Bonds Die, CPI’s Lie & Gold Rises

Below we look at Gold’s rise in a backdrop of more bond destruction in the public markets and more truth destruction in the war on inflation.

No Recession Yet?

As I argued in 2022, the much-debated and pending recession was in many ways already here, despite official attempts to re-define the same.

The thousands being laid off at Google, Amazon and even Goldman Sachs in 2023, for example, can likely attest to that.

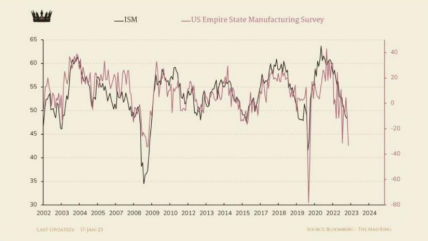

Speaking of recession, last week’s embarrassing Empire Manufacturing report of -32.9 adds more confirmation that productivity and growth are not going to save our increasingly knee-capped economy.

In fact, the manufacturing figures have not been this bad since 2008 and 2020, which, if I recall, were pretty bad vintage years for markets—”saved” only by money printing at warp speed.

This, of course, raises the ever-charged question of whether Powell will be forced to return to more desperate mouse-click money creation—i.e., “quantitative easing.”

For now, of course, the current Fed is going the other direction, “tightening” rather than “easing” reserve assets to the tune of -$95B per month into a perfect debt storm.

As we’ll see below, this lose-lose option is just one of many hidden mines lying just beneath the surface of an already limping US Treasury market.

In the meantime, the dumb just keeps getting dumber.

U.S. Government Bonds: Safe Haven or Mine Field?

Most investors, sensing a recession, are doing what most investors typically do in bad times: Make bad choices.

Key among these bad choices is the traditional flight to long-dated US Treasuries as a “safe haven” as markets and economies head south.

I am here to suggest that such a traditional safe haven is now more like a death trap.

Why?

Well, the answers are found in blunt facts and simple math—two themes our policy makers have long-ago decided to cancel, deny or ignore.

So, let’s do the math. It’s as easy as 1, 2, and 3.

The Simple Math of Dying US Bonds

- Fed Deficits—The First Land Mine

In the painful days of 2008 and 2020, U.S. deficits as a percentage of GDP rose by 8% and 10% respectively.

After all, bad times require more debt “accommodation”—i.e., more deficit spending and rising growth rates for debt.

Heading into 2023, the annual Federal deficit burn rate was already at $1.5T, which is not only embarrassing but dangerous.

Unfortunately, hard math suggests that this figure is likely to get worse in 2023.

Much worse.

Using the prior deficit growth percentages (800 and 1000 bps) in 2008 and 2020, respectively, 2023 could mathematically see annualized Federal deficit burn rates hitting $2T to $2.6T, which would conservatively place the U.S. Federal deficit somewhere between $3.5T and $4T in 2023.

But that’s just the beginning.

- More QT, More Deficit Pain: Land Mine Number 2

If we then tack on the current -$95B monthly tightening (QT) at the Fed, this would take our 2023 deficit levels near and then past the $5T mark.

This, of course, is assuming Powell doesn’t pivot from his QT war on inflation, which as my last report objectively confirmed, risks sending the US markets and economy to lows not seen since well before 1871…

- Foreigners Dumping Uncle Sam’s IOUs: Land Mine Number 3

The growing lack of trust and interest in USTs merely compounds the problem and math of this ticking deficit timebomb.

As argued throughout 2022, Powell and Yellen’s myopic and one-sided policy of raising rates and strengthening the USD was an absolute gut-punch to foreign currencies and economies.

Like the sanctions against Putin, this attempt to lure foreign money into the UST market backfired.

Instead, it just forced developing and developed nations (from the BRICS to Japan) to dump (sell) USTs in order to defend their own currencies against the otherwise bully-like and unsustainable rise in the USD.

Given the foregoing, we could easily witness another $1T in foreign selling of US Treasuries in 2023, which could ostensibly lift that growing US deficit figure above $6T by year end.

Doing the Math

The very notion of such a net issuance in USTs suggests that the supply of Uncle Sam’s IOUs will be greatly surpassing their demand as we limp into 2023.

From high-school econ, we know that such a mis-match in supply and demand means a massive fall in price.

Stated otherwise, U.S. Treasuries will be falling like Newton’s apples as yields rise like approaching shark fins.

Do USTs Still Make Sense to You?

Returning, then, to the original question of whether the traditional flight to long-dated US Government bonds as a safe-haven makes sense in the current reality, the answer becomes easier to see.

In short, the need to dramatically increase the supply of USTs to match growing US deficit levels is greatly at odds with the hard fact that natural and foreign demand for those IOUs just aint there anymore…

Unless, of course, these IOUs are purchased with mouse-click money and Powell’s so-called war against inflation pivots toward a QE policy of extreme inflation.

Ahhh. The ironies, they do abound. Powell is quite simply cornered. His options are horrific.

He either tightens and thus destroys markets and Main Streets, or he loosens and destroys the USD within an inflationary hurricane.

Given current policies and trends, it is therefore mathematically safe to suggest that going long those long-dated USTs is more akin to tip-toeing through a minefield rather than sailing into a “safe-haven.”

As maintained throughout 2022, and despite the official narrative to the contrary, my view is that growth rates and yield curves suggest we are already in a recession, and that once that recession becomes official (always a lagging announcement), there will be even more UST issuance and hence even more tanking bond prices.

The USD and Gold

As for the USD and its impact on the Dollar-based gold price, throughout 2022 I argued that the strong USD was an obvious gold headwind.

I also argued, many times, that such a strong USD was not a sustainable path, for the simple reason that rising debts, rising interest rates and a rising currency are not a sustainable trio.

Given the deficit levels discussed above, and given the $2.9T the U.S. spends on entitlements as well as the $900B annually handed over to its military industrial complex/leadership, there’s simply no way the US can continue a strong dollar policy without risking outright default.

But given the fact that defaults amount to political suicide as well as global disruptions in credit and banking systems not seen since the second world war, it’s far more likely that the Fed, which is apparently more powerful than the White House in setting economic policy, will eventually require more “liquidity” to buy Uncle Sam’s otherwise unwanted but increasingly issued bonds.

Such liquidity is a clear and seemingly inevitable inflationary tailwind, so please don’t be mollified by the so-called fall in official CPI inflation from 9% levels to the current and misreported 6.5% headlines.

This liquidity is also an open headwind to the USD, whose temporary rise in 2022 is potentially heading for a much longer-term fall in the months ahead.

As the USD’s relative strength as well as inherent purchasing power makes deeper turns south into the foregoing debt storm and inflationary flood, gold’s slow and steady trend north is fairly easy to foresee.

How to Fix Inflation? Just Lie

But as for inflationary pain and gold’s gradual victory over the same, our genius policy makers in DC have come up with a simple and familiar solution: Just lie about it.

As former Finance Minister and European Commission President, Jean-Claud Juncker, famously confessed, “when it becomes serious, you have to lie.”

And when it comes to lies from high, the empirical abundance of such lies over the years is not fable but fact.

From employment data to CPI data, or from central bank distortions and digital currencies to Ex-Items accounting scams and media fictions on viral science or the re-definition of a recession, the rising levels of open fantasy passing for daily reality seems to suggest that things must indeed be getting “serious.”

In other words, the lies are mounting in lock step with mounting financial desperation.

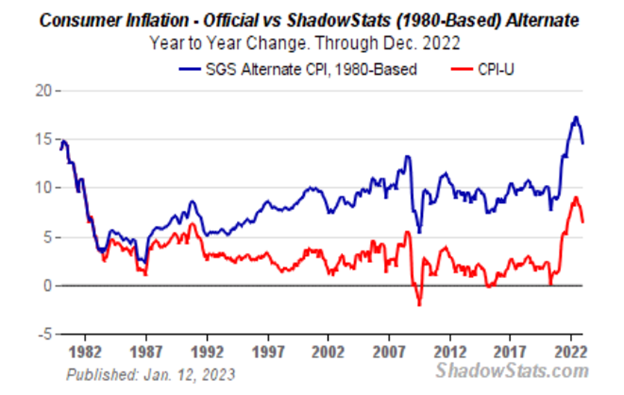

Despite such serious problems, the latest changes now being made to redefine an already dishonest CPI scalefor measuring inflation is nothing short of comical, or at least tragi-comical.

As I’ve argued for years, the Fed’s public ruse to fight inflation while simultaneously exploiting inflation (and negative real rates) to “inflate away” historical debt levels was a dishonest of way of “having their cake and eating it too.”

That is, the Powell camp can lie about (i.e., misreport) actual inflation (the “cake”) for the headlines while enjoying the benefits of hidden/denied inflation (“eating it too”), whose presence and continued rise toward stagflation (in my opinion) has been and will be anything but “transitory,” as I warned long before Powell invented that term (lie).

As for the CPI methodology changes scheduled to take effect next month, the inflation fiction writers over at the Bureau of Labor Statistics (i.e., the BLS, or “Office of BS” for short) have decided to adjust the weightings for Owners’ Equivalent Rent (or, “OER”).

The Official Data: Never Right, but Never Wrong

Among other tricks, the aim of the Office of BS is to now use neighborhood level information on housing structure types for a calendar year to effectively manipulate a lower than honest CPI inflation rate.

This is rich coming from a CPI scale (red line below) that is already notorious for under-reporting genuine inflation by 50% when compared to the old inflation scale (blue line below) used in the Volcker era.

Effectively, such lies may never be right, but as the official data point of the US Government, they are also never wrong.

Now, the big question going forward is simple: Will the lie work?

The inflation data from the US Office of BS is the effective equivalent of a thermometer which promises the sick a healthy temperature despite the fact that they are literally burning with a 103-degree fever, night-sweats and aching muscles.

Such tricks open the door for Powell to even return to more inflationary money printing without risking inflationary headlines simply because the CPI scale is telling us the inflation “data” is improving—despite the fact that consumer expenses are literally burning with a 103-degree fever, night sweats and aching muscles…

Just ask yourselves: Does your cost of living seem to be rising by 6.5%, or does that “fever” feel a bit higher than what you’re being told?

Gold: A Better Safe Haven?

Based upon the foregoing, each of us must therefore ask ourselves where to find his or her safe haven in a time of extended war, dishonest math, re-defined recessions, dying bonds, debased currencies and gyrating equity markets trending noticeably south.

Traditionally, of course, the risk-free-return of sovereign bonds in general and USTs in particular was understood as the safest bet.

Based, however, upon 1) the non-traditional, and in my opinion, complete distortion/destruction of the global bond marketsdue to years of criminally negligent monetary policies from Tokyo to DC and 2) the genuine rather than reported real (i.e., inflation-adjusted) return on Uncle Sam’s IOUs, it becomes increasingly clear that their “risk-free-return” is little more than return-free-risk.

That is why more informed investors, willing to take the extra minutes to understand simple bond history and math soon discover that yes, even the 0% yield of gold with its naturally-derived/constrained stock to flow ratio (i.e., a nearly “finite” annual production of barely 2%) and infinite duration does a far better job of preserving wealth than bonds of finite duration and seemingly infinite issuance…

Got gold?

About Matthew Piepenburg

Matthew Piepenburg

Partner

VON GREYERZ AG

Zurich, Switzerland

Phone: +41 44 213 62 45

VON GREYERZ AG global client base strategically stores an important part of their wealth in Switzerland in physical gold and silver outside the banking system. VON GREYERZ is pleased to deliver a unique and exceptional service to our highly esteemed wealth preservation clientele in over 90 countries.

VONGREYERZ.gold

Contact Us

Articles may be republished if full credits are given with a link to VONGREYERZ.GOLD