.7 | -41.4% |

| Türkiye | 177.4 | 5.0% | 121.5 | 3.7% | -55.9 | -31.5% |

| United States | 368.5 | 10.4% | 256.6 | 7.8% | -111.9 | -30.4% |

| France | 19.0 | 0.5% | 19.9 | 0.6% | 0.9 | 4.5% |

| Germany | 15.6 | 0.4% | 196.4 | 5.9% | 180.8 | 1,159% |

| Italy | 92.1 | 2.6% | 17.8 | 0.5% | -74.3 | -80.6% |

| UK | 75.0 | 2.1% | 35.6 | 1.1% | -39.4 | -52.5% |

| Rest of Europe | 142.4 | 4.0% | 115.1 | 3.5% | -27.3 | -19.2% |

| Other | 1,076.0 | 30.4% | 669.1 | 20.3% | -406.9 | -37.8% |

| Global Demand | 3,544.6 | 100.0% | 3,303.3 | 100.0% | -241.3 | -6.8% |

Source: World Gold Council, Incrementum AG

Recent developments point in the same direction. In the first eight months of the current year, Asian gold ETFs increased their holdings by 7.7%, while North America and Europe recorded outflows of 2.3% and 6.1%, respectively. Significantly, in the bars and coins demand segment, Turkey and Iran replaced Germany and Switzerland in the top 5 in the first half of the year. China now leads this sub-segment of gold demand – in the first half of 2022, Germany was still in the lead – followed by Turkey, the US, India and Iran. This is because while demand for bars and coins in Turkey shot up from 9.5 tons to 47.6 tons in the second quarter of 2023, it fell by around three quarters in Germany.

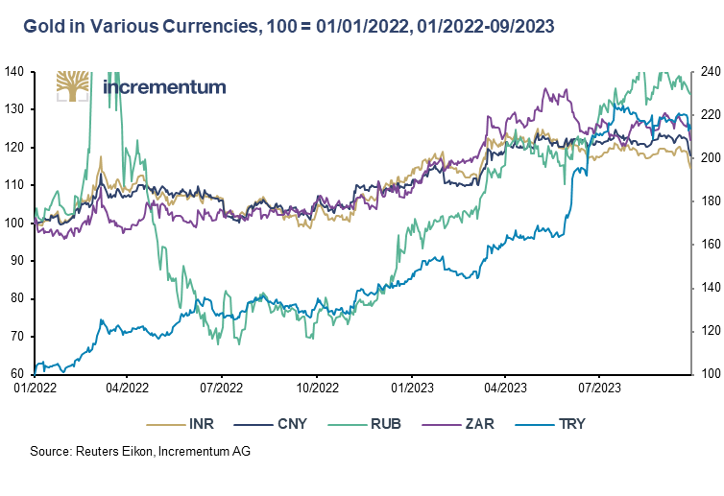

The price of gold in currencies of the East has increased significantly

As of the end of September, gold was 14.6% higher in Indian rupees than at the beginning of 2022, 18.0% higher in Chinese renminbi, 34.3% higher in Russian rubles, 22.1% higher in South African rand (all left-hand side) and 114.0% higher in Turkish lira (right-hand side). Gold thus impressively demonstrates its value-preserving properties in difficult (geo)political and macroeconomic situations in these countries.

The significantly increased premium on the gold price in China since July is an unmistakable sign that there is a structural shortage of gold in the Chinese market and thus an expression of the strong demand for gold in the Middle Kingdom, which is struggling with profound economic problems.

Conclusion

This shift in demand from West to East can be observed not only among governments or government-related entities, but also among institutional and private investors. Gold is flowing to where it is most valued and where economic prosperity and savings rates have increased. In the medium term, the shift in demand should therefore find support from the higher growth prospects in Asia and the Middle East. “Ohne Geld, ka Musi” (“Without money, no music”) – this is how the vernacular formulates this economic truism in German. And as the IMF’s most recent economic growth forecast indicates, the sub-region of emerging and developing Asia will grow at a projected 5.2% this year and 4.8% next year, while the West will grow much less strongly. This will also lead to a shift in influence on pricing from West to East.

Von Greyerz: There’s No One to Save This Broken System of Debt, War & Currency Destruction

In this brief yet substantive MAMChat, Matterhorn Asset Management principals, Egon von Greyerz and Matthew Piepenburg, address the overlay of escalating geopolitical tensions, oil markets, currency direction and, of course, gold’s critical and increasingly obvious role in preparing for the same.

Egon opens by asking a repeated question: “Is this fall the fall of falls?” Specifically, he addresses rising risk levels from inflation forces, unsustainable debt levels and toping markets to banging war drums, which sadly, are a fundamental symptom and aspect of debt cycles and debt crises. Naturally, tensions in the middle east will have ripple effects in oil markets which in turn impact the USD and hence gold, a theme which Matthew addresses in greater detail.

Specifically, Matthew discusses the double-barreled stresses on US oil production as a result of increased CAPEX costs on the back of Powell’s rising rate policies and the negative impact Biden’s pro-Green, anti-oil policies have had on US oil production. Strategic Petroleum Reserves, last year at over 650 million barrels, are now clocking in at 350 million barrels, and thus getting dangerously closer to supply-driven price hikes. Adding insult to injury, we are also seeing sanctioned nations like Iran, Venezuela and Russia selling oil outside of the USD to oil-thirsty nations like China, all of which point toward a slow drip away from the Petrodollar, which will impact Dollar-demand. Longer term, this will mean more artificial USD production and hence currency debasement in favor of precious metals.

This all-too-familiar (as well as historically-confirmed) interplay of debt, currency debasement, inflation and war is theme to which Egon returns in the concluding remarks. Gold, of course, can not and will not solve all of the myriad problems—political, military and social—making headlines at increasing speed today. Nevertheless, gold’s role as a preservation asset against undeniably weakening fiat money around the world is now undeniable. As Matthew then adds, once the role of gold is fully understood, it is equally critical for investors to understand the best jurisdictions to store this asset as well as the need to avoid paper gold in ETFs and gold “storage” in fractured and levered commercial banks.

Von Greyerz: There’s No One to Save This Broken System of Debt, War & Currency Destruction

In Part II of his conversation with Wealthion founder, Adam Taggart, Matterhorn Asset Management partner, Matthew Piepenburg, transitions from the broader (and increasingly unsettling and fractured) macro themes of Part I to addressing specific portfolio approaches and viable asset classes for concerned and informed investors.

Taggart reminds that despite Piepenburg’s longer-term expectation of debilitating inflationary forces, that nearer-term deflationary or dis-inflationary forces from falling markets and recessionary economies are expected. This view provides a needed context for portfolio preparation today.

Piepenburg, like many clear-eyed portfolio managers, argues that further Fed liquidity, and hence further market support/tailwinds, won’t emerge until after risk asset markets in general, and equity markets in particular, experience at least a 30%-40% mean-reversion/drawdown.

In short, the Fed won’t pivot until markets inevitably puke.

This means investors currently falling for the “soft-landing” narrative and chasing stock market tops are doing so at unacceptable risk.

Piepenburg further reminds that investment advice does not come in a one-size-fits-all package, as there are clear and legitimate differences between those seeking (understandably) to grow wealth and those seeking (understandably) to preserve wealth.

Furthermore, there are those who have the experience to invest on their own; whereas the vast majority rely on third-party advisors. To this later group, Piepenburg underscores the importance of vetting and selecting sober portfolio managers who: 1) prioritize risk management over lofty projections in these topping markets; 2) understand the importance of cash equivalents and short-duration sovereign bonds as an allocation and risk tool; and 3) who have the proven ability to hedge, both long and short. This final skill of active, rather than passive management, is admittedly difficult for even seasoned portfolio managers as volatility twists and turns dramatically.

Overall, Piepenburg aggressively warns against the consensus-think faith in traditional risk parity portfolios of de-worsified equities and de-worsified credits. Given unhinged, post-08 monetary policies by all the major central banks, both stock and bonds are simultaneously over-valued. This means bonds, once designed to hedge stock risk, are now correlated assets and hence correlated risks.

Naturally, Piepenburg addresses his preference and style of wealth preservation through real assets in general and precious metals in particular. Although everyone claims to buy low and sell high, nearly no one actually does this. Toward this end, Piepenburg prioritizes longer-term investing and preservation goals, as well as tracking commodity cycles against stock cycles. In the end, the next many years will reward those who understand these relationships.

The conversation briefly returns to, and ends with, current political and financial leadership and the implications going forward, both optimistic and pessimistic.

Watch part 1 here.

Von Greyerz: There’s No One to Save This Broken System of Debt, War & Currency Destruction

In his latest (two-part) conversation with Wealthion founder, Adam Taggart, Matterhorn Asset Management partner, Matthew Piepenburg addresses the broader global risks as well as specific market signals to make the complex simple for global investors.

In short, Piepenburg separates the media fog from the clear lighthouse signals of historically unprecedented and unsustainable debt levels. Those who follow the lighthouse, he maintains, are better equipped to make it safely to shore.

Piepenburg discusses the importance of employing empirical facts to make sense of otherwise “Truman Show-like” attempts by global policy makers to replace hard evidence with empty platitudes. In particular, Piepenburg addresses the string cite of data points which show that not only are US and global markets far from a “soft landing,” but already deeply careening into a hard-landing, the ignored evidence of which is literally all around us.

Toward this end, Piepenburg touches upon the sin, as well as orchestrated strategy, of deliberate omission used to hide disturbing market and economic indicators, all of which support inevitable stressors in risk assets as well as Main Street unrest. Piepenburg reminds that such fact-based realism can no longer be disregarded as mere “gold bug” cynicism.

Piepenburg opens with a sober assessment of unsustainable and ever-climbing debt levels at the home of the World’s reserve currency. The mismatch between increasing UST supply (and debt levels) and declining trust and demand for the same points toward greater pressure on falling credit markets, rising bond yields and unpayable (rate-driven) debt costs. In the end, Piepenburg sees an unavoidable reversion to inflationary money creation to monetize sovereign bonds following a deflationary/recessionary fall in global markets. Ultimately, central banks will be forced to chose between saving their “system” or sacrificing their currency. Piepenburg concludes that history, without exception, tells us the last bubble to pop is always the currency.

The conversation eventually turns to declining trust in political and financial leadership as markets, bonds and currencies limp toward a fiscal cliff which can no longer be blamed on a pandemic, Russian bad guy, global warming or little green men from Mars. This leads toward a deeper dive into inflationary/deflationary forces, currency direction, de-dollarization and, of course, physical precious metals. Here, Piepenburg speaks to the obvious implications of the record-breaking stacking of physical gold by global central banks as both a symptom and solution to growing global distrust in fiat money and unloved, over-issued sovereign bonds.

In Part II of this conversation (released tomorrow), Piepenburg then speaks to portfolio and investor responses/solutions to these increasingly difficult macro conditions.

Von Greyerz: There’s No One to Save This Broken System of Debt, War & Currency Destruction

In many recent articles and interviews, I’ve warned that Powell’s “higher for longer” war against inflation will actually (and ironically) lead to, well… greater inflation.

That is, the rising interest expense (nod to Powell) on Uncle Sam’s fatally rising 33T bar tab will inevitably need to be paid with an inflationary mouse-clicker at the Eccles Building.

I’ve also consistently maintained that Powell’s war on inflation is mostly just optics, as he secretly seeks inflation to help pay down that bar tab with an increasingly inflated/debased USD.

Powell achieves this open lie by publicly declaring a steady decline in inflation by simply misreporting the true CPI number.

As John Williams recently argued, true inflation using an honest (rather than the openly bogus BLS) measure is now closer to 11.5% rather than the officially reported headline rate of 3.7%.

This should come as very little surprise to those whose eyes are open to the Modis Operandi of debt-soaked/failed regimes. As former European Commission President, Jean-Claude Juncker confessed: “When the data is too bad, we just lie.”

But even for those who still believe the current Truman Show inflation (and “soft landing”) narrative out of DC, the Bezos Post or legacy media A, B, or C, there’s more fire adding to the inflationary flames than just bogus narratives and calming platitudes.

In particular, I’m talking about oil-driven inflation, and nothing burns faster.

Scary Flames in the Oil Supply

Left or right, the dumb out of DC just keeps getting dumber.

Between rising rates (nod to Powell), which make capex investing untenable for US oil producers, and a Weekend at Bernie’s White House, which has spent years effectively legislating US oil into oblivion, US energy supply is falling, and we all know that weakening supply leads to higher prices—and inflation.

Meanwhile, Saudi Arabia, whom that same White House called a “pariah state,” has not been warming to Biden’s awkward fist-pumps and increased production pleas, but rather joining other OPEC leaders in cutting, rather than expanding, oil production.

Gee, what a geopolitical shocker…

Net result, both national and global oil inventories are falling, and falling hard.

The Awkward Oil Two-Step

The once “go green” White House realized that the world, and inflation scales, still revolves around oil, especially after sanctioning Western Europe’s former energy supplier in one of the most short-sighted (i.e., stupid) policy decisions since the Iraq war.

This may explain why Biden changed his stripes and why there was a sudden pivot toward allowing greater US shale output in 2023 by pumping more cash into those shale fields at a pace not seen in 3 years.

Unfortunately, however, this may be too little too late (like Powell’s QT) to prevent oil price shocks and higher inflation into year end, thus adding insult to an already injured (and rising) US CPI measure of inflation.

As oil supply tightens, oil prices, and hence inflation rates, rise together with bond yields and interest rates—a perfect storm for over-inflated bond, stock, and real estate markets.

Those prices and inflation rates would be even worse if Chinese oil demand rises—which is why current Western headlines are literally praying for China to implode first. This might explain why The Economist has had two consecutive cover stories about an imploding China.

See how big media and big government sleep together?

Tying it Together

Regardless, we need to tie all this together.

If, as I see it, inflation (however misreported) becomes obviously more real and felt, the consequent rising bond yields will make the USD stronger and Uncle Sam’s bar tab more expensive, which hardy bodes well for America’s twin deficit black-hole of unpayable debt unless…

…Unless the Fed starts printing more fake and inflationary money to buy its own IOUs and weaken its export-killing, and BRICS-ignoring, USD.

Again, no matter how I turn the macros, the Fed will eventually have no choice but to pivot toward more instant liquidity and hence more inflationary policies to save/monetize its broke(n) bond markets.

Once this inevitability becomes a headline, the temporarily rising USD will be seen for what most of the informed world already recognizes—just another fiat monster backing a world reserve currency in the hands of a nation whose debt to GDP and deficit to GDP ratios mirror that of any other banana republic.

Reality is Hard to Look at Directly, But not for the BRICS

Many in the US or EU may not wish to see this. Bad news, like death and the sun, is hard to stare into.

But the BRICS nations, no strangers themselves to embarrassing balance sheets, are seeing this clearly.

Although I never bought into the gold-backed BRICS currency hype, I have zero doubt that this amalgam of commodity-heavy nations has a common enemy in the current US-dominated (and USD-driven) international trade system, whose hegemonic days are now numbered and whose alliances, as we warned from day-1 of the Putin sanctions (economic suicide), are forever de-dollarizing away from DC.

Moreover, the BRICS don’t need an “official” gold backed currency to trade their real assets in gold rather than Dollars. All they have to do, as Marcus Krall and I recently discussed, is request payment for their exports in gold.

The BRICS+ nations are hardly the perfect marriage of unlimited trust and efficient coordination. Nevertheless, they share an existential threat from an over-priced USD and negative-returning UST.

Furthermore, and as I recently noted at the Rule Symposium, they may not trust each other completely, but they do trust gold completely.

System Change is Now a Matter of Survival

Never has the phrase the “enemy of my enemy is my friend” found a better home than among the rising list of BRICS+ actors who recognize that their very survival hinges upon escaping the suffocating death of paying > $14T of USD-dominated debts whose rising costs (rates) they can no longer afford lest they become vassals of DC.

As Luke Gromen recently observed, from the perspective of the BRICS nations, it’s “either hang together or hang separately.”

A Changing Petrodollar?

China, for example, can not abide forever by a petrodollar system of oil purchases. As the world’s largest oil importer, it mathematically recognizes that it will eventually run out of dollars to buy that oil.

In short, China needs to come up with a better plan—outside the Greenback.

And they will.

By the way, have you noticed the next BRIC in the wall? It’s Saudi Arabia.

See a trend? See a looming change in oil currencies?

Just saying…

As I warned months ago, this Saudi trend away from DC and closer to Shanghai could eventually be a key driver in slowly unwinding the current petrodollar system between a once “friendly” US-Saudi relationship toward a now weakening relationship which hitherto ensured the global demand (and hence the survival) of an otherwise debased paper Dollar.

If the petrodollar system radically or even slowly unwinds, this will do far more to destroy demand and the inherent purchasing power of the USD (and send gold skyrocketing) than any gold-backed BRICS trade currency.

And yet with all the recent sensationalism preceding the BRICS summit in South Africa, almost no one saw this—at least not in the legacy media.

Imagine that…

Other Tricks Up the BRICS Sleeve: More USD Assets than Liabilities

Aside from knee-capping the USD via a shift (gradual or sudden) in the petrodollar trade, it’s worth noting that but for South Africa, the remaining BRICS nations have more USD assets than liabilities, which means they can start dumping USTs to the detriment of Uncle Sam in order to raise USDs.

Many idealogues and US-thinktankers still think the US has all the power over these silly little BRICS nations who allegedly suffer from a dollar shortage.

The chest-puffers still see the USD as all-powerful and all-controlling, after all, just ask Iraq or Libya…

But the dollar-forever crowd is missing the forest for the trees or the basic math of fantasy debt.

If you haven’t noticed, the US just added an extra $1.9 trillion of insane borrowing to the back end of 2023.

And they did this as rates are rising and with the Fed still in full QT/suicide mode.

This mathematically places downward price pressure on bonds and hence upward cost pressure on yields, a scenario America simply can’t play out for much longer at $95T+ in combined public, household and corporate debt.

If the BRICS nations chose to add a layer of US asset dumping to this toxic mix, the ramifications for Uncle Sam would be even more staggering/painful for a debt-based system already on the cliff’s edge.

This is Bad, Really Bad

To repeat: The macros, no matter how I turn them, have never been this bad, this vulnerable and this foreseeable.

The US is now trapped in a vicious circle of debt for which there is no way out other than a currency-destroying return to more artificial, QE “stimulus” and the mother of all inflationary waves.

The horizon is now clear: Yields are up, twin deficits are up, inflation, even the mis-reported kind, is up, and yes, GDP is up too, but as I recently wrote, debt-driven GDP growth is not growth, but just debt.

Unless DC cuts spending at record levels (which kills election results for political opportunists and thus won’t happen), the only tool Washington DC has is more fake money and more real inflation, which means the Dollar in your wallet, checking account or portfolio is about to insult you.

Von Greyerz: There’s No One to Save This Broken System of Debt, War & Currency Destruction

Matterhorn Asset Management partner, Matthew Piepenburg, sits down with Rick Rule and Jim Rickards at the recent Rick Rule Precious Metals Symposium to discuss the future of the USD, the rising BRICS tide and the Realpolitik of any realistic (i.e., immediate) gold-backed BRICS trade currency.

Each of the trio share their views on the de-dollarization trend, with Piepenburg and Rule taking a far less optimistic view of any immediate gold-backed trading currency emerging among the BRICS nations in 2023.

Toward this end, Piepenburg argues that not even BRICS nations are ready to limit themselves or their financial powers to a gold-backed trading currency; and certainly not to a gold-backed sovereign currency. That said, all agree that the weaponized USD is losing trust and that the UST is losing demand as a post-sanction world moves further and further away from Dollar-based trade agreements.

For Piepenburg, the end-game is clear. Debt drives policy and debt drives current market directions. This debt will not and cannot be sustained by GDP growth or tax revenues, which means ultimately money printers will continue to de-value that world reserve currency, and hence devalue the once hegemonic respect for the US holder of that currency. All agree that gold’s role in protecting investors from this increasingly beleaguered, self-destructive, debased and less popular US currency is becoming increasingly clear.

Von Greyerz: There’s No One to Save This Broken System of Debt, War & Currency Destruction

This 25 minute video with Matthew Piepenburg and myself is probably one of the most important discussions that we have had.

For years we have both warned investors about the consequences of a system based on unlimited money printing, debt creation and money debasement.

The world economy and the financial system is now on the cusp of a precipice.

No one can forecast when the coming violent turn will come.

It can take years or it can happen tomorrow.

Future historians will tell us when it happened.

In the meantime investors have one duty to themselves and their dependents which is to protect their wealth from total destruction.

Money printing and debt creation have taken markets to dizzy and unsustainable levels.

Since Nixon closed the gold window in 1971, both global and US debt is up over 80X!

And asset markets have been inflated by this fake money with the Nasdaq up 120X and the S&P up 44X since 1971.

But the bubbles are not just in stocks but also in bonds, property, art, other collectibles etc, etc.

In our view, the time to pay the Piper is here and now. The consequences will be costly, even very costly for the investors who ignore this major risk.

Just as bubble assets can go up exponentially they can implode even faster.

RISK OF MARKETS FALLING 50-90%

Sustained corrections of 50% to 90% in stocks and bonds are very possible and when the bubble bursts it will go so fast that there won’t be time to get out or to buy insurance.

Whether the Everything Bubble turns to theEverything Collapse today or tomorrow, the time to protect your assets is before it happens which means NOW.

Forecasting the gold price is a Mug’s game . But understanding the significance of gold for protecting against unprecedented risk is not. We had the Ides of March in mid March this year when 4 US banks, led by Silicon Valley Bank and Credit Suisse, Switzerland’s second biggest bank all went under in a matter of days.

That was a rehearsal. Bad debts and rising interest rates are a timebomb for the banking system. So is the $2-3 quadrillion derivatives risk. This gargantuan risks are before us now and could materialise at any time starting this autumn.

The risk ofA Catastrophic Debt Implosion is just too big to ignore.

In our video discussion below Matt and I discuss these risks and most importantly, the best way to protect or insure against this risk.

Owning physical gold outside the banking system is by far the superior method to preserve wealth.

But it is not just about buying physical gold but how you own it, where you store it, in what jurisdictions etc.

This is an area which MAM/GoldSwitzerland has focused on for a quarter of a century and has developed a superior system for HNWIs.

Please watch this important discussion.

Egon von Greyerz

Von Greyerz: There’s No One to Save This Broken System of Debt, War & Currency Destruction

In this brief yet engaging conversation at the recent Rick Rule Symposium in Florida with Charlotte McLeod of Investing News Network, Matterhorn Asset Management partner, Matthew Piepenburg, calmly separates harsh realities from BRICS hype with regard to the de-dollarization themes of 2023.

After a brief discussion on Piepenburg’s path to precious metals and role at Matterhorn, the conversation turns to Piepenburg’s understanding (and prioritization) of risk management and wealth preservation. Piepenburg sees the lack of such risk thinking as a central concern and open threat to personal wealth in a current backdrop of artificially elevated markets and herd-buying/chasing of unsustainable market tops.

Equally ignored is the hidden risk of currency debasement slow-dripping in real time as debt levels cross the Rubicon of sustainability. Piepenburg argues that “soft-landing” narratives of late are far too soon to call, and that evidence of current and pending “harder landings” are all around us.

Piepenburg keeps it simple. If we assume the US will not allow sovereign bonds to fail or deficits to contract, we can easily foresee more synthetic liquidity, and hence inflation, as the longer-term endgame.

Piepenburg also addresses the “horrifying” profile and slow rollout of CBDC in the years ahead.

As to the BRICS narrative and the rising headlines around a gold-backed trading currency emerging from the August BRICS conference, Piepenburg is far less sensational. Despite his open concerns for the USD and the clear evidence of post-sanction de-dollarization trends, he is not holding his breath for any immediate and gold-backed trading currency to de-throne the USD. Instead, Piepenburg foresees rising inflation forces, continued currency debasement and increasing evidence of centralized controls over our personal and financial lives—all of which make a strong case for owning physical gold outside of the global commercial banking system.