GOLD – THE ONLY SAFE PLACE

In 2019, the investment world will start to realise that asset markets don’t grow to heaven as stocks, bonds, and property start their long journey down, which will eventually lead to declines of 75% to 95% in real terms. But the major risk is not just investment markets. Just as important is counterparty risk, which too few investors are concerned about.

Anyone who wants to protect their wealth should not be invested in any of the bubble asset markets as I have stated in many articles. But to also avoid counterparty risk is a lot harder.

It is clear that it will be extremely hard to navigate investment markets between Scylla and Charybdis (a rock and a hard place). For the few investors who early on get out of the risky asset markets fuelled by credit expansion and money printing, many other dangers remain.

FEW INVESTORS WORRY ABOUT COUNTERPARTY RISK

Counterparty risk is the risk associated with the other party to a financial transaction not meeting its obligations.

The average investor never worries about counterparty risk. Because “banks are always safe”. And “government bonds is the safest investment you can buy because governments can never default”.

Investors, both private and institutional are today facing the biggest risk in investment history. And virtually no one is aware of this. The 2007- 9 financial crisis and the fall of Lehman alerted investors to the risk of counterparty failing, but since then, 10 years have passed, and all now seems quiet on the financial risk front.

But things are far from quiet below the calm surface. Because once the next crisis starts, not a single bank could ever repay their depositors and no government can repay their debt with real money.

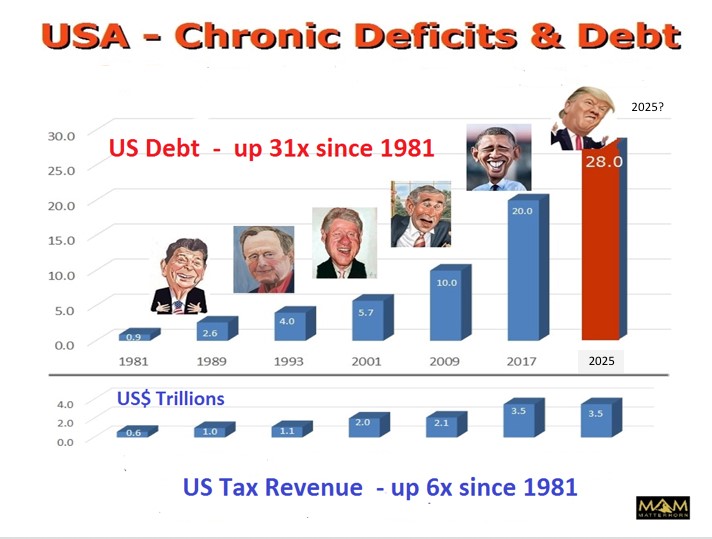

USA – 60 YEARS OF MISMANAGEMENT

Let’s first consider the US government. For 60 years, the US federal debt has increased every year, with two minor exceptions in the 1960s. The Clinton surpluses in the 1990s were fake since debt continued to increase in those years. So here we have a government that couldn’t make ends meet for well over half a century. In 1958, when the deficits first started, the US debt was $280 billion. Today, it is almost $22 trillion. That is a 75x increase. Currently, the US deficits are running at more than $1 trillion per year, and that is very likely to at least double very soon. Since Reagan became President in 1981, US debt has, on average, doubled every 8 years. Trump inherited a $20 trillion debt and if the trend continues, the US debt will be at least $40 trillion in 2028, whoever is President at that time.

DEBT IS A GLOBAL DISEASE

The US is the most indebted country in the world, but debt is a global disease. In China, total debt has grown from $2 trillion in 2000 to $40 trillion today. Japan is just as bad. Japan, with government debt at Yen 1 quadrillion (250% of GDP), would default if rates increased by 0.5%. In Europe, the Mediterranean countries, with Italy the worst, are borrowing heavily, mainly financed by the ECB and German banks. But we only need to look at the balance sheet and share price of Deutsche Bank to realise that the German banking system is on the verge of collapse too. And so it goes on, with most emerging markets heavily indebted and unable to ever repay their debts.

If we then add derivatives at $1.5 quadrillion, we know that global debt and liabilities will implode into a black hole and cause asset prices to collapse.

THERE IS NO SAFE PLACE

Coming back to risk, the few investors who shrewdly exit the overvalued asset markets before they collapse must then consider what to do with their money.

This is where counterparty risk must be carefully evaluated. Sovereign bonds are clearly a very bad risk since neither capital nor interest will be paid in the end.

The banking system is a terrible risk. With leverage of 10 to 50 times, banks will be unable to meet their obligations to depositors and clients. Thus, money will first be bailed in and eventually lost as the bank defaults.

If governments try to save the financial system again, it is likely to fail this time. Global debt has doubled since the last financial crisis started in 2006, and printed money will be worth less than the paper it is printed on or the electricity required to create electronic money. So, any fresh money fabricated by governments will just debase the currency to ZERO.

DON’T HOLD YOUR ALL YOUR ASSETS IN THE BANKING SYSTEM

This leaves a dilemma for investors on what to do with their money. Of course, there are assets that will not lose the majority of their value, such as hard assets and commodities, including food and precious metals mining stocks. The key will be to hold these assets outside the financial system. Otherwise, a systemic failure would either freeze the assets for an extended period at best, or at worst, they would be lost as counterparties fail.

The best wealth preservation asset is precious metals. Gold and silver are both a store of value and a medium of exchange. In virtually all periods of crisis in history, precious metals have always been used as money or barter. There is no other asset which provides instant liquidity at a known market price.

Precious metals must obviously be held in physical form and outside the banking system. Preferably, they should be held in a safe jurisdiction where there is a rule of law and not in the country of residence of the owner. This is to avoid confiscation and the possibility of leaving the country of residence if security, politics or an oppressive regime necessitates a move.

To store gold and silver at home is not a good idea. A criminal can always find it, using violence. If you store any valuables at home, which I would dissuade, it should not be more than you can afford to lose. Much better to store in high-security vaults in countries like Switzerland and Singapore.

ELIMINATE COUNTERPARTIES

It is essential to have as few counterparties as possible, but there must always be one. If you hide your money or gold in the ground, the hole will be your counterparty, and someone might steal it, or you might forget where it was.

If you store your metals in a high-security vault, you must have direct ownership and access to your gold and silver bars without going through a middleman. Most companies that organise vault storage do not allow direct access without their approval or often not at all. This is absolutely not acceptable.

ONLY 10% IN GOLD IS NOT SUFFICIENT PROTECTION

Many people ask us what percentage of financial assets to hold in metals. We advised up to 50% back in 2002 when gold was $300. That might be more than many people will be comfortable with. Most of our clients have at least 25% in precious metals. No use holding only 10% when risk is extreme and you expect major problems in the financial system. My recommendation is that investors should at least hold enough gold and silver to fall back on if their other assets collapse or become illiquid.

As I showed in my article two weeks ago (REAL GOLD PRICE LOWEST IN 50 YEARS), gold is now as cheap as in 1970 (at $35) and in 2000 (at $250). Thus, this is the perfect time to acquire gold and silver for wealth preservation purposes.

What is interesting to note is that the Swiss gold refiners, who produce 70% of the gold bars in the world, are reporting very slow business in December and so far also in January. In spite of this, gold is up $75 since early December.

Also, China is continuing to increase its total gold holdings and acquired another 178 tonnes in December, taking the total to 17,100 tonnes.

The East is continuing to accumulate gold at an increasing pace. Whilst the West hasn’t got a clue that the financial system and currencies are on the verge of collapse, the wise people in the East understand the vital importance of wealth preservation and also that “money is gold and nothing else”.

SHORT TERM OUTLOOK

Looking at investment markets, there will be major changes in 2019. Stocks have turned down, and so has the dollar. Gold and silver are on their way to new highs. It looks like the next major fall in stocks is imminent, as well as the move up in the metals.

However, wealth preservation investors should not be concerned with short-term price movements and instead hold physical gold and silver as insurance against an investment and counterparty risk, which is greater than at any time in history.

About Egon von Greyerz

Egon von Greyerz

Founder and Chairman

VON GREYERZ AG

Zurich, Switzerland

Phone: +41 44 213 62 45

VON GREYERZ AG global client base strategically stores an important part of their wealth in Switzerland in physical gold and silver outside the banking system. VON GREYERZ is pleased to deliver a unique and exceptional service to our highly esteemed wealth preservation clientele in over 90 countries.

VONGREYERZ.gold

Contact Us

Articles may be republished if full credits are given with a link to VONGREYERZ.GOLD