How an Illiquid Dollar Ruins the World

One can’t emphasize enough how dangerous the current macro setting is in the wake of a deliberately strong and illiquid Dollar.

Biden, of course, says not to worry. We say otherwise.

The Illiquid Dollar: We Showed You So

Over the years, we have written and reported a great deal about the US Dollar and the ironic mix (as well as danger) of its over-creation yet simultaneous lack of liquidity.

This illiquid Dollar, as argued since the first repo crisis of late 2019, combined with a now weaponized US Dollar on the backs of intentionally rising rates by a cornered and Volcker-wannabe Fed, all converge to spell short-term power for the Greenback and longer-term misery for just about every other asset class and economy in a now openly fractured global financial system.

As to the stark reality/risk of this illiquid Dollar, rather than just say “we told you so,” it would be better to “re-show-you so” by making specific reference to a prior report published in December of 2021.

“Dollar Illiquidity—The Ironic Yet Ignored Spark of the Next Crisis”

Since penning that report just over 10 months ago, it’s worth revisiting the implications of an illiquid Dollar and the financial crisis of which we warned then and now find ourselves today.

Why Strong is Weak

It may intuitively feel good to see one’s currency beating all the others and hence puff American chests in a kind of proud admiration for the strongest currency on the block.

Nothing, however, could be further from the truth.

In fact, bragging about a strong US dollar in today’s global neighborhood would be akin to bragging about the healthiest (yet terminally ill) patient in an overcrowded hospice center.

In the end, of course, all fiat currencies revert to the value of their paper, which as Voltaire reminds, is zero.

Or as J.P. Morgan warned years ago, gold is the only money, the rest is debt.

But I digress…

In simplest terms, the strong US Dollar is only relatively strong because every other currency is tanking faster by the second, and this collective spiral is a direct result of the rising US Dollar exporting its inflation to its neighbors and using the bullying power of its world reserve status to weaken, well…the world.

Let’s explain/dig in.

How We Got Here

So, how did we, and the rest of the world’s tanking currencies, get to this embarrassing as well as fatal turning point?

As indicated in the above and other reports, many of the answers lie in the otherwise long and sordid history of central bank fraud, derivatives madness, repo-to-Euro-Dollar obfuscation and just plain ol’ global debt addiction.

Again, and despite trillions in printed/mouse-clicked US Dollars, much of those dollars are all tangled up in the morass (or “milkshake” aka Brent Johnson) of a highly illiquid derivatives market and increasingly illiquid Euro Dollar market.

As we indicated then:

“As Egon von Greyerz and I have said many times, the first overt signs of this danger in the cash-poor (i.e., illiquid) market reared its ‘repo head’ in September of 2019.

This [repo illiquidity] was a neon-flashing signal of long-term trouble ahead. And it had nothing to do with COVID…

Informed investors in the autumn of 2019 had sifted through all the confusing minutia and noise behind the September panic in the otherwise open-fraud scheme that is the U.S. repo market (i.e., private banks levering GSE deposits for guaranteed payouts from Uncle Sam which the U.S. taxpayer funds).

Despite all this noise, and despite being completely ignored (and deliberately downplayed) by an otherwise teenage-savvy mainstream financial media, the entire repo story simply boiled down to this: There weren’t enough available dollars to keep it (and the banks) going.

As a result, the 2019 Fed printed more dollars and immediately dumped a $1.5 trillion rollover facility into the repo pits.

Much, much more followed.”

And boy did it follow.

As recently reported, the Fed has already begun daily rollover liquidity boosts of over $2T in overnight money-market loans to the increasingly illiquid reverse repo swamp.

This is basically “backdoor QE” and serves as just another sign of a USD-addicted system with a never-ending survival thirst for less and less available (and hence more expensive) Dollars.

The Euro Dollar: All Tangled Up in Blues…

The other skunk in the illiquid Dollar woodpile was what we called the “ticking timebomb” of the misleadingly-named ‘Euro Dollar’ market, discussed as follows:

“In fact, Eurodollars have been floating around the world in greater force since the mid-1950s.

But banks (and bankers) always come up with clever ways to make simple [and liquid] Eurodollar transactions complex [and illiquid], as they can easily hide all kinds of greed-satisfying and wealth-generating schemes behind such deliberate Eurodollar complexity.

Specifically, rather than foreign banks using U.S. Dollars overseas (i.e., Eurodollars) to make simple, direct loans to corporate borrowers that can be easily tracked and regulated on the asset and liability columns of offshore bank balance sheets, these same bankers have spent the last few decades getting more and more creative with the Eurodollar – which is to say, more and more toxic and out of control.

Rather than using Eurodollars for direct loans from Bank “X” to Borrower “Y,” offshore financial groups have been busy using these Eurodollars for complex inter-bank borrowing, swap schemes, futures contracts, and levered derivative transactions.

In short, and once again: More derivative-based poison (and extreme banking risk) at work.”

Tangled Dollars = Unusable, Unavailable and Illiquid Dollars

All of this scheming, leverage and swapping boils down to not enough available (i.e., liquid) USDs in a global financial system in which nearly everything—from debt, to oil to derivatives—still has to be paid in increasingly scarce and hence increasingly expensive Dollars.

In addition to this twisted, illiquid and over-levered swamp, the USD rises even higher on Powell rate hikes, all of which combine to force the world’s other currencies to fall.

Why?

Because other countries and central banks have no choice but to swallow/import USD inflation, monetary policy and American political self-interest. Indeed, with financial allies like the U.S., who needs enemies?

Whenever the Fed, for example, prints more of the world reserve currency or raises its interest rate, the rest of the world, which is tied to that currency, is forced to react—i.e., debase, hike and suffer.

We remind that nearly $14T in USD-denominated debt is owed by both emerging market and developed market economies.

As the USD rises in strength on the back of Powell’s impossible Volcker-revival and tangled derivatives, other Dollar-desperate nations from Argentina to Japan find themselves with not enough Greenbacks to pay their debts or settle trades, wires and oil purchases, which thus forces them to print (i.e., debase) more of their local currencies to make USD-denominated payments.

But Japan takes the cake for debasing its own currency all on its own, as no nation has ever loved a money printer and currency-debaser more.

This might explain why Japan is leading the charge in dumping its USTs into the FOREX markets, which only adds more pressure to rising yields and hence rising rates.

Thanks Kuroda—just one more central banker with a mouse-clicker gone mad… Perhaps he’ll be next in line for a Nobel Prize?

But Japan is not alone, as other nations dump the once sacred UST just to keep their currencies afloat…

In short: The strong USD is crippling the word, and that world, as we’ve written numerous times, will be de-dollarizing at a steady and irreversible pace.

No shocker there. At some point, Dollar-indebted nations crack and this twisted global game ends in a credit crisis for the history books.

Other Domino Effects of the Illiquid Dollar

It’s also worth noting that a current and temporarily strong USD effectively knee-caps US exports, as anything that is actually produced in the USA is now far more expensive and hence less competitive abroad, further adding to US trade deficits (not to mention budget deficits) in a world marching toward a financial cliff.

As importantly, as the USD rises in a new environment of rising rates and less liquid dollars, commercial banks in the US (10X levered) and in Europe (20X levered) are exploiting this higher rate policy to de-lever their derivatives exposure, which squeezes an already fatally toxic $2 quadrillion derivatives market, thereby making that ticking timebomb one tick closer to full implosion.

So, no, a strong and illiquid Dollar (world reserve currency) is hardly good for America, the markets or the world. It’s a poison rather than inflation-killer.

How to Fix the Poison?

For those waiting for the Fed to fix the morass we now find ourselves, there is no miracle cure ahead but merely a choice among poisons.

Pick Your Poison

As we’ve warned numerous times, the Fed is caught between a rock and hard-place of its own profoundly inept design.

Should Powell continue his open ruse to allegedly “fight inflation” (which is 50% unreported anyway) using rising rates, then the USD and DXY will keep rising until the global (and debt-driven) economy completely buckles under the expensive weight of unpayable (and dollar-denominated) IOU’s.

Meanwhile, truth-allergic (as well as history-blind and math-inept) politicos will scramble from one government-complicit, PRAVDA-like propaganda platform to the next blaming the looming credit and currency implosion they engineered on a virus, a Vladimir, an oil well or a coal plant.

However, once the US policy makers admit we are in a recession, there will be no way to fight that recession (and the additional $300B in interest expenses owed for every 1% rate hike) without mouse-clicking more USDs and hence forcing the Dollar and rates down rather than up, as no recession in history has ever been defeated with high rates and a roaring currency.

Alas, what is high today will be low tomorrow, and the Fed (controlling a US economy driven by over 91T in combined public, household and corporate debt and a 125% public debt to GDP ratio) will have to choose between saving the bond and stock markets or killing its currency.

That is, the Fed will eventually (don’t ask me when) join the ranks of the UK, Japan and other nations forced to revert/pivot toward their smoking money printers.

Pivot Point?

For now, I still see Mr. Powell heading toward in inevitable (though not imminent) pivot from hawk to dove once credit markets and economies are in even more peril than their press secretaries can deny.

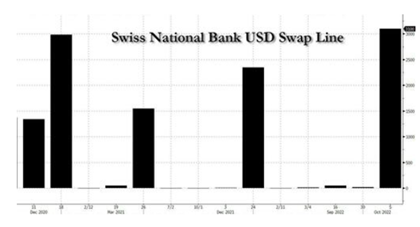

Again, lack of USDs in general (and GDP growth in particular) has already forced the Bank of England to confess its mouse-click/QE addiction, and just recently the Swiss National Bank took a $3.3 billion swap line from the Fed to give its central bank more of those otherwise scarce and expensive USDs.

In the interim, the deliberate efforts by the Fed to engineer a painful recession after they engineered the greatest/grossest asset bubble (and wealth transfer) in history can only be seen as either intentionally evil or unpardonably stupid.

Pick your own verdict. I’d vote for both…

At that pivot point, the Dollar will fall, inflation will rise and stagflation will become the new normal for many years to come, for it’s also worth noting that no modern nation has ever enjoyed a “softish-landing” (quoting Powell) in a recessionary backdrop in which inflation was greater than 5%–and we are already far ahead of that embarrassing and central-bank-created marker.

So, and again, pick your poison: Depression or Inflation? Dead market or dead currency?

A Prize for the Guilty?

As for this current and one-way trip toward global ruin, we can thank Mr. Powell (as well as Bernanke, Greenspan and Mrs. Yellen), none of whom deserve a Nobel Prize, and yet the fact that Bernanke (who gave Japan its QE and Yen-destroying playbook in the late 80’s) now has such a prize is just further proof that this rigged to fail system has completely lost any mooring to sanity, honesty, ethics or economic decency.

Bernanke’s “nobel/noble” policy is the equivalent of buying one’s son a home with an Amex card and then sending the invoice to the grandson.

In short, Bernanke holding a Nobel Prize makes as much sense as Bernie Madoff winning “trader of the year”—but then again, neither ethics nor truth ever stopped Madoff from becoming the NASDAQ’s chairman…

I can’t help but think of La Rochefoucauld’s maxim that “the highest offices are rarely, if ever, served by the highest minds…”

We’ve written too many articles and books to make the Fed’s guilt any more clear today than it already was yesterday.

As for debt-soaked, Frankenstein markets now reeling under rising rates and ever scarcer Dollars, we are nowhere near a bottom and no way out of the woods of ever more volatility to come.

And as for Gold…

As for gold, it rises as fiat currencies tank. For now, the relative and short-lived power of the Fed’s rising rates has been a tailwind to the Greenback and thus a headwind to USD-priced gold.

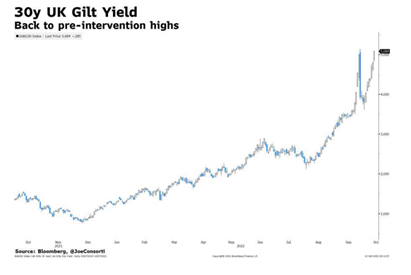

For other countries like Japan or the UK, however, their central banks simply can’t afford the same rate hikes which the Fed’s suicidal reserve eminence allows, so the gold price in the Yen is rising as the purchasing power of the Yen is falling…

…and the same is true for the tanking British pound and rising gold price there:

But like Japan and the Bank of England, every other major central bank from the ECB onward will need to print more local currencies to keep their bonds from tanking and yields from spiking…

Despite its world reserve status, the US Treasury markets face a similar fate and the hard math points toward more inevitable mouse-click QE from the Fed to purchase its own debt.

This makes a tanking USD plain to see coming, and hence gold’s historical USD rise equally plain to predict.

In the interim, the LBMA and COMEX markets are using forward contracts to force gold down in pricing so they can take physical delivery for themselves before the metals skyrocket in USD.

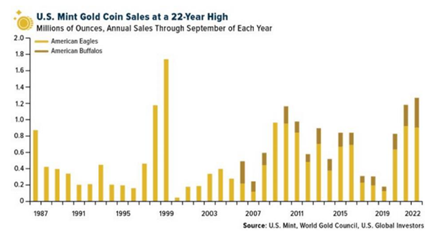

Smart money is catching on, as flows out of paper gold and into physical gold mark a new direction.

For informed investors, now is the value window to do the same with physical gold.

Unfortunately, and as in every asset class and historically-confirmed bubble, the common psychology is to buy high and sell low rather than buy low and sell high.

Informed gold investors, however, are not making this human-all-too-human error as the world tilts each day toward dying paper and rising metals.

Unless, of course, you still think the Fed has your back?

Jeeeessshhhhh.

About Matthew Piepenburg

Matthew Piepenburg

Partner

VON GREYERZ AG

Zurich, Switzerland

Phone: +41 44 213 62 45

VON GREYERZ AG global client base strategically stores an important part of their wealth in Switzerland in physical gold and silver outside the banking system. VON GREYERZ is pleased to deliver a unique and exceptional service to our highly esteemed wealth preservation clientele in over 90 countries.

VONGREYERZ.gold

Contact Us

Articles may be republished if full credits are given with a link to VONGREYERZ.GOLD