Liquidity Crisis: Wells Fargo & Repo Markets Sound Alarms

Every financial crisis ultimately boils down to a liquidity crisis, namely: Not enough fiat dollars to keep the financial wheels sufficiently greased.

Below, we look at two warning signs from Wells Fargo (NYSE: WFC) and the reverse repo market which warn of precisely that: a liquidity crisis.

From Debt Binge to Credit Crunch: A Chronicle of Excess

In a world in which consumers, corporations, and sovereigns have falsely confused debt-based growth as actual growth, a liquidity crisis is not a theoretical debate, but a mathematical certainty.

For years, self-serving politico’s, central bankers, Wall Street sell-siders, and a woefully unsophisticated cadre of main stream financial “journalists” have endeavored to downplay this rise-and-“pop” certainty by deliberately ignoring the $280T debt elephant in the global living room.

Of course, that debt, for years, has been “monetized” by increasingly debased currencies and rising money supplies created literally from central bank mouse-clicks rather than productivity, as evidenced by the embarrassing fact that global GDP is less than 1/3 of the global debt.

Needless to say, money (i.e., “liquidity”) created out of thin air, and then justified with even thinner (yet comfortably titled) policies like Modern Monetary Theory has its temporary charms.

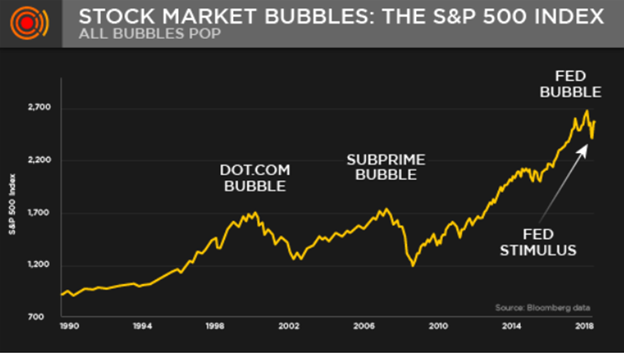

It Was the Best of Times…

Risk assets—namely stocks, bonds and real estate– love easy money, be it printed out of nowhere or lent at rock-bottom (and artificially repressed) interest rates.

For years, the big boy corporations on the major exchanges have been borrowing trillions per annum to buy their own stocks and/or pay dividends, which naturally makes stocks go up rather than down.

In short, when money is flowing, risk assets rise on a rising tide, even if that tide is artificial, “printed,” pretended or extended (yet ultimately a source of financial drowning).

It Was the Worst of Times…

In the meantime, those good-time rising tides benefited an increasingly smaller segment of the social-contract, which explains why historical levels of wealth inequality have led to equally inevitable (and rising) tides of undeniable social unrest.

Economics Matters—History Turns on “Dimes”

Despite the fact that such appalling debt dangers existed long before COVID, the “experts” now conveniently blame our fractured societies (and growing debt burdens) on a pandemic while distracting the masses with a media that is far more obsessed with transgender bathroom rights, racial headlines, the latest COVID variant and the sorrows of Prince Harry than they are with the fact that our financial system is rotting right below our feet.

This financial rotting has real consequences for society not just market analysis.

After all, social unrest always follows a financial crisis (and inequality), despite the perpetrators’ best efforts to shield themselves from blame.

Transparency Matters—But It’s Gone

Of course, as every magician (or covert operative) knows, the best way to pull off a trick is to distract the audience from the real slight-of-hand, allowing the hocus-pocus of a self-inflicted financial disaster to hide from immediate view via lies of omission rather than the courage of accountability.

Perhaps the greatest of these lies was the daily-telegraphed message that extreme money printing and debt expansion was only “temporary” and “under control” as opposed to a full-out addiction which always ends in a fatal financial overdose.

For years, we’ve been told that $28T in global central bank money printing was not inflationary, and finally, when that inflation did rear its head, we’re now being told it’s only “transitory.”

Most, however, know better.

Swapping One Addiction for Another

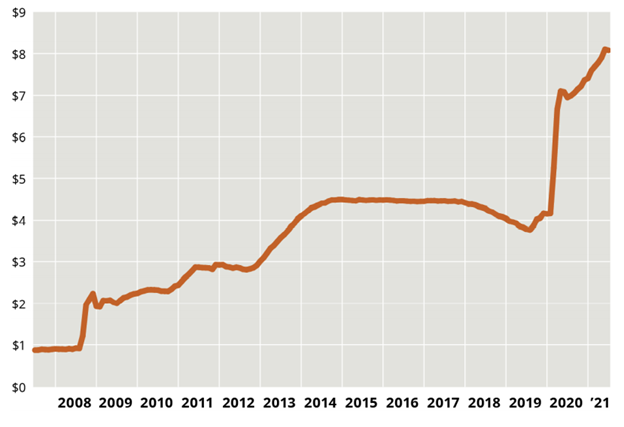

Frankly, even the central bankers themselves (from Yellen to Powell) are finding it harder to whistle past (or double-speak through) the graveyard of debt and dying dollars which they alone created through appalling balance sheet expansion (addiction) like this:

There was even “frightening” talk of central bank “tapering,” as these bankers ran out of excuses, credibility and options to justify more money printing.

But if one addiction loses its source, there’s always a new drug pusher (and “liquidity” source) to step up, and in a global financial system marked by an addiction to easy money (rather than needed austerity or actual productivity), the newest addiction to replace Fed money printing is now government deficit spending.

That is, extreme fiscal policy is gradually replacing (or at least joining) extreme monetary policy (and governmental guarantees of commercial bank lending) to keep dollars flowing and hence a slowly tanking financial system momentarily “greased” with yet another deadly liquidity “fix.”

Just like we saw QE 1 fatally morph from QE2-4 into “Unlimited QE,” we shall soon see fiscal policy 1 morph into unlimited “fiscal policy” at a nation-state near you; beginning, of course, with Biden et al.

But as we’ve said many times elsewhere, addiction—be it to monetary stimulus or fiscal stimulus—always ends the same way: One either quits or dies.

Again, even the bankers and a small handful of brain-celled politicos know this, which is why we are starting to see signs of a genuine hangover (i.e., liquidity crisis) in our artificial yet liquidity-addicted financial system.

As for these flashing warning signs, let’s just consider two recent tremors percolating below our feet: 1) Wells Fargo and 2) the reverse repo market.

1. Wells Fargo Welches in Panic

We’ve given many prior warnings regarding the objective evidence of banking risk in the global financial system, and despite Basel III’s virtue signaling, we also warned that those risks were anything but “transitory.”

In fact, even the big boys in the big banks are getting nervous—as well as ahead of—the financial crisis they see coming after years of benefiting almost exclusively from a credit binge which they themselves engineered.

In short, the liquidity they once relied upon is drying up.

Thinking always of themselves first and clients second, Wells Fargo just announced that they are permanently suspending/closing all personal lines of credit (from $3k to $300K) in the coming weeks.

Yes. That’s kind of a big deal…

Wells Fargo is effectively confessing that they are worried (seriously worried) about inevitable credit/loan defaults on their consumer credit lines for which they charge interest at anywhere from 9% to 21% (and who thought usury was dead?).

Why the sudden change of heart at that oh-so generous bank?

Because Wells Fargo is worried about a crisis ahead—namely a liquidity crisis.

Nor is Wells Fargo alone. Many insider businesses (i.e., publicly-traded fat cats) who benefit from the best loan terms and unfair capital access are taking on less debt.

Why?

Because their massive debt exposures have just gotten too big to ignore, and they have no choice but to borrow less rather than more.

Of course, less borrowing means less lending, and less lending means tightened credit, and tightened credit means a credit crunch (i.e., liquidity crisis), and a credit crunch in a world/market addicted to credit (i.e., debt) means ”uh-oh” for risk assets like stocks, bonds and real estate.

Meanwhile, as Wells Fargo hunkers down for the pain ahead, JP Morgan, one of the smartest insiders in the entire (rigged) banking system, is beginning to carefully hoard and stockpile cash ($500B) and moving more to the safety of short-term bonds.

Why?

Well, they’d like to have some dry-powder when risk assets tank and rates rise, for the best time to buy is when there’s blood in the streets; and the best time to lend is when inflation and rates are rising, not falling.

But more to the point, JP Morgan (like Wells Fargo) sees a liquidity crisis on the horizon…

But what suddenly tipped them off?

Let’s talk about the Reverse Repo market…

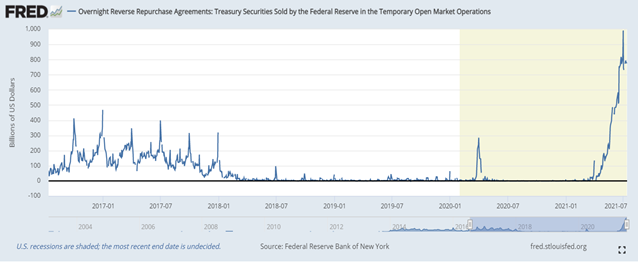

2. The Reverse Repo Market—Banks Losing Trust in Each Other

Signals from that esoteric (and hence media-misunderstood) corner of the banking system known as the repo market have been making neon-flashing warning signs.

Traditionally, the reverse repo market is where banks went to borrow from banks, typically offering collateral (US Treasuries) for some short-term liquidity—i.e., money at low rates.

But in September of 2019, those rates spiked dramatically for the simple reason that banks began distrusting each other’s credit risk and collateral. That’s a bad sign.

What is happening now is that the Fed, rather than the commercial banks, are taking a much greater role in back-stopping this increasingly fractured intra-bank repo (credit) market.

And unlike retail clients paying double-digit rates for credit lines, the Fed has lifted the interest (IER) they pay to banks (no shocker there) as banks are parking more money at the Fed where they are exchanging cash for Treasuries in a now unignorable flight to safety.

As a result, the repo market has skyrocketed as banks are parking nearly $1T per day at the Fed, which is 3X the normal operational amount.

This is a screaming sign of counter-party risk among the banks themselves, whose last hope is the Fed, not each other.

And why are the too-big-to-fail banks looking for low-rate handouts and T-bills from these grotesquely bloated (and Fed-supported) repo markets?

Because they see a crash coming and are bracing for the transition from credit addiction to financial crisis—i.e., less “liquidity” to grease the broken wheels of an overheated credit system.

Risk Assets Facing Real Risk

What does this mean for the great inflation-deflation debate?

Well, a liquidity crisis is never good for risk assets like stocks, which will see a price decline and hence “deflation;” but don’t confuse that with the real-world notion of inflation—namely rising prices for the things most mortals need to live.

As more banks are swapping T-bills as collateral from the Fed rather than each other for cash, this means massive amounts of money (“liquidity”) is coming out of the system.

The money markets are moving alarming amounts of dollars to the Fed, which means bank reserve accounts are moving from the banks to the Fed itself; this, in turn, means less bank reserves and hence less bank lending—i.e., a credit tightening rather than credit binging.

Such reduced “liquidity,” as mentioned above, is a very bad omen for risk asset markets.

Gold’s Direction and Meaning

As for gold, when markets tank, gold can follow, but with far less depth and speed. Many tapped out investors are forced to sell safer precious metals to cover risk asset losses, and the pinch to gold is temporary yet real when markets decline.

But as deflation hits the exchange prices, inflation in the price of everything else continues its slow climb north, which gold eventually and consistently follows.

In short, in a financial crisis, gold ultimately shines brightest as its inherent value is inherently superior to tanking currencies, stocks and other risk assets.

As liquidity dries up in a financial crisis, the trend will be disinflationary, but please remember that disinflation is not deflation; it’s a just slower rate of inflation.

Between 1972 and 74, for example, when risk assets fell in nominal terms by 50% (“deflationary”), consumer prices had risen by 10% (“inflationary”).

Informed gold investors have known for years that the banking system is deeply flawed and that at some point a monetary collapse far greater than the GFC of 2008 is inevitable, which, by the way, does not mean imminent.

Preparation is Wiser than Timing

But for gold investors (rather than traders/speculators), timing is not the motive, preparation is.

When the monetary system implodes under its own excess (for which the foregoing warning signs from Wells Fargo to the repo markets are merely the first tremors), gold will be far kinder than currencies and traditional (and now historically bloated) risk assets.

The obvious question today is how much deficit spending (inflationary, by the way) will governments desperately commit to in order to fill the gap of dollars now coming out of the commercial banking system?

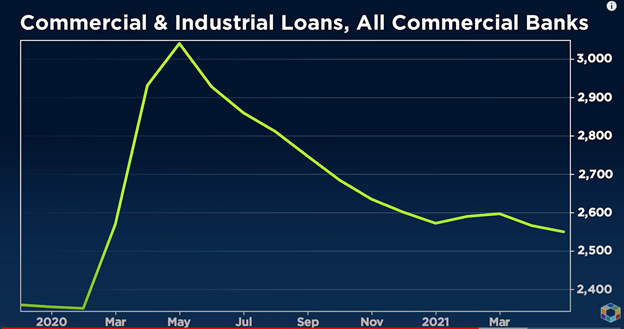

Again, we already know that commercial bank lending (and credit availability) is down:

Meanwhile, M2 money supply, compliments of deficit spending, was up 25% in 2020 as governments monetized their debt with, alas, more debt…

As hinted above, are we transitioning from unlimited QE to unlimited deficit spending to “solve” liquidity crises? Are we coming out of one type of addiction and heading into another?

The sad answer is yes, and again, we all know how addictions end.

In short, what we are seeing in the repo market will not be the cause of the next yet inevitable implosion, but is merely a dying canary in the financial coal mine:

The markets, alas, are handing investors clear warning signals of a liquidity crisis and hence financial crisis.

Who will heed it?

About Matthew Piepenburg

Matthew Piepenburg

Partner

VON GREYERZ AG

Zurich, Switzerland

Phone: +41 44 213 62 45

VON GREYERZ AG global client base strategically stores an important part of their wealth in Switzerland in physical gold and silver outside the banking system. VON GREYERZ is pleased to deliver a unique and exceptional service to our highly esteemed wealth preservation clientele in over 90 countries.

VONGREYERZ.gold

Contact Us

Articles may be republished if full credits are given with a link to VONGREYERZ.GOLD