Gold’s Climb Amidst Wisdom’s Decline

As the latest headlines from the FTX implosion remind us yet again of a politicized and rigged market riddled with deception, gold’s climb becomes easier to foresee.

But first, a little philosophical musing…

Modern Policy: High Office, Low Wisdom

I have often referred to La Rochefoucauld’s maxim asserting the highest offices are rarely, if ever, held by the highest minds.

Nowhere has this been more apparent than among the halls of the physically impressive yet intellectually vacant Eccles Building on Constitution Ave in Washington DC, where a long string of Fed Chairs have been un-constitutionally distorting free market price discovery for over a century.

The media-ignored levels of open fraud and inflationary currency debasement which passes daily for monetary policy (namely monetizing trillions of sovereign debt with trillions of mouse-clicked Dollars) within the FOMC would be comical if not otherwise so tragic in its crippling ripple effect to the Main Street citizen.

From Greenspan to Powell, we have witnessed example after example of error after error and gaffe after gaffeon everything from mis-defining inflation narratives as “transitory” to re-defining a “recession” as non-recessionary.

And all this while the Fed (and its creative writing team at the BLS) simultaneously and deliberately fudges the math on everything from misreported CPI data to artificial U6 employment statistics.

Pondering the Philosophically Nobel Amidst the Administratively Dishonest

To any who have pondered the philosophical pathways (as well as elusive definition) of wisdom (from the ancient Greeks to the pre- and post-modern Europeans, romantic Emersonians, tortured Russians or enlightened Confucians), one common trait of wisdom through time, culture and language is the ability to admit, and then learn from, error–as any man’s journey is one riddled with countless opportunities for teachable error.

Yet when it comes to public mea-culpas and the grand teaching moments of “I was wrong,” it seems our central and commercial bankers have failed miserably.

Infallible Bankers or Exceptional Finger Pointers?

Not only have bank leaders taken little to no responsibility for (or contrition of) their many financial, political and moral sins (think billion-dollar bailouts, a 0 in 10 record for recession forecasting or the creation of the greatest and levered asset bubble and wealth transfer in history), they have a remarkable talent for blaming anyone (Putin et al) or anything (COVID or coal) but themselves or the derivative toxins and unpayable debt piles they alone created…

In summary, it seems we are living in era of great change, great turmoil and great risk, yet also one of very little accountability, transparency and hence: wisdom.

Sustained Levels of Mediocrity

Instead, from DC to Wall Street, Tokyo to Brussels, Canada to Australia, and Brainard to Draghi, the world is increasingly led by figures (left, right and center) who are capable, at best, of little more than a sustained level of mediocrity and an over-paid repertoire of canned phrases and prompt-read platitudes rather than actual, economic savvy, candor or personal wisdom.

Such high-office mediocrity and lack of wisdom, of course, spills well beyond the centers of political power and office; in fact, it thrives with equal force in the private sector and public markets, as any who have tracked and pre and post Enron world will and do know…

Modern Dystopia: High Tech, Low Wisdom

As to more recent scandals and headlines related to the staggering blowout at FTX, enough has already been written/said of its impressive mix of fraud, leverage and corrupt (paid-for) politics for me to add more mathematical detail here.

Unfortunately, FTX’s scandalous scheming with investor money (ala Madoff) and bank leverage (ala Bear Sterns) is nothing new.

The broader sins of fractional reserve banking, historical debt levels and trillions in mouse-click monetary policies have effectively murdered honest capitalism within a rigged-to-fail financial system whose destructive consequences far outpace the FTX headlines of late.

I am thinking of 1) the leverage-poisoned MERK, compliments of Leo Melamed and Alan Greenspan in the 80’s, 2) a completely fixed paper gold pricing exchange, 3) the post Glass-Steagall (nod to Larry Summers) banking era which turned depositor accounts into levered ammunition for banks speculating like hedge-funds or 4) the open fraud (legalized counterfeiting) which daily passes for monetary policy at a central bank near you.

As Henry Ford warned, if more folks actually understood banking practices and the false idols hiding behind expert masks, the net result would be chaos.

Patterns of Fake Genuis

As for the recent chaos in the C-suites of our tech leadership, an equally clear, and all too familiar pattern of under-30 millionaire/billionaires (from WeWork’s Adam Newman to Facebook’s Mark Zuckerberg or FTX’s Sam Bankman-Fried) is the now obvious as well as inverse correlation between so-called “technological genius” and basic human wisdom.

In short, we would be right to ask if our modern technological progress and high-office prestige has far outpaced our human wisdom.

All Piano, No Music

As Antoine de St. Exupery warned (as far back as 1944), the world is capable of producing 1000 pianos per hour but unable to produce enough worthy pianists to play them.

In short, the speed of our so-called “progress” (from computer chips, social media, Fauci-science and digital money to de-regulated margin accounts) seems to have tragically outpaced the philosophical measure of our wisdom.

Despite some wonderful exceptions from Wall St to Pal Aalto, many of our best and brightest are driven by the timeless and “human all too human” impulses of greed, FOMO, and telegraphed/photographed virtue-signaling rather anonymous good work or honest commerce.

Sam Bankman-Fried (SBF), for example, was a master at appearing like a Robin Hood despite having the instincts of a robber baron.

Self-Service Masquerading as Virtue Signaling

The end result is a literal “selfie culture” which, fractured by identity politics, victim narratives and resentment on the fly, has morphed into a priority of the “I” over the good of (or genuine concern for) the many.

This trend is equally true of our public and private markets.

Moral, legal and economic laws have become more and more, shall we say… “elastic” as the sins and consequences (from currency debasement to anti-trust/monopolies and cancerous debt levels) of one generation are happily billed to the next.

Such patterns of ignored decencies/rules in which a Madoff sits comically on the NASDAQ board or an SBF ironically teaches a paid-for Congress about crypto safety, are common.

Equally disconcerting is a celebrity-mad population who trusts its mandate science to Spike Lee or its crypto advice from Matt Damon. If one is financially “successful” it is assumed he is wise; that is a dangerous assumption…

Meanwhile, headline spin and financial lobbying has replaced the ideal of genuine capitalism with a kind of neo feudalism in which figures like Bezos (with easier access to capital after years of violating anti-trust principles and CEO-to-employee salary ratios) have become part of a new aristocracy rather than exemplars of democratic meritocracy or fair-priced capitalism.

Back to the Markets: What FTX Portends

Given the foregoing cynicism/realism emanating from our modern markets, there is still much we can glean about the direction of, and risks to, our current markets.

For example, it will come as no surprise that the FTX fiasco has already been spun into a positive rather than negative narrative for the BTC camp.

As to cryptos in general and BTC in particular, I have already written and spoken at length of my views.

Toward this end, and to the understandable chagrin of the crypto camp, I (rightly or wrongly) view BTC more as a speculative growth/tech stock than as a viable alternative currency or long-term store of value.

Nothing about the recent FTX blowup has altered this view.

Again (and I could very easily be wrong), I don’t see BTC as money, a view which seems to be shared by a large number of emerging markets and central banks who are loading up on record amounts of physical gold rather than invisible cryptos.

Just saying…

And to re-heat a tired yet accurate quote by JP Morgan, I (we) still fully embrace the “barbarous” notion that gold is money, the rest is credit/debt.

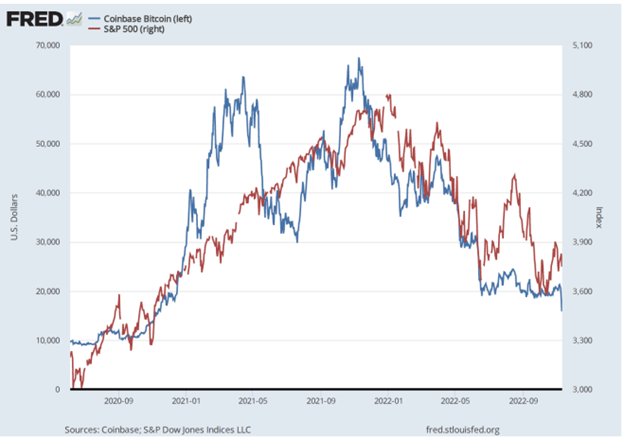

BTC As Market Indicator

Regardless, however, of one’s views, biases or take on cryptos, Bitcoin’s pricing still has immense relevance to modern markets, including gold markets.

In terms of US stocks, for example, BTC has been an exceptional leading liquidity metric outside of the derivatives markets or Fed-manipulated bond markets.

In other words, stock, bond and even property markets tend to behave and move a lot like BTC behaved just a short period before.

In short, and regardless of one’s pro or con take on BTC, as an asset class and market indicator, this “coin” still clearly matters.

BTC: Local to Systemic Sickness?

And perhaps more to the point: As a tanking asset class with trillions in losses, BTC, like any bleeding asset in a grotesquely over-levered system, really matters.

Why?

Because BTC’s local sickness can easily become systemic.

The risk of this systemic spread, for example, will increase if there are less and less “dip buyers” for BTC, especially when inflation factors should otherwise favor the asset.

The potential for such a low-bid trend for BTC (based on FTX-like fears of broken exchanges and hence broken TRUST) could easily and accurately portend a low-bid contagion effect in the broader equity markets in general and the already bleeding tech sector in particular.

That said, an increasingly cynical as well inflation-ravaged generation of jaded outsiders are feeling increasingly cornered, which means they have less and less to lose.

This desperation may lead to more distrust in the system and hence more buying of BTC as a modern 9and fully understandable) middle-finger to that system.

For now, let’s wait and see what the post-FTX trend will be for BTC; I personally foresee an eventual (though not immediate) rip in its price.

The Bond Market Matters

Equally, if not more importantly, the current and declining liquidity canary in the BTC coalmine, as stated above, has been a leading indicator for equal liquidity risks (and hence declining behavior) in the bond and property sectors as well.

With US debt to GDP levels above the precarious 120% level and US deficits spiking, Uncle Sam is going to need to need to find liquidity somewhere to cover its bond obligations.

One can not emphasize enough how much this bond market matters.

Hawk to Dove—A Brewing & Golden Tailwind

And as I’ve been arguing ever since Powell went Hawkish, it is my conviction that such liquidity will ultimately (and only) be found when that hawk becomes a doveand the Fed reverts to the desperate mean of relying (tragically/addictively) on the only consistent income source it has, namely: A mouse clicker at the Eccles Building.

Such mouse-clicked “magical money,” of course, has immediate as well as immense inflationary and currency (USD) ramifications, which means the pivot will have immediate as well as immense ramifications on the price of gold in USD.

Expanding Deficits: More Tailwinds for Gold

Equally bullish for gold yet equally tragic for the US are the recent (and doubling) deficit forecasts coming out of DC.

That is, the US Treasury has already announced its borrowing amounts for the next 6 months ($1.3T), which is an indirect way of revealing a federal deficit doubling (on an annualized basis) for the same period.

For me, the implications of such added debt levels are mathematicalrather than just cynical or political.

That is, Uncle Sam simply can’t afford to pay ever-increasing debt piles of this embarrassing magnitude unless interest rates are decidedly negative rather than painfully positive.

Stated even more plainly, all debtors love (and hence eventually engineer) inflation rates to be higher than interest rates.

And since Uncle Sam (and the Fed) are not only powerfully distorted, but powerfully in control, one can easily predict what any all-powerful but debt-cornered policy hack would and will do as we stumble into 2023, namely: Seek more inflation and lower rates while simultaneously under-reporting inflation by at least 50%.

How’s that for trust building, wisdom and central bank accountability?

In the end, as wisdom dies from above, and hence trust rots from within as inflation rises and real rates go increasingly negative, Gold will do what it always does in such man-made settings—namely surge north as the USD, now artificially supported by rising rates, sinks dramatically south once those rates go dovishly in the same direction.

Defaulting Bonds, Tanking Treasuries, Rising Gold

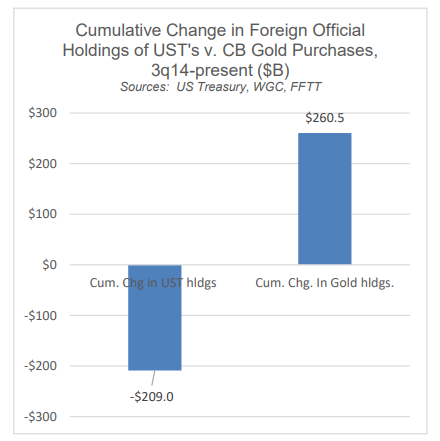

Of course, as soon as the market collectively realizes that negative yielding bonds (the historical instrument of all debt-soaked and hence failing regimes) are effectively defaulting bonds, investor interest in US Treasuries will fall while interest in gold will rise, as is already the case:

Cynics, of course, might say that $260B in gold is a trifle amount compared to other asset classes.

Fair point.

Gold: Repressed Today, Fairly Priced Tomorrow

But here’s the rub: The central banks are (and have been) intentionally suppressing paper gold in order to take more physical delivery today before they inevitably reprice gold higher tomorrow to recapitalize their horrific balance sheets.

This trend is easy to see simply because the rigged game played by the broken actors described above is as easy to predict as their lack of wisdom is easy to measure.

As Egon and I have often remarked, the central banks are unwittingly gold’s best friend, for the bankers’ lack of wisdom and abundance of self-interest in otherwise desperate times makes them easy to track.

Or stated more simply: As the system gets more corrupt (as it always does when backed against a debt wall and a moral vacuum), gold gets more loyal.

About Matthew Piepenburg

Matthew Piepenburg

Partner

VON GREYERZ AG

Zurich, Switzerland

Phone: +41 44 213 62 45

VON GREYERZ AG global client base strategically stores an important part of their wealth in Switzerland in physical gold and silver outside the banking system. VON GREYERZ is pleased to deliver a unique and exceptional service to our highly esteemed wealth preservation clientele in over 90 countries.

VONGREYERZ.gold

Contact Us

Articles may be republished if full credits are given with a link to VONGREYERZ.GOLD