Dark Forces, Plain Speak, Brighter Gold & The Fed’s Sick End Game

Below, we look at debt forces alongside supply and demand forces to help investors see (and prepare for) the darker forces within an entirely rigged end game and shifting financial backdrop.

As usual, the end game will boil down to yield curve controls and more money printing, which means more currency debasement and a central bank system that secretly (and historically) favors inflation over truth and markets over Main Street.

2018: A Template for 2023

Throughout the entire year 2018, as the Fed forward-guided rate hikes at 25 bps a pop, I warned investors of a massive year-end correction and to prepare their portfolios accordingly.

This required no tarot cards or market-timing hype.

So, how did I know?

Easy: The Fed told me so in October of 2017. That’s when they publicly announced a tapering of Treasury purchases and progressive rate hikes for 2018.

In short: They were putting a match to a can of gasoline.

Given that liquidity and low rates were the sole winds beneath the debt-driven market bubble which began under Bernanke following the 2008 crisis, it didn’t require exceptional genius in 2017 to see that reduced liquidity and rising rates in 2018 would immediately have the opposite effect—namely, send bloated markets tanking.

By Christmas of 2018, markets were gyrating at 10% swings per day, and by New Year’s Eve, panic was everywhere as I watched the fireworks from Cannes with that annoying “I told you so” expression.

Rolling into 2019, the Fed then did precisely what any addict would do. When markets tanked, the Fed stopped the rate hikes and re-ignited more addictive money printing liquidity—literally unlimited QE.

My book, Rigged to Fail, came out that same year; the timing as well as title was spot on. The Fed’s mandate was the market, not the economy. Debt, and the future be damned—just prop risk assets and let the next generation swallow the bill.

Today, we see a similar “2018 move” from hyper-liquidity to drying-liquidity by a desperate Fed tapering UST purchases into a market bubble and seeking to raise rates despite a debt bubble.

Why are they repeating this insanity yet again?

Simple: They see a market implosion ahead and need rates to go up now so that they will have something to cut when the next recession and market slide–which they alone created rears its head yet again.

Get Ready for Convulsions in 2023

So let me be perfectly clear again: When the current QT liquidity spigot starts to dry up during a “taper,” the liquidity-addicted markets will go into withdrawal convulsions.

In other words, expect some serious volatility in 2023.

To grasp this, it is essential to recognize the illusion of Fed power in general and to embrace the tragic fragility in what was otherwise the most liquid (i.e., doped and artificial) market in the world.

And if you want to see what fragility looks like, keep reading…

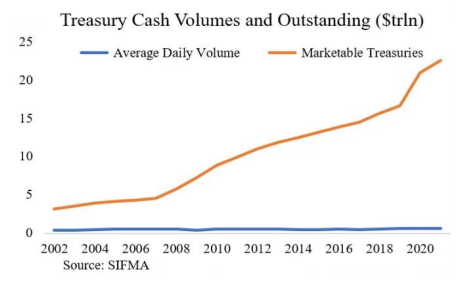

Boring Stuff Like Treasury Volumes

For the last two decades, outstanding Treasuries (i.e., Uncle Sam’s IOUs) have risen by 7-fold while cash volumes for the same period rose by less than 2-fold from $370B to $620B.

In short, liquidity is steadily drying up, and every market crisis is at root a liquidity crisis. The above imbalance is a ticking Treasury timebomb.

Looking ahead, this means that just about any trigger can move liquidity-addicted markets from a tremor to a full-on earthquake.

When today’s “forward-guided” tapering (i.e., QT) shocks an even more bloated 2023 market in the same way that QT shocked an already-bloated 2018 market, the aftershocks tomorrow will be brutal, so hold on tight and get your portfolios prepared before rather than after the quake.

Treasuries, the USD and Gold

As for Uncle Sam’s embarrassingly unpopular (i.e., distrusted, discredited and un-wanted) IOUs, the ramifications of this debt addiction are severe and far ranging, especially for the global reserve currency.

We’ve been writing extensively of the USD and its slow de-anchoring and decline in prominence, a long-overdue slide only accelerated by the disastrous ripple effect of the myopic sanctions aimed at Putin (but which shot the West’s foot).

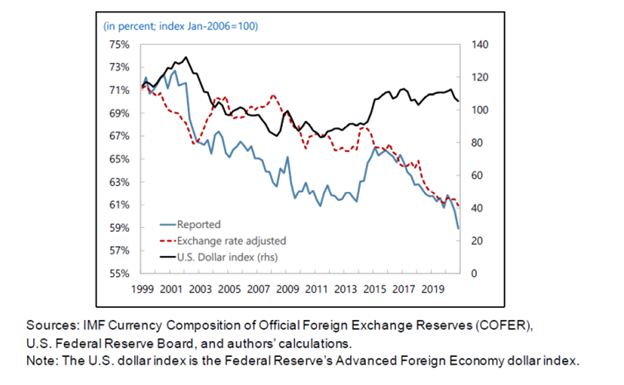

As the chart below shows, the percentage of US Dollars in global FX reserves has fallen in the last 20 years from 73% to 58%, which reveals the consistent decline in foreign demand for US Treasuries.

Of course, when demand falls, so does price, and when demand (and prices) for US sovereign bonds fall, their yields go up.

And when yields go up, so too do interest rates and the cost of US debt, which scares debt-soaked markets like the DOW, NASDAQ and S&P almost as much as it scares debt-soaked countries like the US.

Why a Strong USD When Demand for USTs is Tanking?

Many of you, however, may be scratching your heads and wondering why or how the USD has remained elevated in its international trade value despite clear declines in the USD’s share of global FX reserves?

A true paradox to be sure, no?

We think this can be explained by the fact that as the number of USDs in FX reserves declines (i.e., as foreign purchasing of UST’s declines), this forces Uncle Sam to increase his borrowing at far greater levels than the global markets.

This dynamic pushes up the price of the USD.

In short, Uncle Sam is borrowing so much that he’s actually a market-maker creating his own demand for his own dollar.

But here’s the rub—and it’s a doozy.

That same USD can tank if Uncle Sam issues so (too) many IOU’s that the supply of USTs gets so (too) massive that bonds tank in price and yields spike.

This inevitable dynamic (too many IOU’s and too little global demand for the same) will force the Fed to impose open Yield Curve Controls (or “YCC”—which just means more money printing to buy bonds), an end game I’ve been predicting as inevitable for over a year now.

The End Game: YCC Just Means a Weaker USD

Over-supply of UST’s will push bond prices down and bond yields up.

Rising yields will then force the Fed into official YCC, which, to repeat, simply means more printed/debased dollars that will send the USD falling to levels commensurate with the graph above.

This potential trend toward a falling USD, by the way, is just one more reason to favor gold in particular and commodities, industrial equities and real estate (agricultural/luxury) in general as everything broken gets even more broke in the coming months.

Bankers to the Rescue? Think Again

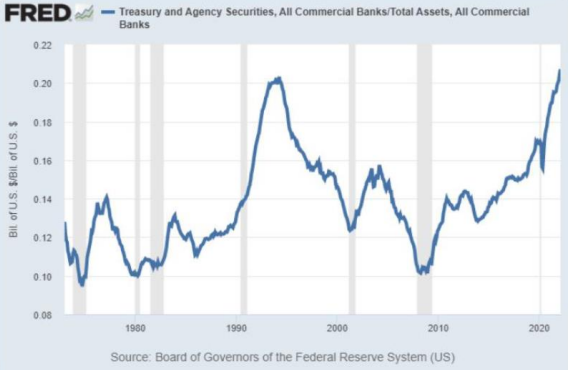

Many, however, will argue that the big US banks (you know, those TBTF juggernauts of sound management you bailed out in 2008) will help Uncle Sam by purchasing his otherwise unwanted IOUs and thus create more rather than less demand for USTs—thereby “saving” the Dollar too.

After all, the big banks helped Uncle Sam in the aforementioned disaster of 2018, so why can’t they do it again in the pending disaster circa 2023 and buy more US IOUs?

The answer boils down to this: Those big banks have already purchased/consumed so many UST’s that they are risking indigestion.

Today, US commercial banks are already sitting upon the highest percentage of USTs on their balance sheets in history.

So, folks, if: 1) foreigners don’t want Uncle Sam’s debt (weaponized FX reserves post-Ukraine hardly made the US or its bonds popular) …

…and 2) if even JP Morgan and other banks don’t want it, this just means…

3) USTs will keep tanking, and…

4) yields will keep rising like shark fins and…

5) more centralized control from DC in the form of YCC (i.e., gobs more money printing) is now as inevitable as the setting sun falling on the once-revered US financial system.

Of course, more money creation just means more inflation as measured (i.e., defined by) silly things like the money supply, which in turn just means more debased dollars ahead and thus more reasons to love assets which central banks can’t print or create with a mouse-click, namely: GOLD.

More Debt, Less Buyers = Uh Oh Ahead

To add even more comedy to the tragi-comedy of the cornered Fed and bankrupt US, the folks at the US Treasury are about to issue even more un-loved IOUs at precisely the same time in which the demand for them is shrinking at a record and global pace.

US deficits as a percentage of GDP are rising like a cancer amidst to the entire world as Uncle Sam’s bar tab bloats beyond anything his equally comical “Office of Management of the Budget” (“OMB”) predicted in the last six years.

No shocker there.

The list of failed projections coming out of the OMB (not to mention the BLS) would take too many paragraphs to fully describe.

For now, it’s worth a reminder that in 2016, that same OMB forecasted that US deficits as a percentage of GDP would remain flat at around 2.75%.

By the end of that same year, however, the deficit percentage shot up to 3.75% (following a rate hike, btw…).

In 2017, that percentage then rose to 4%; in 2018, deficit levels climbed to 5% of GDP and by 2019, the percentage was 2X higher than what the same OMB had “forecasted” in 2016.

Again: So much for trusting the experts…

How Nations Die

Given that debt is rising faster than income or tax receipts in the US, do we really think Uncle Sam and Uncle Fed will allow the cost of that debt (i.e., interest rates) to rise even more?

Given blunt math rather than fancy words or political posturing, the Fed will need to keep yields controlled and hence interest rates repressed.

And the only way to do this is to keep bond prices up and yields down.

And the only way to keep bond prices up is if there are buyers.

And if since are no buyers (foreigners or banks, see above), then the buyer of last resort will be the Fed.

And the only dollars the Fed has are the kind that are created out of thin air.

And that, folks, is how nations die from within and currencies rot from the top down.

As I see it, more liquidity injections and hence YCC are ahead, and will come into play the moment the stock markets start to gyrate and die like a fish on the dock.

Why Not Let the Market Die?

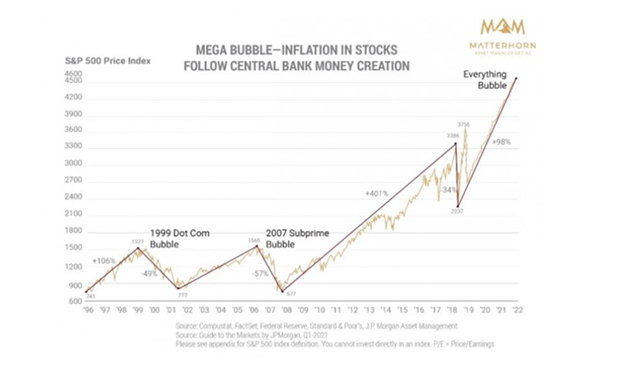

Some, including von Mises (and myself), would have no tears for the death of a bloated, artificial and wealth-disparity-creating, social-unrest-generating and entirely capitalism-destroying market bubble like the current one.

After all, the “constructive destruction” of cancerous market bubbles like this one…

…is in fact a natural and necessary part of healthy capitalism.

This is why some feel the “Fed put” (or airbag) below the current everything bubble will no longer be there to save Mr. Market next time around.

A crashing (deflating) market, after all, would help the Fed fight inflation, so perhaps they’ll just step aside and let the S&P tank, right?

Hmmm…

Not so fast.

As I’ve said for years, the Fed’s real mandate is not the USA, its workers or the cost of groceries.

Good grief, the Fed isn’t even federal.

It’s a private bank created by bankers to prop markets not national interest.

DON’T ever forget this—even if your elected officials were lobbied to forget this.

Furthermore, if the Fed were to turn its back on more money printing, YCC and/or rate “accommodations” and thus fail to “support” the market once the next implosion comes, then IRAs, pension funds and even wealth managers lose a fortune, which means consumers lose a fortune and stop spending.

The US Can’t Afford to Let Markets Die

If this next implosion were not bailed out, consumer spending, as well as tax receipts, would tank and the nation (and markets) would sink into a recession that would make the 1930’s seem pleasant.

In short, the Fed knows that our stock market (as grotesquely fake, bloated, rigged and rotten as it may be) is nevertheless about the only thing that is “positive” in the US of A.

As a result, I feel it’s far more likely that the Fed will momentarily watch markets flip and flop (deflationary, yes), but will then immediately pivot out of QT and jump into QE overdrive, printing trillions more to save Mr. Market in the form of YCC and runaway inflation.

Such measures, of course, will crush Main Street yet, once again, bail out Wall Street, which is the Fed’s true love and mistress—i.e., its real mandate.

As I’ve also warned, the Fed pretends to combat inflation, but in truth, wants inflation to inflate away its debt.

In short, the next QT-to-market implosion-to-market-bail-out will resemble the 2018-2019 pivot (discussed above) all over again, but at a far greater level of insanity—i.e., level of “emergency” money printing.

This insanity, of course, “saves” artificial markets but kills the inherent purchasing power of those fiat currencies mouse-clicked at the Eccles Building and now sitting (dying) in your checking account.

Again, this all points back to gold as currency insurance in a world where currencies are already burning to the ground—and will burn even faster when YCC becomes the new MO of the FED.

About Matthew Piepenburg

Matthew Piepenburg

Partner

VON GREYERZ AG

Zurich, Switzerland

Phone: +41 44 213 62 45

VON GREYERZ AG global client base strategically stores an important part of their wealth in Switzerland in physical gold and silver outside the banking system. VON GREYERZ is pleased to deliver a unique and exceptional service to our highly esteemed wealth preservation clientele in over 90 countries.

VONGREYERZ.gold

Contact Us

Articles may be republished if full credits are given with a link to VONGREYERZ.GOLD