Hidden Bankruptcy: The Reality Behind Uncle Sam’s Inflated Bar Tab

Below, we look at The hidden bankruptcy of the US in the wake of even more inflationary forces confirmed by cost-of-living-adjustments, Uncle Sam’s interest expenses, objectively unloved Treasuries and a roaring as well as convenient COVID narrative.

Math vs. Double-Speak

Given the fact that just about everything coming out of the mouths of debt-cornered policy makers requires a lie-detector and “double-speak” translator, we’ve been arguing since the moment the Fed began peddling the “transitory inflation” meme/myth to think differently.

In short: It’s our view that inflation is a snowball growing, not melting.

Toward this end, we’ve written and spoken at length as often as we can as to the many converging forces pointing toward rising inflation—from increased governmental guarantees (controls) over commercial bank loans, commodity super cycles to just plain economic realism, as inflation (and hence currency debasement) is the only tool left (beyond bankruptcy, taxation and “growth”) to service otherwise unsustainable debt levels: A hidden bankruptcy.

But let us not stop there, as other inflationary storm clouds are on the horizon yet ignored (not surprisingly) by an increasingly clueless financial media.

Another Glaringly-Ignored Inflation Indicator—COLA 2.2022

In particular, we are thinking about the U.S. Cost of Living Adjustment (“COLA”) for 2022 which could easily reach 6%, the highest of its kind since 1982.

It would seem that the U.S. Social Security Administration, unlike Powell, is aware of inflation, and therefore preparing (i.e., “adjusting”) for the same.

As the price for entitlement obligations rises, so too will the level of money printing to pay for the same, a veritable vicious circle for rising inflation.

Then there’s simple math.

We’ve talked about the Realpolitik of negative real rates as the final and desperate way for debt-soaked sovereigns to service their debt.

The signs of this are literally everywhere.

If we take, for example, a 1.4% Treasury Yield and subtract a potential 6% COLA increase for Social Security, we get -4.6% real rates, which will be a boon for alternative stores of value like gold and silver or “currencies” like BTC (as well as farmland and high-end real estate, which is continuing to enjoy a debt-jubilee of negative 3% real (i.e., “free” mortgages).

The necessary evil of negative real rates also speaks to the ongoing taper debate…

Giving Clarity to the Taper Debate

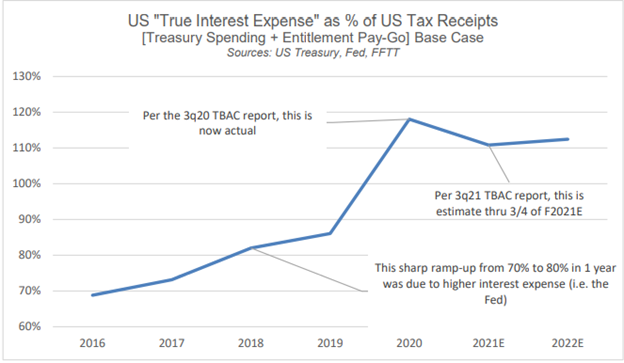

As tweets by twits pour across the electronic universe, it’s often important to notice what is not being “tweeted,” such as the interest expense on Uncle Sam’s national bar tab.

As the financial world hangs on the edge of its seat to see if the Fed will taper its QE (i.e., money printing) program and send bonds (and stocks) to the floor and rates toward the sky, they’ve ignored some basic math and a key chart.

Specifically, we are referring to the chart below representing the true interest expense on the debt bar-tab of a now fully debt-intoxicated Uncle Sam:

With central-bank “accommodated” asset bubbles (from stocks to real estate to art) now at historically unprecedented levels, tax receipts flowing into the U.S. coffers from the ever-growing millionaire-to-billionaire class have been rising.

This may seem good for that punch-drunk Uncle Sam, but what no one is talking about is that despite even those “capital gain” receipts, the interest expense (i.e., “bar tab”) in D.C. is now an astronomical 111% of those same tax receipts.

In other words, U.S. tax income doesn’t come close to even paying interest (let alone that archaic concept known as “principal”) on growing U.S. debt obligations.

Can anyone say, “Uh-oh?”

Given the stark but ignored reality of unpayable U.S. debt, the implications going forward are fairly clear.

First, the Fed will not be able to “taper,” as less QE will mean an even higher interest rate, and thus higher interest expense on debt it still can’t pay at today’s artificially low rates.

Stated otherwise, a “taper” would only add helicopters of gasoline to a debt fire that is already burning the Divided States of America.

Given the dangers of such a taper, it likely won’t happen because it can’t happen, and this means more money printing and hence more negative real rates creating a hidden bankruptcy ahead, a weaker USD and rising precious metal prices, among others.

But What If the Fed Tapers?

Alternatively, should the Fed somehow turn hawkish and taper its QE support in the face of a debt forest fire, Treasuries will sell off dramatically, rates will rise, markets will tank, and the USD will surge—not good for Gold, BTC or just about anything else.

Does it Matter?

But as we’ve also tried to make crystal clear, there is no way the Fed will taper QE liquidity before it sets up a back-channel for even more liquidity from the Standing Repo Facility, Reverse Repo Facility and FIMA swap lines, which are all just “QE” by other names.

In simple speak, therefore, the “taper debate” is no debate, as the Fed has many liquidity tricks up its greasy sleeves.

In addition to liquidity tricks, the Fed has some ugly bonds to buy.

Embarrassing Treasuries

As we’ve said so many times, the biggest issue today is unsustainable and embarrassing debt levels requiring inflation (hidden bankruptcy), compliments of policy makers rather than a viral pandemic narrative out of all proportion to its confused scientific truths.

COVID has been an all-too timely and convenient pretext for blaming global debt ($300T) or U.S. public debt ($28.5T) on a flu rather than a sordid history of grotesque mismanagement from politico’s and bankers that was in play long before the first headlines out of Wuhan.

Furthermore, COVID monetary and fiscal policy measures effectively became a (hidden) pretext for a second market bailout greater in scope (yet better in optics) than the post-Lehman bailout of those otherwise Too Big to Fail banks.

In short, the façade (and branding) of a humanitarian crisis allowed a market-saving liquidity rescue (Bailout 2.0) to an otherwise Dead-on-Arrival bond market in late 2019.

In case this sounds too controversial to consider, please follow the Treasury market rather than our bemused nouns and adjectives, not to mention our total lack of scientific/medical credentials.

Bad IOUs

Just like friends don’t accept IOUs from drug addicts, global investors heading into 2020 stopped buying Uncle Sam’s Treasuries.

In simple-speak, Uncle Sam just seemed too debt-drunk to trust.

As a result, his Treasury bonds, once seen as “safe havens,” were finally seen as “bad jokes”—akin to the paper coming out of equally discredited zip codes like Greece, Italy or Spain.

For this reason, foreigners in a nervous 2020 (unlike a broken 2009) had not only stopped buying U.S. Treasuries, they were selling them.

Yep.

Months ago, smart voices from the Street, including Stan Druckenmiller, were warning about the implications of such a shift in financial consciousness/trust.

Druckenmiller’s Astonishment

Specifically, Druckenmiller spoke of something he’d never seen in over 40 years as a market veteran.

That is, as stocks were tanking in the spring of 2020, he also saw the bond market lose 18 points in one day.

This correlated fall in stocks and bonds was not, as everyone “tweeted,” a reaction to the fiscal profligacy of the CARES Act, but more sadly a very new trend by foreigners to get rid of increasingly discredited U.S. IOUs.

Folks, this is a critical shift.

For over two decades (including during the Great Financial Crisis of 2009), U.S. Treasuries (and the USD) were once seen as “safe” landing places for foreign money rather than a risky bet.

Now, instead of seeing an annual average $500B inflow into U.S. bonds, we are seeing annual outflows of $500B…

When you tack on a $700B current account deficit in D.C. to a net loss of $1 trillion in Treasury support, whose left to “fill the gap” and buy those unwanted IOU’s?

You guessed it: The Fed.

And how will they come up the money to cover these purchases?

You guessed it again: They’ll mouse-click that “money” out of thin air to create a stealthy, hidden bankruptcy.

Needless to say, such realism (i.e., objective math) puts a lot of pressure on the U.S. Dollar as the Fed is forced to create even more money at a record pace to buy otherwise unwanted Treasuries.

But what kept the USD from falling in favor by end of 2020, if no one was buying our bonds but the Fed?

Well, the short answer is that all that foreign money (from sovereign wealth funds and foreign central banks) once ear-marked for our once-credible U.S. Treasury bonds went instead into those massive U.S. digital transformation companies who benefited most from a locked-down new mad world, namely GOOG, ZOOM and MSFT etc.

And how did Druckenmiller describe this shift?

Simple. He called it a “raging new mania.”

From Mania to Desperate

Foreign money once reserved for “safe haven” bonds was (and is) pouring into an already over-sized equity bubble.

By July, the USD had peaked, but after a peak comes, well…a fall for the Greenback—all very good for commodities, real estate, growth tech stocks and, of course, precious metals.

Back to the “What If” of a Naked Taper

But (and this is a very big “but”), what if the Fed were insane enough to taper QE without any back-door liquidity from foreign swap lines and the repo programs?

Again, ugly Treasuries would get even uglier, tank in price, sending rates and the USD higher and gold lower, along with a sharp sell-off in risk assets—i.e., corporate stocks and bonds.

But again, we don’t think this will happen, because as desperate as central bankers are, they are equally predictable.

Predictable Behavior?

That is, they know that such a naked taper (i.e., a taper without a back door repo or swap-induced liquidity) would cause rates to spike, and hence Uncle Sam’s bar-tab to default.

As the Fed’s Vice Chair intimated last year, US Treasuries (Uncle Sam’s bar tab) are simply too big to fail.

This means we can expect more liquidity (QE or repo/swap) and hence more, not less inflation.

The Fed is stuck in a self-inflicted dilemma–between letting inflation rip (to partially service America’s bar tab and “declaring” a hidden bankruptcy) or watching markets sink to the bottom of time.

For now, which choice do you think these banking, pro-market cabal thinkers will make?

The Realpolitik of COVID

Meanwhile, and regardless of one’s views on the vaccine mandates, case fatality rates vs. infection rates, or mask wearing vs. mask annoyance, no one needs our amateur medical advice.

But looking at COVID as a policy tool rather than as controversial health issue, it’s also fairly clear that the powers that be will be milking this fear-porn-to-policy trick for all its worth for as long as its worth.

Why?

Again, COVID is a wonderful narrative to justify more debt and more instant liquidity (i.e., fiat monetary expansion) and hence more inflation to inflate away the debt of debt-drunk nations already fatally in debt pre-COVID.

Rightly or wrongly, there are already scientists out of the UK (namely Oxford vaccine creator Sarah Gilbert) with more IQ-power and credibility than Fauci or Fergusson (admittedly not a high bar), who are already signaling that COVID will resemble little more than a common cold by next year.

This, if true (and no one really knows anyway), would be good for the world—but would the policy makers like this?

A post-COVID normal would be a boon to commerce and economic activity, and hence a boon to the velocity of money, which would kick inflation into ultra-high-gear.

High inflation will mean higher rates, which scare debt-soaked politicians and central bankers, unless inflation rises higher than those rates and negative real yields become the norm, which, again, we think is the realistic (i.e., only option) for these financial magicians running our governments, lives and central banks.

In such a scenario, gold will smile upon the inflation to come.

In short, and however we look at it, inflation is the new norm, and negative real rates are no less so, regardless of how the taper or COVID debate plays out.

As the future unfolds, gold, whose price is waiting for confirmation of such inflation, will only grow stronger as the “transitory” meme gets weaker by the day.

About Matthew Piepenburg

Matthew Piepenburg

Partner

VON GREYERZ AG

Zurich, Switzerland

Phone: +41 44 213 62 45

VON GREYERZ AG global client base strategically stores an important part of their wealth in Switzerland in physical gold and silver outside the banking system. VON GREYERZ is pleased to deliver a unique and exceptional service to our highly esteemed wealth preservation clientele in over 90 countries.

VONGREYERZ.gold

Contact Us

Articles may be republished if full credits are given with a link to VONGREYERZ.GOLD