MAKING SENSE OF COMEX INSANITY

We certainly live in interesting times. Yet be you bear or bull, left or right, optimist, cynic or pessimist, one would be hard pressed to pretend that anything is, well, normal.

The Controversially Insane

Many are questioning why a virus with a death rate of less than .4% has shut down the global economy for a year and counting.

Despite extremely legitimate moments of silence for those who died with (or of) COVID, others are questioning policy makers who ignored protecting the most at risk profiles while remaining largely silent for the self-inflicted death for the rest of Main Street economies shut-down across the world.

As millions of Americans await a check from Uncle Sam to the tune of $1400, some are wondering why SEC-sanctioned liars and tweet-happy front runners like Elon Musk and other C-suite tech giants are amassing fortunes.

Incidentally, that $1400 check is ¼ the cost of the dress worn by Meghan Markle in her recent attempt to convince Oprah and the rest of the world to sympathize with her unique struggles while more than 50% of U.S. children are living in welfare-assisted homes.

Again, is this normal?

It certainly is “interesting.”

Central banks, printing trillions per year to buy otherwise unwanted sovereign IOU’s are keeping bonds so over-supported and over-valued that the bulk of the nominal and real yields on government debt are negative—something never seen in 5000 years of recorded market history.

Meanwhile, more than 20% of US corporate bonds are literally zombies—i.e. dead men walking on new debt to pay interest on old debt with no chance of ever repaying principal as the vast majority of US corporate credits (well over 65%) are either levered loans or just one eyelash above junk status.

Slowly rising yields, still openly repressed by central bank intervention, are now being telegraphed to the world as a sign of “economic growth” by Wall Street Pinocchio’s paid to sell hope rather than facts.

At the same time, the media now has the masses convinced that a magical vaccine will solve everything, despite reams of Congressionally-ignored evidence that the specific antibodies within these vaccines attack non-specific antibodies so critical to our immune systems for later illnesses.

In sum, when it comes to central bank accommodation, lock-down measures, yield manipulations or rapid-fire vaccines, it’s at least plausible to wonder if certain policy cures are indeed worse than the global diseases.

That said, I’m certainly no virologist nor an expert on Oprah’s ratings or Elon’s Twitter account, so these are just rants and questions rather than dispositive conclusions, but I am, like so many of you, starting to question the “interesting” world around me.

The Openly Insane

What is less open for debate, however, is the otherwise obvious yet media-ignored disaster otherwise known as the global financial system and the distortions (i.e. lies) that govern them, as evidenced, for example, in the comical CPI measure of inflation.

The very fact that markets reached all-time highs while global economies, GDP’s, employment rates and social conditions reached new lows in the backdrop of a world-wide shutdown, for example, ought to have everyone, including those who know nothing about free market capitalism, scratching their heads.

The Death of Free Markets

This is because there is no such thing as free market capitalism in a world where central banks, eight key commercial banks, and one or two global “institutions” (hint: IMF and World Bank) have effectively and completely taken over, as well as distorted, almost every aspect of the natural supply & demand forces to which we and Adam Smith once swooned.

In case you think such statements are meant to create drama rather then perspective, let’s consider objective facts rather than controversial adjectives and nouns.

It would (and has) taken hundreds of pages to delineate the myriad ways in which fiscal and monetary policy from global law-makers and bankers have hijacked, distorted and then destroyed free market price discovery and natural, true capitalism.

Rather than break such a word count here, let us briefly examine just one corner of this twisted world order and illustrate how rigged the current playing field otherwise known as free-market capitalism and free market “price discovery” truly is.

In short, let’s draw back the curtains to that corrupted stage otherwise known as the COMEX futures market for precious metals and see for ourselves.

Buckle up.

The COMEX Futures Market –Making the Complex (and Rotten) Simple

For many, the COMEX future’s market is a very scary, mysterious and almost foreign universe.

And yes, it’s also complex in all its trading paper, players, strategies and layers—too complex, indeed, to fully unpack here.

At its most basic level, however, the COMEX futures market is a place where paper contracts representing actual hard assets (from soybeans to gold) are traded.

In a normal world, for example, a contract to buy a bundle of grain at a fixed price can be traded on the COMEX market to ensure fixed (i.e. contractual) pricing against market price swings.

Once such a contract (be it for grains, metal, or pork-bellies) nears its expiration date, the holder of the contract can either take delivery of the contracted-for commodity, or rollover (i.e. extend) that contract for a longer period, thereby delaying actual delivery.

Pretty simple, right?

From Simple to Manipulated

Such simplicity, however, gets more complex when that same exchange (thanks to creative young bucks like Leo Melamed and Alan Greenspan) allows those simple contracts to be traded with leverage, anywhere from 100:1 to even 300:1.

In short: Far more contracts than the actual assets within them.

The simplicity gets even more complicated when participants are allowed to go long AND short those contracts via the use of admittedly complex derivative instruments.

Finally, the simplicity gets fully distorted, and complex, when a small minority of extremely deep-pocked participants control the vast majority of the buying and selling of those contracts, and hence their pricing.

In short, the COMEX futures market is not a simple place for the buying and selling of paper contracts, but rather a highly corrupted place for the manipulation, leverage and manipulation of those paper contracts and hence the pricing of the assets they represent.

Worthless Paper…

But paper, as we know, is ordinarily just a flimsy thing. Paper is also where we get to hold and touch fiat currencies, which like most paper products, are not terribly valuable. As Voltaire famously said: “All paper money eventually returns to its intrinsic value—zero.”

Yet this ever-weakening paper money, ever since Nixon robbed it of its gold-backing in 1971, is what makes the ever-mad financial world go ever-round in this new, ever-“interesting” era.

Central banks, and broke nations, therefore need to make otherwise weak paper appear valuable, and will do all kinds of complex market gymnastics to keep the illusion that paper is actual wealth.

Toward this end, it is therefore very, very, very important for those powerful players to make true stores of wealth—i.e. gold and silver—look far less valuable than what the natural market would otherwise dictate.

In short, key market manipulators (described below) like to use paper products to make gold and silver products look less sexy, for if gold and silver where to be priced according to genuine supply and demand forces, then the entire (and embarrassingly broken) paper scheme of global fiat currencies and markets would fall like a house of cheap (paper) cards.

Hard to believe?

Let me show you.

Gold & Silver’s Fictional “Paper” Price

Take my two favorite, misunderstood, yet historically-confirmed stores of genuine rather than paper (or even crypto) value: Gold & silver.

Popular demand for these assets is in fact massive, which means their price power should be openly and equally so.

After all, true, free-market capitalism rewards those assets which enjoy high demand but relatively low supply, right? That, after all, is Econ 101.

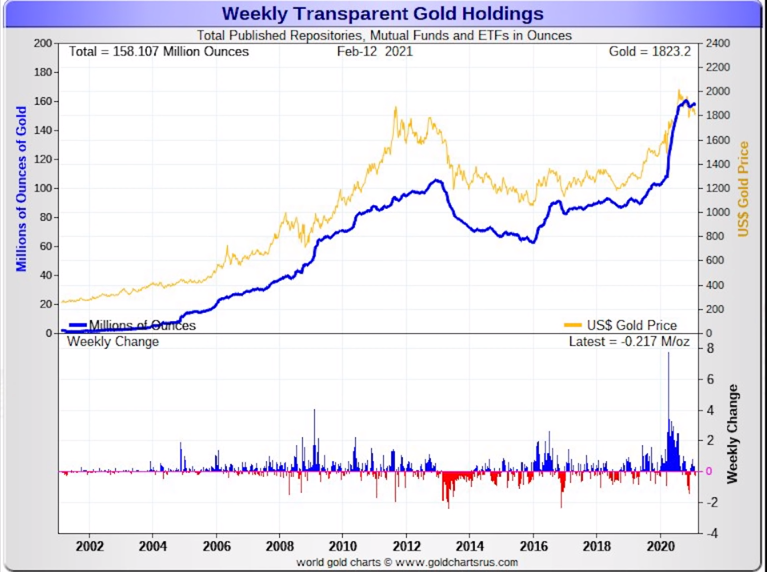

Let’s look, then, at the example of rising demand for silver in 2021 as measured by ETF flows:

And let’s do the same for flows into gold ETF’s, just to make the natural demand visually clear:

With such rising demand for ETF gold and silver (allegedly backed by actual physical gold and silver held by the custodians of these funds), shouldn’t gold and silver prices therefore be skyrocketing in the paper markets that represent them?

Well, as alluded above, paper is a funny thing, and for the policy makers (i.e. central banks, major commercial –or “bullion”—banks and all dollar dependent politicians) who are deeply threatened by rising gold and silver prices, paper can be easily manipulated, which means so can the price of gold and silver.

How the Hateful-8 Kill Free Market Price Discovery

And to make this obvious, objective and undeniable as opposed to just theoretical or dramatic, let’s see how the big players, rather than the natural supply and demand forces, artificially, legally and yet dishonestly fix the gold and silver prices, and thus mock any vestige of respect for that bygone ghost otherwise known as free market price action.

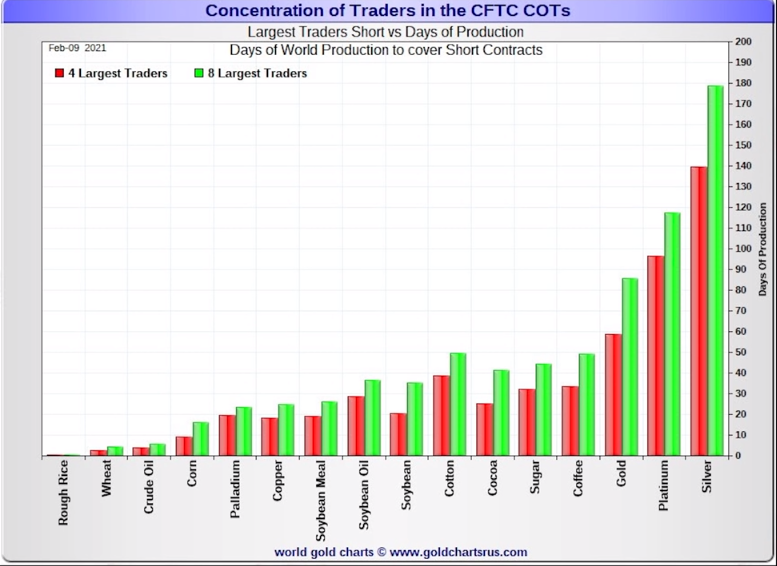

Specifically, let’s see how just eight major commercial banks are able to overpower the natural price power of thousands of other contract buyers on the COMEX futures market to artificially suppress the natural pricing of these two precious metals.

Believe it or not, nearly every contract (and I’m talking thousands of them) for gold and silver in the COMEX futures market trade net long—meaning they are buyers. That should make their prices quite high.

Yet all it takes to defeat the demand power (and rising price) of those contracts and metals is for just four to eight of the largest traders (mainly bullion banks) in the futures market to perpetually short (i.e. bet against) those other contracts to keep their prices suppressed.

Hard to believe? Then see for yourself:

In sum, what we see in the COMEX futures markets are eight players essentially betting against the rest of the world in order to control the price of precious metals.

Alas, this tiny handful of eight (the “Hateful-8”?) are and were short more than 50% of the entire futures market, and by going this deep and this short they literally (and artificially) control the paper price of precious metals, for without such intervention, the price of gold and silver would literally be skyrocketing.

Do you now see how terrified the big boys are of rising gold and silver? Recently, they were 112% short silver to the tune of over 412 million ounces.

Of course, we already know what they are afraid of: Rising gold and silver would be the ultimate and absolute confirmation of the otherwise open failure of unlimited money printing and fiat currencies in a post-Nixon world.

How Long Can Natural Price Forces be Repressed?

But the next question is equally obvious: How long can this scam/manipulation continue?

That is, if four to eight big boys are colluding to the tunes of billions and billions and billions of dollars in short contracts on the COMEX, how long can this game continue without a wrench in their plans?

Key to the survival of this open scam and price suppression (in play since 1973) is to keep the short contracts on these precious metals perpetually rolling over rather than expiring, for if the contracts were to ever expire, an actual physical delivery of the underlying metals would be legally required.

But that would immediately spell party over for the Hateful-8 as well as the COMEX itself.

That’s because these same big boys would default on actual delivery for the simple reason that they don’t actually own enough gold and silver to honor their levered contracts. Not even close.

That is also why the current cost spread on the COMEX for rolling over (rather than delivering) these contracts in gold and silver are so cheap—in fact, almost free.

In simple terms, these market manipulators (or the COMEX itself) wouldn’t survive without such manipulation and perpetual contract roll-overs.

Alternatively, if they couldn’t make actual delivery of the metals (and they can’t), the Hateful-8 would be forced to cover their own COMEX shorts and go net long once gold and silver prices climbed (i.e. “squeezed” them) beyond their control.

This short-covering would cause the price of precious metals to skyrocket.

But even the big boy’s pockets aren’t deep enough to ever afford going net long to cover their own sins and shorts—this would require trillions, not billions.

Not even a bailout from Exchange Stabilization Fund could help these TBTF (Too Big to Fail) bullion banks at that point.

In short, this small handful of big boys shorting the gold and silver contracts on the COMEX are playing with gasoline and matches.

All of the big boys, that is, but one…

Enter JP Morgan—No Honor Among Thieves

When JP Morgan inherited the post-08 books of that other headline failure, Bear Sterns, this included 30,000 to 40,000 short contract positions in gold and silver.

For all the reasons (and risks) stated above, JP Morgan knew it was dangerous to be net short gold and silver (because as metal custodians for other funds, Morgan knows better than anyone that there simply isn’t enough physical gold and silver to meet the delivery demands of the grossly levered contracts traded on that over-levered COMEX).

Stated otherwise, Morgan needed to dump (and cover) those shorts (by going long) at just the right moment, i.e. when prices were low.

Thus, after spoofing the market in early 2020, Morgan artificially manipulated the prices down before going net long to cover their shorts last March.

As of now, JP Morgan has closed its short positions and is market neutral rather than net short gold and silver.

In fact, they are stacking their physical gold and silver bars in London warehouses as I type this, controlling over 1B ounces of Silver and over 25M ounces of gold.

Why?

Very simple, they plan to front run the inevitable gold and silver bull market of which we’ve been writing for years.

And as for the COMEX futures market in paper gold? Well, its days are numbered and the fallout from its failure will be more than “interesting,” but nothing less than a disaster.

About Matthew Piepenburg

Matthew Piepenburg

Partner

VON GREYERZ AG

Zurich, Switzerland

Phone: +41 44 213 62 45

VON GREYERZ AG global client base strategically stores an important part of their wealth in Switzerland in physical gold and silver outside the banking system. VON GREYERZ is pleased to deliver a unique and exceptional service to our highly esteemed wealth preservation clientele in over 90 countries.

VONGREYERZ.gold

Contact Us

Articles may be republished if full credits are given with a link to VONGREYERZ.GOLD